/Intel%20Corp_%20Santa%20Clara%20campus-by%20jejim%20via%20Shutterstock.jpg)

Since taking up the CEO position at the beleaguered chip giant, Intel (INTC), Lip-Bu Tan has made it clear that he is the ultimate authority at the company now. Shareholders should have no complaints, as the stock has more than doubled since his appointment. As such, several investments in startups where Tan is closely involved have not raised governance issues around Intel (yet).

The clear first among equals, among these investments, has been in a company called SambaNova. Planning to invest about $15 million in the AI infrastructure company, Intel's latest investment would increase its stake in SambaNova to 9% from 6.8% earlier. Notably, Intel's association with SambaNova has been long, with the company participating in the latter's $150 million Series B round in 2019.

However, the gap between the last investment and the latest one comes within a gap of just two months. Part of the company's $350 million Series E round in February, Intel's latest move, and within such a short span of time, begs the question: What is the rationale? Has anything changed in the past couple of months? Let's find out.

What Sealed the Deal?

The clear rationale for another investment centers entirely on capturing the lucrative enterprise inference market. Since finalizing a strategic collaboration earlier this year, the companies have been heavily integrating Intel Xeon processors with SambaNova SN50 accelerator chips. Funding the startup in rapid successive tranches gives Intel management the ability to monitor critical technical milestones while easily navigating regulatory red tape. This is basically Intel placing a massive financial hedge to ensure they secure a premium spot in specialized data centers without having to acquire the startup outright.

Holistically, SambaNova gives Intel a very real shortcut to challenge the absolute dominance of Nvidia (NVDA) and the rising server threat of AMD (AMD). Nvidia currently maintains an iron grip on the market for training massive language models, so SambaNova smartly targets the inference stage where those models actually operate in everyday applications. Their custom reconfigurable dataflow units are drastically more power efficient than standard graphics processing units. By packing Intel server processors and networking equipment alongside these specialized inference chips, Intel can pitch a complete turnkey hardware rack. The two companies claim this joint architecture delivers a total cost of ownership up to ten times better than traditional graphics card setups, which is a massive selling point for cost-conscious corporate buyers looking to host private local models.

On the proprietary hardware side, Intel just unveiled its Core Ultra Series 3 processors at the 2026 Consumer Electronics Show (CES). These chips are a huge deal because they are the very first consumer platform built on the highly anticipated Intel 18A manufacturing node. They bring vast improvements in power efficiency while baking in much larger graphics and neural processing units for local desktop workloads.

Looking slightly further out to late 2026, the company is also prepping the Series 4 Nova Lake desktop line. These specific chips are engineered to reclaim the absolute performance crown from AMD by introducing a massive cache memory system designed to directly neutralize competitor cache advantages. Thus, between the increased core counts and advanced integrated graphics, Intel is finally showing signs of catching up to the raw performance gap with its biggest rivals.

Financials Slowly Progressing

Intel's decade of difficulties was marked by revenue and earnings posting negative CAGRs of -0.46% and -45.59%, respectively, over the past 10 years.

Also, there are some telltale signs of stabilization in the financials, however. Over the past nine quarters, Intel has beaten Street earnings expectations on six occasions. The most recent quarter also delivered beats on both revenue and earnings.

Notably, revenue declined 4% year-over-year (YoY) to $13.7 billion. The client computing segment, still the largest, fell 7% to $8.2 billion, though this could improve in the coming quarters with the launch of the company’s first AI PC platform built on the Intel 18A process, the Intel Core Ultra Series 3. The data center and AI segment grew 9% to $4.7 billion, while the Foundry business increased 4% to $4.5 billion.

Earnings per share rose 15% to $0.15, comfortably ahead of the $0.08 consensus. This marked the second consecutive quarter of beating earnings estimates.

Meanwhile, cash flow from operations for 2025 totaled $9.7 billion, up from $8.3 billion in the prior year. The company ended the quarter with $14.3 billion in cash and equivalents, well above its short-term debt of $2.5 billion.

Valuation metrics present a mixed picture. The forward P/E of 104.21 sits significantly above the sector median of 21.76. However, the forward P/S of 4.70 (versus 2.93) and forward P/CF of 17.72 (versus 16.50) appear more reasonable relative to peers.

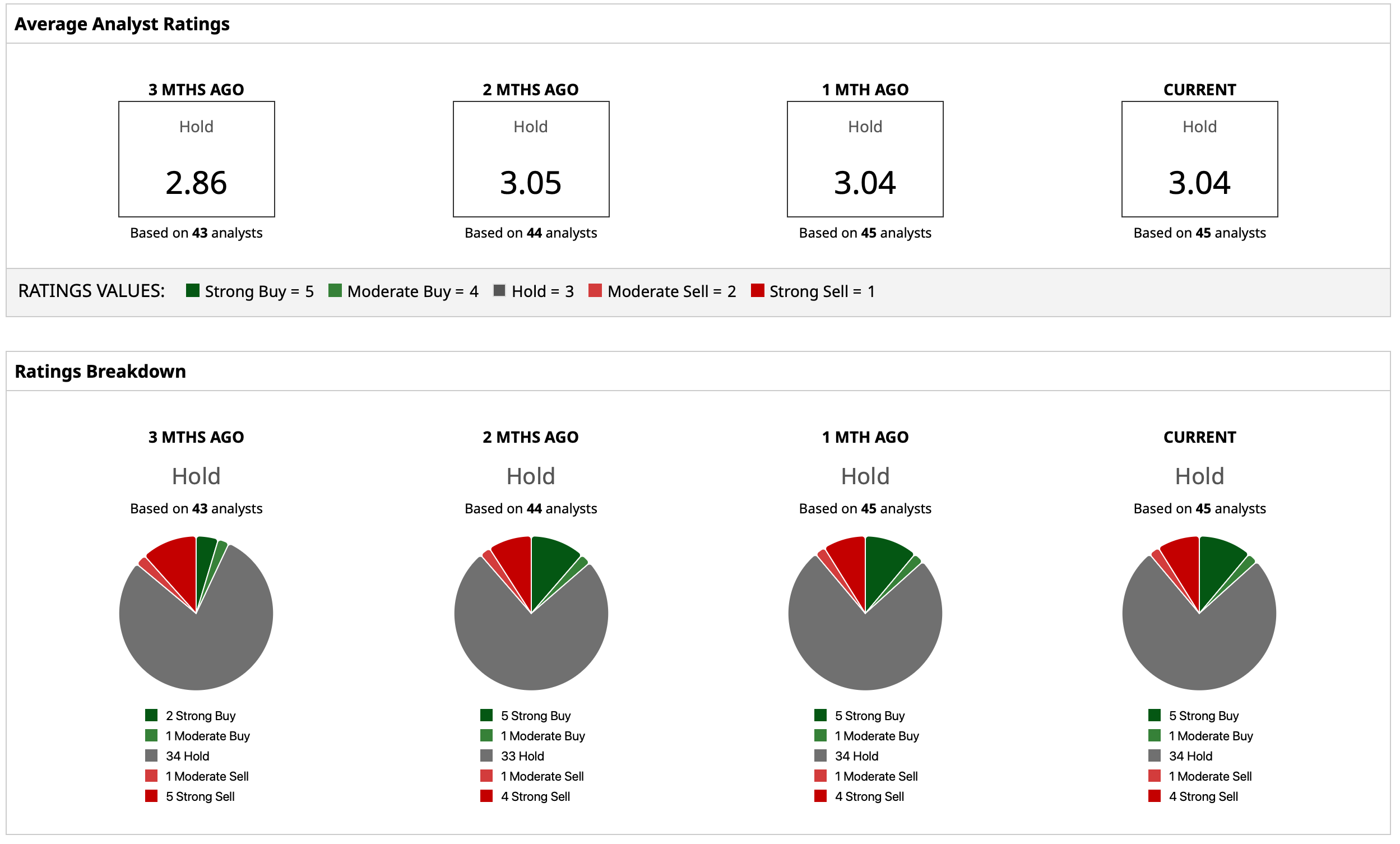

Analyst Opinion on INTC Stock

Overall, analysts continue to rate the stock a consensus “Hold.” The mean target price has already been surpassed, while the high target price of $66 indicates an upside potential of about 31% from current levels. Out of 45 analysts covering the stock, five have a “Strong Buy” rating, one has a “Moderate Buy” rating, 34 have a “Hold” rating, one has a “Moderate Sell” rating, and four have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)