/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

Chinese tech shares have been bumpy of late. Investors have grown wary of sky-high AI research and development costs and slowing consumer spending in China. In this environment, Alibaba (BABA) has been walking a tightrope. Its core e‑commerce business is grappling with intense competition and soft demand, even as the company plows money into cloud computing and artificial intelligence (AI).

Meanwhile, this month, Alibaba unveiled Qwen 3.6-Plus, a new “agentic” AI model designed to let software act on its own. Think of it as an AI assistant that acts, not just answers. The rollout highlights Alibaba’s strategy to be a major player in AI, but in the near term, it’s mostly a long-term growth story for the company.

Alibaba Pushes AI Into Core Products

Alibaba dominates Chinese online retail and has been expanding into new tech frontiers. Now, the company is weaving AI into its main products. It renamed Ele.me as Taobao Instant Commerce and added the service to the Qwen app, letting users place delivery orders through its AI assistant. The company has also rolled out tools like the M6 image model and Wukong enterprise chatbot, showing strong innovation, even if the payoff may take time.

Alibaba stock has had a roller-coaster year. By late 2025, it had rallied, helped by surging cloud and AI revenue, shares slid sharply in early 2026. Year-to-date (YTD), BABA stock is down roughly 16% as investors shake out of crowded tech trades. Much of the late 2025 gain has evaporated on profit worries. Moreover, traders have been “selling the news” on Alibaba’s recent results and investments, leaving the stock in a short-term downtrend despite strong long-term fundamentals.

Like other tech giants, Alibaba doesn’t look wildly overvalued. Its trailing price-to-earnings (P/E) ratio is about 25.7 times, which is below its own 10-year median of 28 times and quite reasonable for a high-growth tech name. BABA stock also has a price-to-sales (P/S) ratio of 1.9 times, which is below the industry median of 2.1 times. Alibaba trades cheaper than many of its peers and even below some of its historical norms, suggesting that the stock is not frothy but roughly in the fairly valued range.

The Qwen 3.6-Plus AI News

The latest big news from Alibaba is Qwen 3.6-Plus, its large language model tuned for “agentic” AI tasks. This model is meant to not just chat or translate but to carry out multistep tasks (like planning travel, coding, or managing simple projects) on its own. Alibaba says the new model has improved coding and reasoning skills, works with text, images, and even audio, and is optimized for business use. It will power features like the Wukong platform, Qwen app and Alibaba’s “Token Hub” AI suite.

Analysts had already predicted Alibaba would lean heavily into AI. For example, Morgan Stanley cited “explosive AI demand” and strengthened commercialization as reasons to stay bullish.

Goldman Sachs even moved Alibaba to its APAC Conviction List, forecasting 30% to 35% EPS growth by fiscal 2027 and 2028 thanks to cloud and AI. So, while Qwen 3.6-Plus underscores Alibaba’s cutting-edge credentials, most investors see its payoff as long-term.

Alibaba Profitability Under Pressure From Heavy Spending

Alibaba’s third quarter showed both the challenges and strengths of the business, yet missed estimates on both lines. Revenue was $40.7 billion, up only 2% year-over-year (YOY) on an absolute basis, or about 9% excluding disposed units like Sun Art.

Profit metrics took a hit due to heavy spending. Net income fell about 66% to $2.3 billion, and adjusted EPS came in at about $1.01 ADS, down 67% YOY.

Operating cash flow was $5.1 billion, but free cash flow plunged to $1.6 billion, down 71%, reflecting big investments in promotions, quick-commerce, and technology. On the plus side, Alibaba ended the quarter with an enormous cash pile of about $80.1 billion on the balance sheet, giving it a cushion for continued spending.

CEO Eddie Wu leaned hard into AI in his commentary. Wu noted that “AI is and will continue to be one of our primary growth engines,” and highlighted that the Qwen app already exceeded 300 million monthly users by enabling AI agents to carry out real tasks. This underscores Alibaba’s goal of making AI central to everything from shopping to business tools. CFO Toby Xu added that the surge in AI/cloud revenue “gives us confidence to scale investments” and that strong liquidity allows management to spend now for long-term gains.

Management’s message was that heavy investment will continue, especially to improve its logistics/commerce technology, even at the cost of short-term profits. Analysts expect this reinvestment phase to last through fiscal 2026. For perspective, consensus forecasts from Wall Street are for roughly flat revenue next year and continued EPS pressure, with a sharper rebound expected in fiscal 2027 if growth re-accelerates.

What Do Analysts Think of Alibaba Stock?

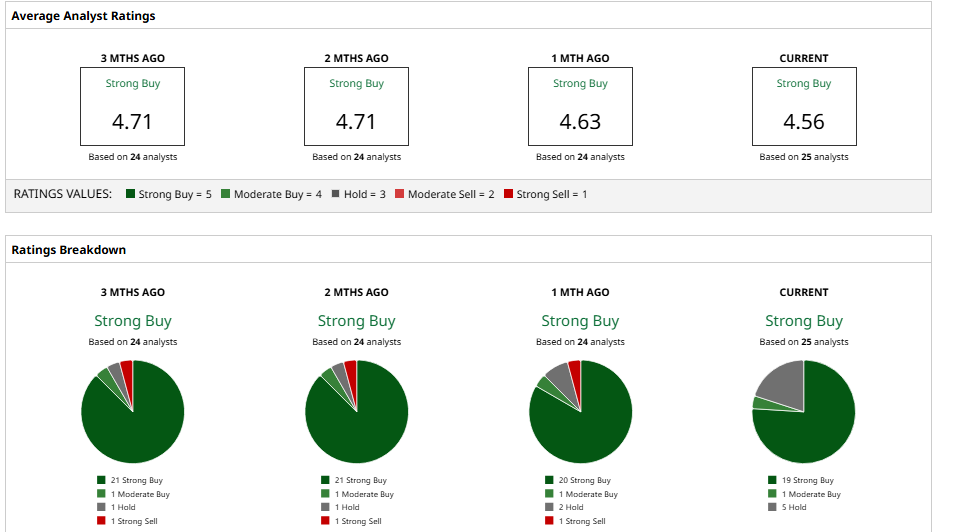

Wall Street is generally bullish on Alibaba’s long-term outlook, although estimates vary.

With the explosive AI demand, Morgan Stanley recently reiterated an “Overweight” rating on BABA stock with a price target of $180, referring to Alibaba as a potential China AI winner. Goldman Sachs became part of the party and upgraded Alibaba stock, predicting it as an APAC “Conviction Buy” and expecting about 31% EPS recovery by fiscal 2027 as AI and cloud go up.

On the other hand, not every firm is bullish. Some outfits are concerned that the vigorous expenditures might postpone any recovery of profits. For example, Erste Group recently kept a “Hold” rating on shares due to margin pressure and increased costs in quick commerce.

Overall, BABA stock has a consensus “Strong Buy” rating. The average 12‑month price target is about $185.13, implying potential upside of more than 51% from current levels.

Should You Buy, Sell, or Hold?

The move by Alibaba into agentic AI is promising. This is the type of innovation that investors had been dreaming of when generative AI first burst. Leadership in AI and cloud may be a source of substantial revenue in the long term for Alibaba. However, in the short term, the company's core business is experiencing challenges, and its profits have fallen to a sharp decline.

I believe Alibaba is currently a hold for a majority of investors. The stock is not yet a buy due to the profit drag, yet neither is it a sell due to Alibaba's robust AI and cloud growth engines. For long-term investors with the patience to wait, Alibaba might be planting the seeds for massive future rewards due to its high expenditures, but for those who want fast returns, the runway can be more than anticipated.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)

/Corning%20Incorporated%20on%20screen%20in%20front%20of%20website%20By%20Timon.jpeg)