/AI%20(artificial%20intelligence)/AI%20Infrastructure%20by%20FOTOGRIN%20via%20Shutterstock.jpg)

Enterprise computing may not grab headlines the way flashy consumer tech does, but it remains one of the most important battlegrounds in the AI era. As companies rush to handle bigger datasets, heavier workloads, and more complex AI applications, the race is on to build the infrastructure that keeps everything running smoothly.

That's where IBM (IBM) and Arm (ARM) come in. The two companies recently announced a strategic partnership aimed at developing new dual-architecture hardware for enterprise AI and data-intensive workloads, while also expanding virtualization and software compatibility across their platforms.

For investors trying to decide which stock looks more compelling from here, this partnership raises an important question. Between IBM’s scale and enterprise reach and Arm’s role in powering efficient computing, which tech stock offers the better long-term opportunity?

Tech Stock #1: IBM (IBM)

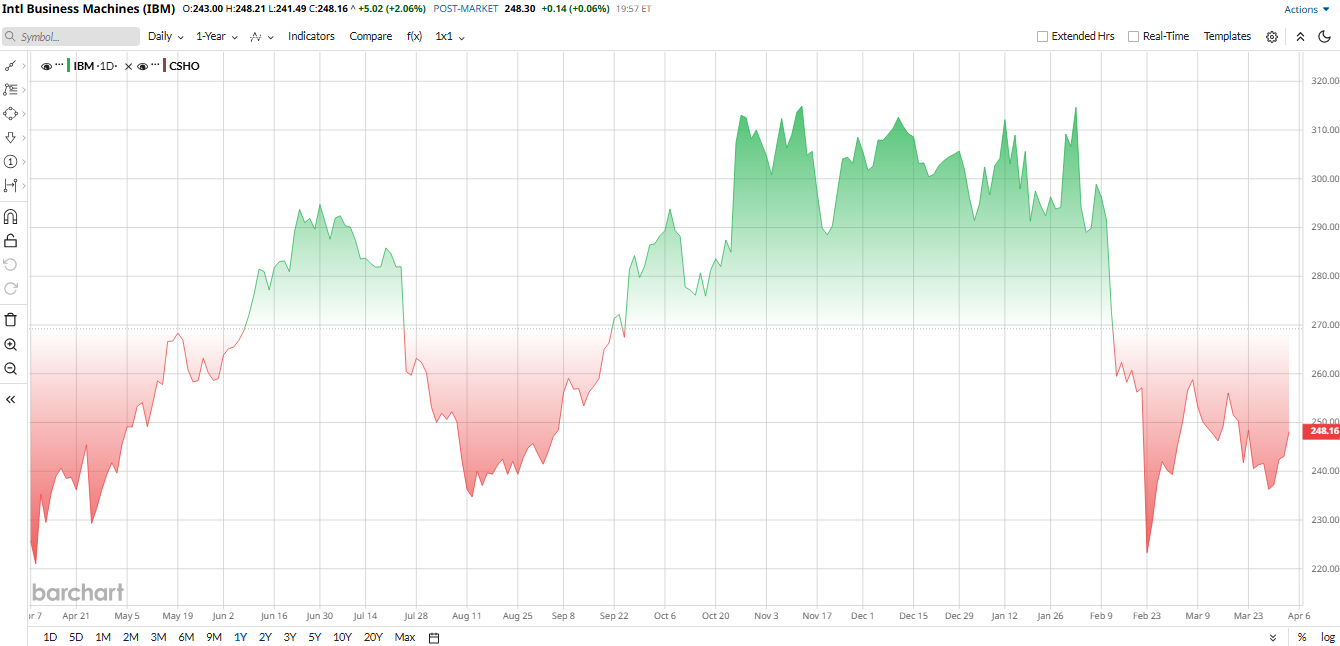

IBM stock has not just gone flat after a strong run. Shares are down about 17% year-to-date (YTD) but up 8% over the past 12 months as the broader first-quarter 2026 selloff, AI valuation worries, and tariff and geopolitical concerns have weighed on the market. IBM also took a sharp hit on Feb. 23 that erased much of its earlier gains, when Anthropic said its Claude Code tool could automate COBOL modernization, stoking fears that AI could disrupt IBM’s legacy mainframe and consulting business.

IBM stock is not cheap, though. IBM trades at around 19.6 times forward earnings, so investors are already paying for a fair amount of future growth. IBM is also a Dividend Aristocrat, having raised payouts for more than 25 years and currently paying about $6.72 per share annually, with a yield near 2.7%.

However, the financial numbers are great. In the fourth quarter of 2025, IBM reported revenue of $19.7 billion, up 12% from a year earlier. Software sales rose 14%, infrastructure sales jumped 21%, and consulting grew about 3%. Gross margin improved to 60.6%, and CEO Arvind Krishna said IBM’s generative AI book of business reached $12.5 billion. For full-year 2025, IBM posted a healthy $14.7 billion in free cash flow, while also guiding for about 5% constant-currency revenue growth in 2026.

IBM is also using the Arm partnership to strengthen its long-term position in AI infrastructure. The collaboration is meant to bring Arm CPUs into IBM’s mission-critical systems, which could help IBM broaden software compatibility and deepen its reach in enterprise computing.

At the same time, IBM continues to invest in its own AI hardware, including the Telum II mainframe processor and Spyre AI accelerator, both aimed at embedding AI into everyday enterprise workloads.

Analysts expect IBM’s upcoming quarter, Q1 fiscal 2026, to continue the growth trend. The consensus calls for mid-single-digit revenue growth and a modest EPS gain. This outlook is in line with IBM’s guidance of 5% constant-currency growth for 2026.

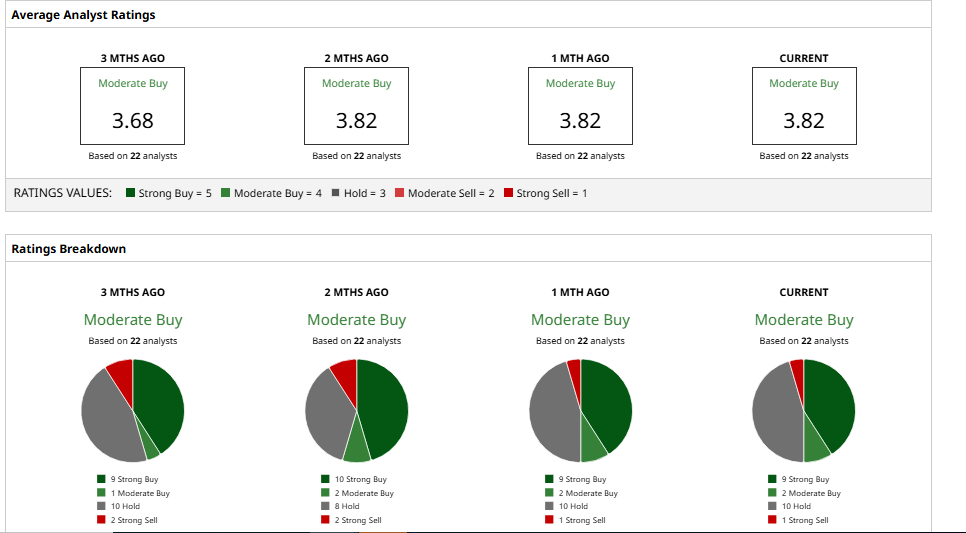

Wall Street remains moderately bullish on IBM stock. The consensus rating is a “Moderate Buy” with an average 12‑month target of $313.90, which implies about 28% potential upside. Analysts are encouraged by IBM’s AI/cloud strategy but note that the P/E tempers expectations. However, the stock's potential upside hinges on the continued execution of its AI-driven growth strategy.

Tech Stock #2: Arm (ARM)

Arm brings a very different profile to the table. The company is best known for its energy-efficient chip designs, which dominate mobile devices and are now becoming more important in data-center and AI applications. That makes Arm a natural partner for IBM, especially as the market shifts toward efficient computing and hybrid infrastructure.

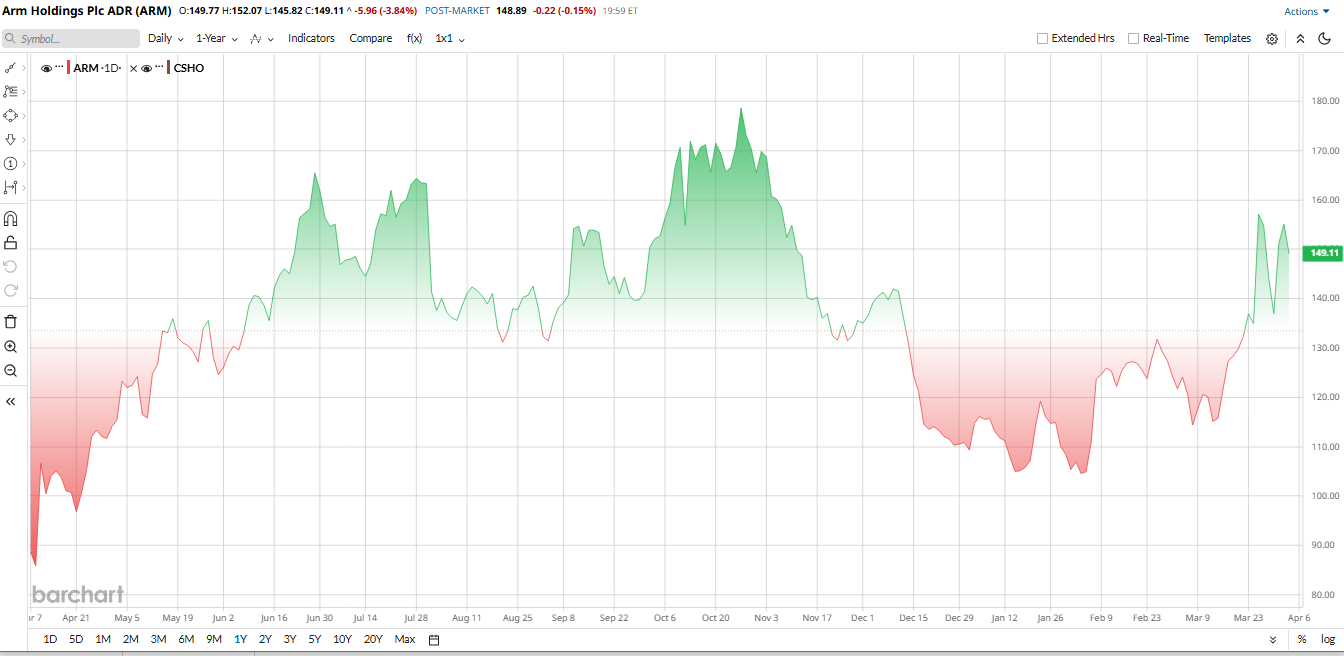

Arm has also had a volatile ride. The stock fell about 11% in 2025 amid broader semiconductor weakness, but it has rebounded in 2026 as business momentum has improved. Over the past 12 months, ARM has delivered a roughly 69% total return, helped by strong demand across AI and data-center markets.

Still, the valuation is rich. The stock trades at around 130 times forward earnings, far above its semiconductor peers. That premium makes sense only if investors believe the company can keep delivering strong growth in AI and infrastructure, and Nvidia’s (NVDA) Vera data-center CPUs. These developments, plus Arm’s partnerships with major cloud and chip players, reinforce its growing role in AI infrastructure.

In its latest quarter, revenue rose 26% year-over-year (YOY) to $1.24 billion, marking the fourth-straight billion-dollar quarter. Royalty revenue climbed 27%, and license revenue rose 25%, showing that Arm’s growth is not just tied to one customer or one market.

Analysts expect Arm’s next quarter to continue the strong growth trend. Arm reiterated its Q4 fiscal 2026 guidance at its March “Arm Everywhere” investor event. Wall Street sees high-teens revenue growth YOY, with EPS declining accordingly as licensing deals roll into royalties.

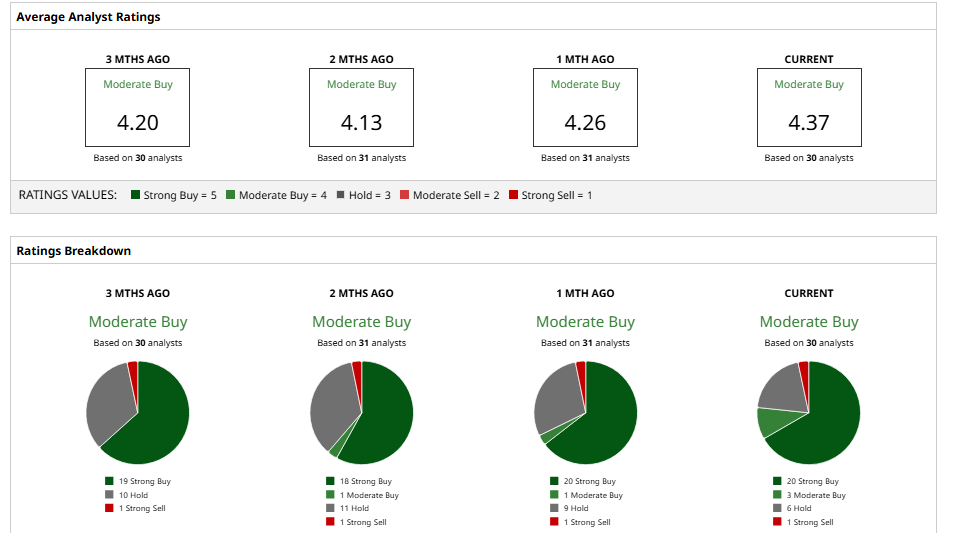

Wall Street analysts are overall bullish on ARM stock; 30 experts with coverage have an average “Moderate Buy” rating on shares. The mean price target of $172.15 indicates potential upside of 16% from current levels.

Notably, many analysts are quite optimistic on the stock. JPMorgan maintains a “Buy” rating with a $175 target, citing Arm’s expanding AI and data-center opportunities. In general, ARM’s strong growth profile earns it a buy-side bias, but the consensus assumes only modest further gains given the already high valuation.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)