/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

Space stocks have rarely felt this electric. SpaceX confidentially filed for an IPO that could value the rocket-and-satellite giant at $1.75 trillion, according to Bloomberg reports from April 1, 2026. Immediately after, NASA's Artemis II mission lifted off from Kennedy Space Center, sending four astronauts on the first crewed lunar flyby since Apollo 17.

Launch companies, lunar lander makers, and satellite operators all rose on the dual catalysts. Investors who own broad space ETFs watched their holdings gain ground in real time. So, let's turn to the company that could make this sector even hotter: Amazon (AMZN).

The Space Boom Is Just Getting Started

The numbers tell a clear story. SpaceX operates more than 10,000 active satellites through Starlink, per company disclosures. Amazon's Project Kuiper—rebranded as Amazon Leo—has roughly 180 satellites in orbit. That gap explains why Amazon wants to close it fast. Globalstar (GSAT) already runs a mature low-Earth-orbit network with ground infrastructure and globally harmonized spectrum. A deal valued near $9 billion would hand Amazon proven assets instead of building everything from scratch.

Globalstar's full-year 2025 revenue reached $273 million, up 9% from 2024. The company guided 2026 revenue between $280 million and $305 million with an adjusted EBITDA margin near 50%. Those figures may look small next to Amazon's scale, but they represent ready-made capacity in a market where every month of delay costs market share.

Amazon's Bold Move into Satellites

CEO Andy Jassy explicitly called low-Earth-orbit satellites one of the "seminal opportunities" for 2026 and guided total capital spending near $200 billion across the company. Acquiring Globalstar's spectrum and ground stations would accelerate Leo deployment without forcing Amazon to shoulder every dollar of new satellite manufacturing alone.

Apple (AAPL) holds a 20% stake in Globalstar from its $1.5 billion investment in 2024, which adds a negotiation wrinkle, but the strategic fit remains obvious: Amazon Leo could expand rural and mobile coverage while Starlink keeps adding customers.

What the Numbers Mean for AMZN Shareholders

Amazon trades at a trailing P/E of 29.26, with the stock closing near $209.77 and trailing 12-month EPS at $7.17. That multiple sits well below the company's 10-year median of 80.87.

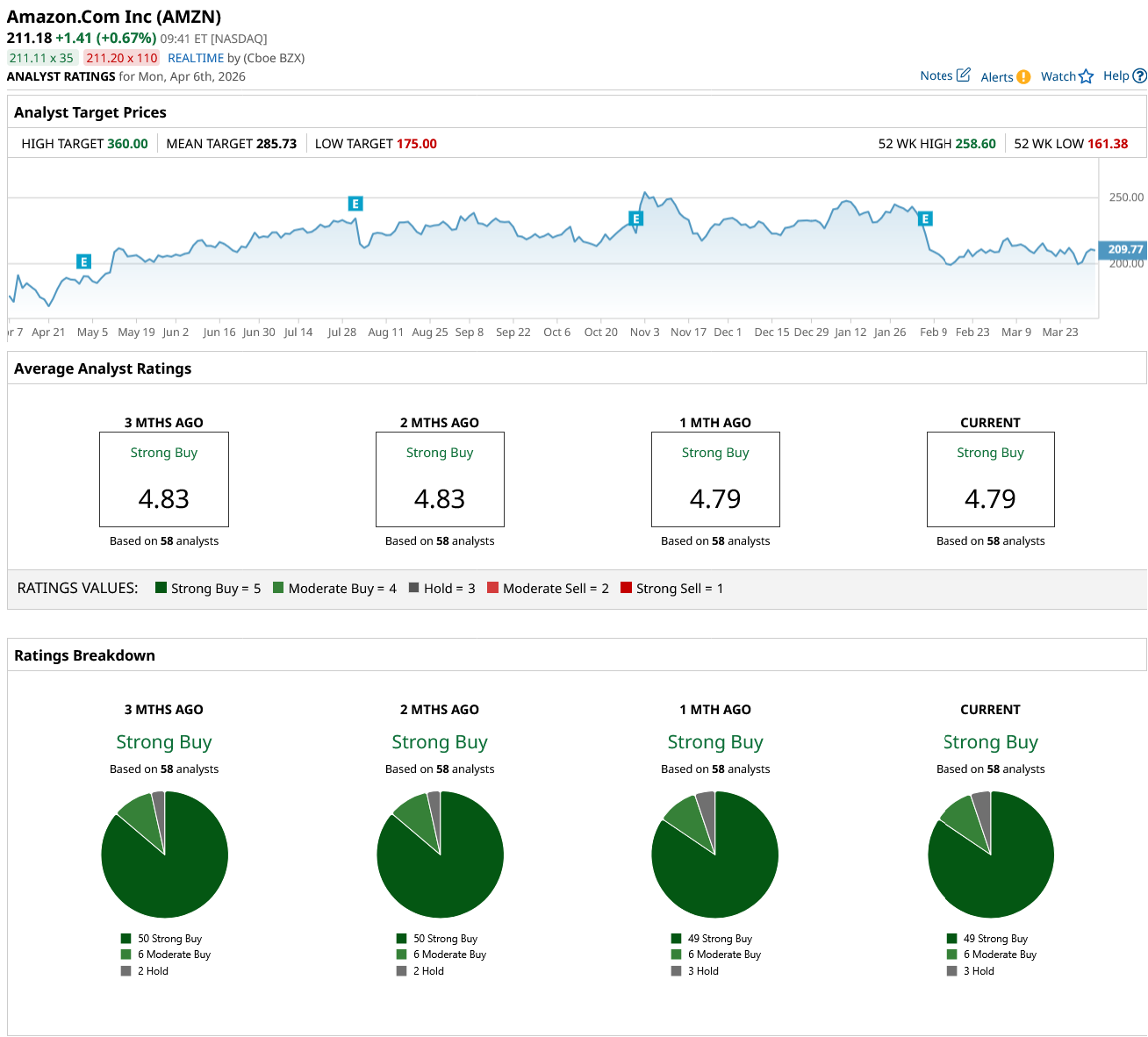

There are 58 firms covering the stock, delivering a consensus "Strong Buy" rating with 55 analysts rating it a "Moderate" or "Strong Buy." Only three rate it "Hold." The mean price target stands at $285.73, implying roughly 35% upside potential from current levels. Globalstar's five analysts rate it a "Moderate Buy," though its smaller size and higher volatility make it a different animal—its market cap recently crossed $9 billion after the news.

Compare the two: Amazon's advertising and AWS segments grew 23% and 17%, respectively, in Q4, funding the satellite push without crimping core profitability. A completed deal would not move Amazon's income statement much in 2026, but it could shorten the timeline to closing the gap with SpaceX's 10,000-satellite fleet.

That said, integration always carries costs. Globalstar's revenue remains a fraction of Amazon's, and regulatory approval for spectrum transfers could stretch into 2027. Amazon's $200 billion capital plan already pressures free cash flow in the near term. Yet the company's $139.5 billion in operating cash flow gives it plenty of dry powder, and the satellite business aligns with long-term AWS edge-computing goals.

Key Takeaways

All in all, Amazon's reported pursuit of Globalstar is less about one $9 billion check and more about buying time—and spectrum—in the fastest-growing corner of the internet. SpaceX's IPO and Artemis II have already lifted the entire sector; a successful AMZN-GSAT tie-up would give retail investors a direct, liquid way to own the next chapter.

For safety-focused investors who like Amazon's 12% revenue growth, 20% cash flow expansion, and sub-30 P/E, this move adds strategic depth without derailing the core earnings engine. Space stocks are hot right now. Amazon just handed long-term holders another reason to stay buckled in.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.