/Nike%2C%20Inc_%20logo%20by-%20Poetra_RH%20via%20Shutterstock.jpg)

Nike (NKE) stock crashed today after the footwear giant posted better-than-expected Q3 results but disappointed in terms of guidance, citing continued weakness in one of its key markets: China.

On the earnings call, management warned of another 20% decline in China revenue and $1 billion in projected tariff costs in the current financial quarter.

Year-to-date, Nike stock is now down more than 30% — a meltdown that Jefferies analyst Randy Konik dubbed a buying opportunity in his post-earnings research note on Wednesday.

Nike Stock Is Super Cheap to Own

Speaking this morning with CNBC, Konik said NKE shares are very attractive given they are now trading at a “cycle-low” price-to-sales (P/S) multiple of about 1.6x only.

According to him, while the recovery in China and Nike Digital may take time, the brand remains ubiquitous and fundamentally strong.

The good news is the progress being made in clearing excess inventory, particularly in the North American market, he added, calling it a precursor to broader recovery and future margin expansion.

Jefferies maintains a “Buy” rating on Nike, with a $110 price target indicating the stock could more than double from here over the next 12 months.

NKE Shares Are Oversold Currently

In its fiscal Q3, Nike successfully reduced total inventory by 1% on a year-on-year basis, signaling the aggressive discounting phase may finally be nearing an end.

The firm’s North American sales also grew 3% in the third quarter, driven by double-digit strength in high-performance categories like Running and Global Football.

More importantly, a 5% increase in wholesale revenue suggests NKE’s strategic pivot back to retail partners is gaining traction and could provide a more stable foundation for a late 2026 recovery.

From a technical perspective, Nike shares’ relative strength index (14-day) crashed to the early 20s today, fueling hopes of a relief rally in the near term.

How Wall Street Recommends Playing Nike

While not nearly as bullish as Jefferies, other Wall Street firms also recommend sticking with NKE stock in 2026, especially since they pay a healthy dividend yield of 3.66% currently.

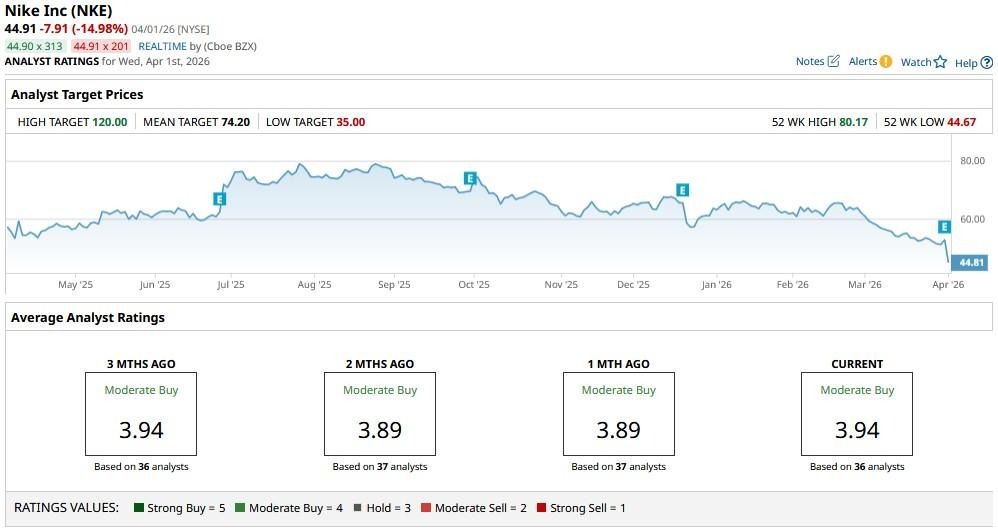

The consensus rating on Nike Inc remains at “Moderate Buy,” with the mean price target of about $74 indicating potential upside of more than 60% from here.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)