With aluminum prices surging back into the spotlight, the setup for producers like Constellium SE (CSTM) is becoming increasingly compelling. Benchmark prices have climbed to multi-year highs recently, around $3,400 to $3,500 per ton, driven by supply disruptions, tight inventories, and resilient end-market demand across aerospace, automotive, and packaging.

The latest leg higher has been driven by geopolitical risks in the Middle East, where disruptions to major smelters and shipping routes have put global supply at risk. The disruption of key shipping routes such as the Strait of Hormuz and smelter outages in the Persian Gulf have pushed regional premiums to multi-year highs and created uncertainty around physical availability.

Beyond near-term shocks, production growth remains limited due to China’s capacity caps and environmental restrictions, while elevated energy costs, particularly in Europe, continue to pressure smelting economics.

However, demand for aluminum is being supported by powerful long-term trends. The metal plays a critical role in electric vehicles, renewable energy infrastructure, and lightweighting across industrial applications, creating a steady and durable demand backdrop.

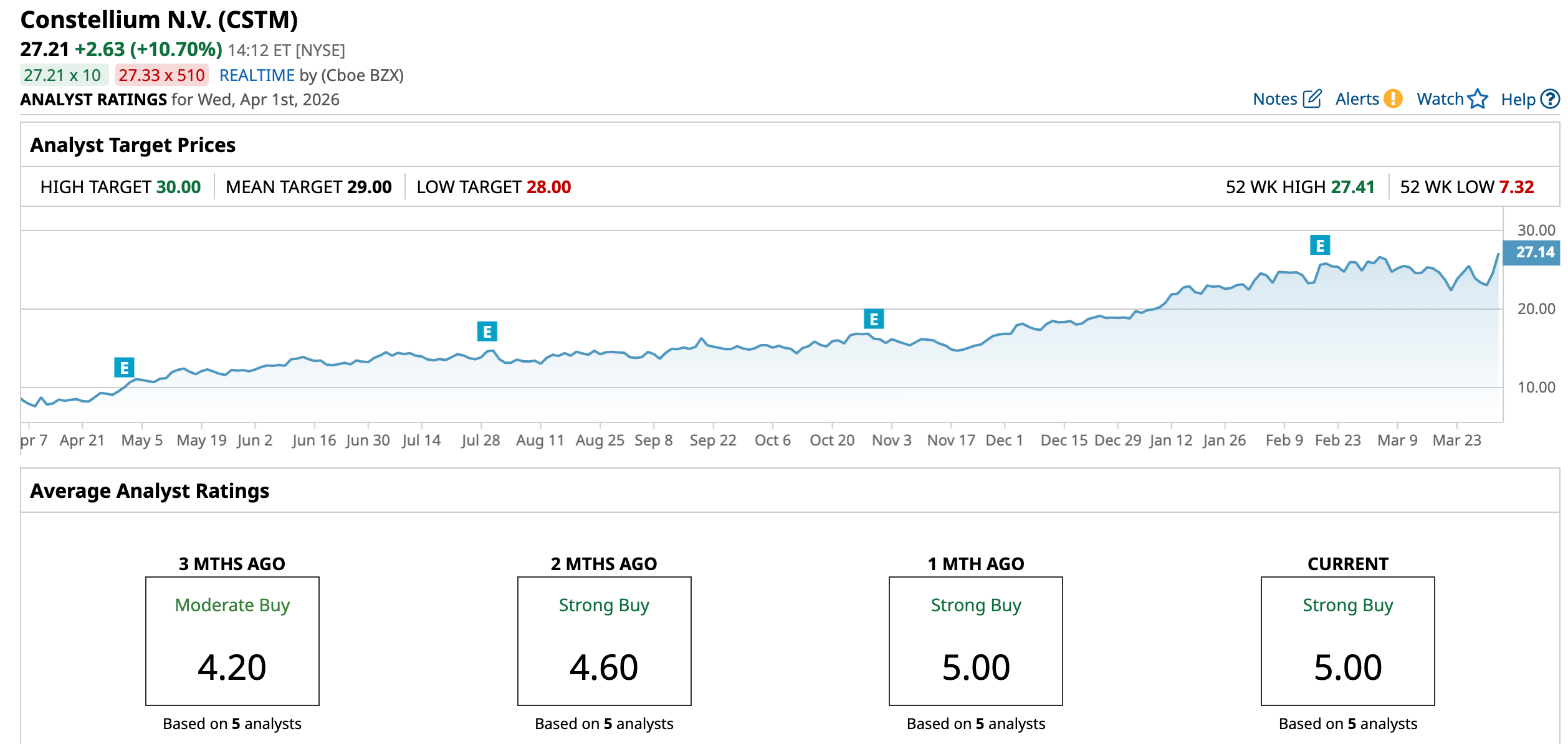

Against this backdrop, BMO Capital sees further upside in Constellium and maintains an “Outperform” rating, as elevated aluminum prices and improving product mix could continue to drive earnings momentum. With a Street-high price target of $30, the analyst implies 10% upside from current levels.

About Constellium Stock

Headquartered in Paris, Constellium SE is a global producer of rolled and extruded aluminum products, serving a diverse range of end markets including aerospace, automotive, packaging, and industrial applications. The company operates an extensive network of manufacturing facilities across Europe and North America, positioning it as a key supplier of high-value aluminum solutions. Constellium has a market cap of $3.3 billion.

Shares of Constellium have delivered a remarkably strong run over the past year, positioning the stock as one of the standout performers within the metals and mining space. Over the past 52 weeks, the stock has surged by 169.7%, driven by improving fundamentals, strong earnings execution, and a favorable aluminum pricing environment. This rally has been accompanied by multiple breakouts to new highs, with the stock touching $27.41 on Mar. 4, underscoring sustained investor momentum and confidence in the aluminum cycle.

On a year-to-date (YTD) basis, the performance has also been notably strong, with gains of 45%, highlighting continued upside. The stock has benefited from stronger-than-expected earnings, improving margins, and rising exposure to high-growth end markets such as aerospace and packaging, alongside tailwinds from elevated aluminum prices.

It is trading at 11.25 times forward earnings, which is below the sector average.

Stable Financial Performance

Constellium reported its fourth quarter and full year 2025 results on Feb. 18, which reflected both cyclical tailwinds from higher aluminum prices and meaningful operational improvements.

In the fourth quarter of 2025, the company posted revenue of $2.2 billion, representing a 28% year-over-year (YOY) increase, driven by higher shipments and improved pricing. Shipments rose 11% YOY to 365 thousand metric tons, highlighting solid demand across end markets. Moreover, net income came in at $113 million, compared to a net loss of $47 million in Q4 2024, marking a significant turnaround. Constellium reported EPS of $0.80 in Q4 2025, compared to a loss per share in the prior-year quarter. Adjusted EBITDA reached $280 million, up 124% YOY.

For the full year ended Dec. 31, 2025, Constellium’s revenue increased 15% YOY to $8.4 billion, supported by stronger pricing and modest volume growth, with shipments rising 4% to 1.5 million metric tons. More notably, profitability expanded significantly, with net income surging to $275 million from $60 million in 2024. Adjusted EBITDA climbed 36% YOY to $846 million. Also, cash generation improved materially, with free cash flow of $178 million, compared to negative free cash flow in the prior year.

Furthermore, for 2026 the company expects adjusted EBITDA to be in the range of $780 million to $820 million and free cash flow in excess of $200 million.

Analysts tracking CSTM project the company’s EPS to rise 6.8% YOY to $2.05 in fiscal 2026 and grow 16.6% to $2.39 in fiscal 2027.

What Do Analysts Expect for Constellium Stock?

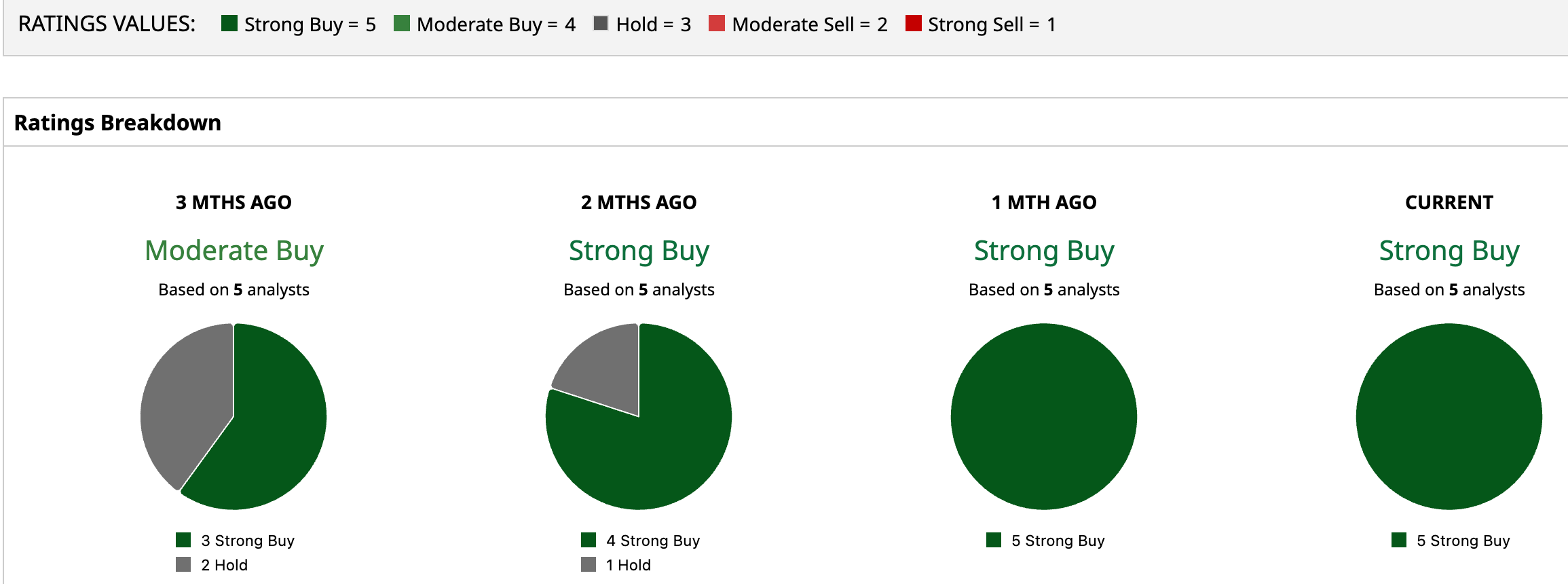

CSTM has a consensus rating of a “Strong Buy” overall. Each of the five analysts covering the stock has rated it a “Strong Buy.”

While CSTM’s average price target of $29 suggests an upside of 6.6%, the Street-high target of $30 signals that the stock could rise as much as 10.3% from current levels.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)