/Semiconductor%20by%20Gorodenkoff%20via%20Shutterstock.jpg)

Jensen Huang seems to have turned into Oprah this month, as the CEO of the chip titan is loosening his pockets quite generously to solidify its position as the leader of the AI revolution. Following investments of $2 billion each in photonics and optical networking majors Lumentum (LITE) and Coherence (COHR), the world's biggest company by market cap has now taken another $2 billion punt on custom AI chipmaker Marvell Technology (MRVL).

Under the terms of the partnership, Marvell will provide its XPUs to Nvidia (NVDA), while the latter will provide access to its vast AI ecosystem to the former. Sounding optimistic about the development, Marvell CEO Matt Murphy said, “By connecting Marvell’s leadership in high-performance analog, optical DSP, silicon photonics and custom silicon to NVIDIA’s expanding AI ecosystem through NVLink Fusion, we are enabling customers to build scalable, efficient AI infrastructure.”

About Marvell Technology

Founded in 1995, Marvell is an AI infrastructure semiconductor company. While its primary focus lies in building custom chips for hyperscalers, it also offers networking, telecom infrastructure, storage, and edge services.

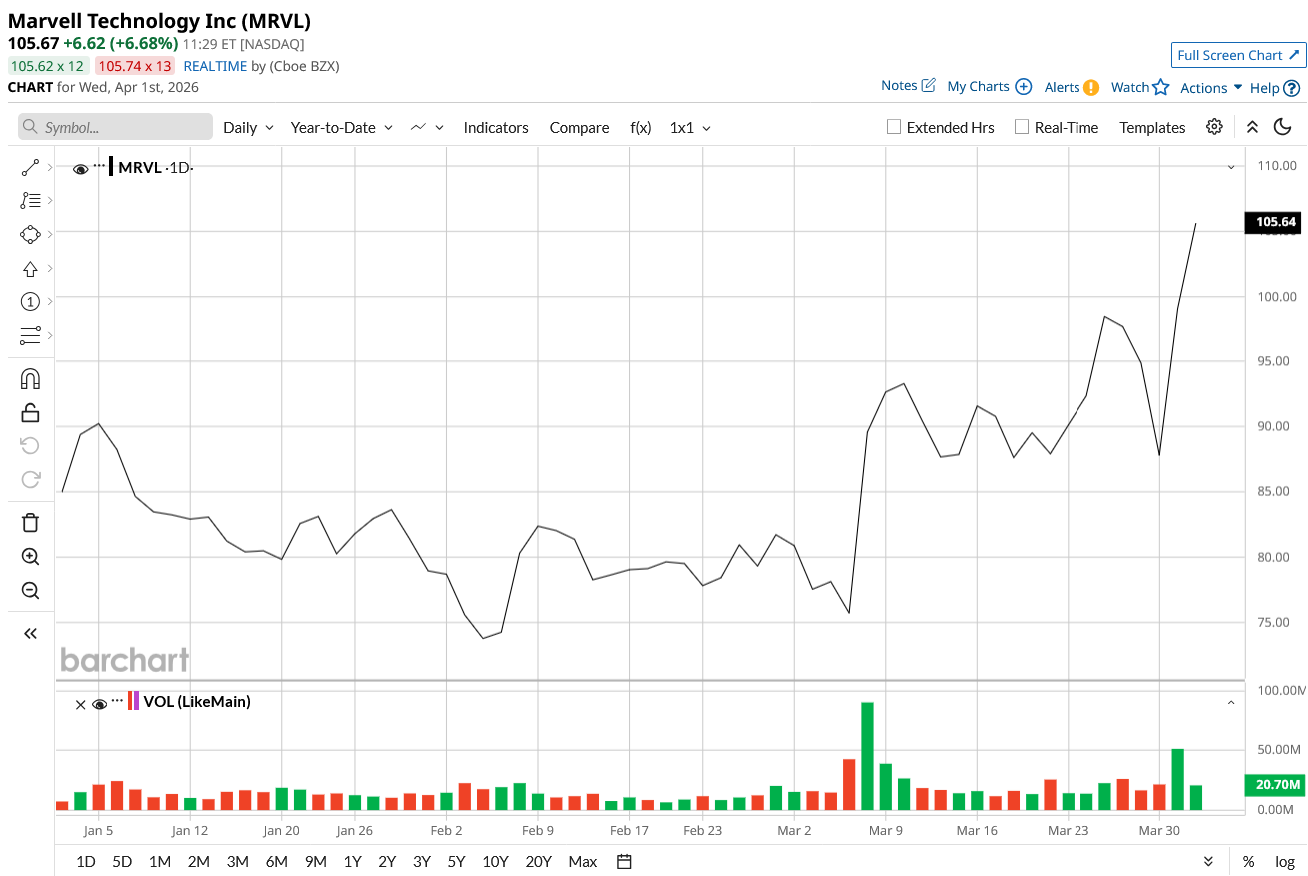

Valued at a market cap of $76.7 billion, MRVL stock is up 24% on a year-to-date (YTD) basis, with the bulk of it coming yesterday on the back of the investment news as the shares popped 12.8%. Moreover, the stock offers a modest dividend yield of 0.25%.

So, what is the broader strategy of Huang's latest move, and how does Marvell fit into it? More importantly, what does this mean for MRVL stock? Let's find out.

“Marvellous” Q4

Marvell had a fantastic Q4 as the company's revenue and earnings both surpassed Street expectations. While this was the second consecutive quarter of earnings beat from the company, over the past nine quarters, the company has reported a miss only twice. Moreover, the past 10 years have seen the company compounding its revenues at a CAGR of 12.15%.

Notably, the company reported record quarterly net revenues of $2.2 billion, up 22.1% from the previous year. Within this, data center revenues witnessed an annual growth of 21% to $1.65 billion as AI demand remained robust. Earnings came in at $0.80 per share compared to $0.60 per share in the year-ago period. Also, this was just higher than the consensus estimate of $0.79 per share.

However, net cash from operating activities slowed down to $373.7 million in Q4 2025 from $514 million in the prior year. An increase in accounts receivable and inventories to $640.2 million and $370.5 million from $30.5 million and $169.8 million were the primary reasons for this decline. Overall, the company closed the quarter with a cash balance of $2.64 billion, much higher than its short-term debt levels of about $500 million.

For Q1 2027, the company expects revenue to be in the range of $2.28 billion to $2.52 billion, while earnings are expected to be between $0.74 and $0.84 per share. The midpoint of the revenues and earnings would denote YOY rises of 26.6% and 27.4%, respectively.

Marvell Deserves It

Marvell is not much talked about when conversations are held about chipmakers, as, just like it is with AMD (AMD), Marvell seems to be the neglected sibling of Broadcom (AVGO) in the ASIC space. However, Jensen Huang certainly rates it highly.

Nvidia chose Marvell over Broadcom because the decision fundamentally comes down to platform control and future network architecture. Broadcom is a fierce competitor that actively pushes its own proprietary networking switches and comprehensive ecosystem components, directly threatening Nvidia's InfiniBand and Spectrum product lines. Partnering with them carries the immense risk of funding a rival behemoth that ultimately wants to dominate the entire data center stack.

Marvell operates quite differently as an incredibly capable and willing collaborator. They specialize in the exact optical interconnects and programmable data processing units Jensen Huang desperately needs to scale his massive GPU clusters. Notably, Marvell integrates its silicon photonics smoothly into Nvidia environments without demanding absolute ecosystem control, creating a symbiotic relationship rather than a hostile standoff.

Meanwhile, Marvell captures roughly 20% of the market but thoroughly dominates in modular flexibility and optical integration. While a Broadcom client gets locked into a rigid architectural path, Marvell provides open, flexible chiplet designs on cutting-edge 3nm nodes. When Broadcom generally wins the raw Ethernet switching bandwidth battle, Marvell consistently outperforms them in electro-optical conversion efficiency and customized compute, giving hyperscalers the freedom to build exactly what they want.

Looking ahead, Marvell's strategy centers entirely around their advanced optical networking pipeline. Traditional copper wires physically cannot handle the bandwidth required when tech giants string together thousands of AI accelerators. Marvell is aggressively cornering the market on next-generation 1.6T and 3.2T optical digital signal processors and silicon photonics engines that translate electrical signals into light.

Beyond optics, their custom ARM compute processors are seeing phenomenal adoption from cloud providers desperate for energy-efficient server infrastructure. Furthermore, their upcoming portfolio of PCIe data retimers, which maintain signal integrity across massive hardware clusters, perfectly positions the company to extract billions in new revenue from the sprawling infrastructure buildout currently transforming the global technology landscape.

Analyst Opinion of MRVL Stock

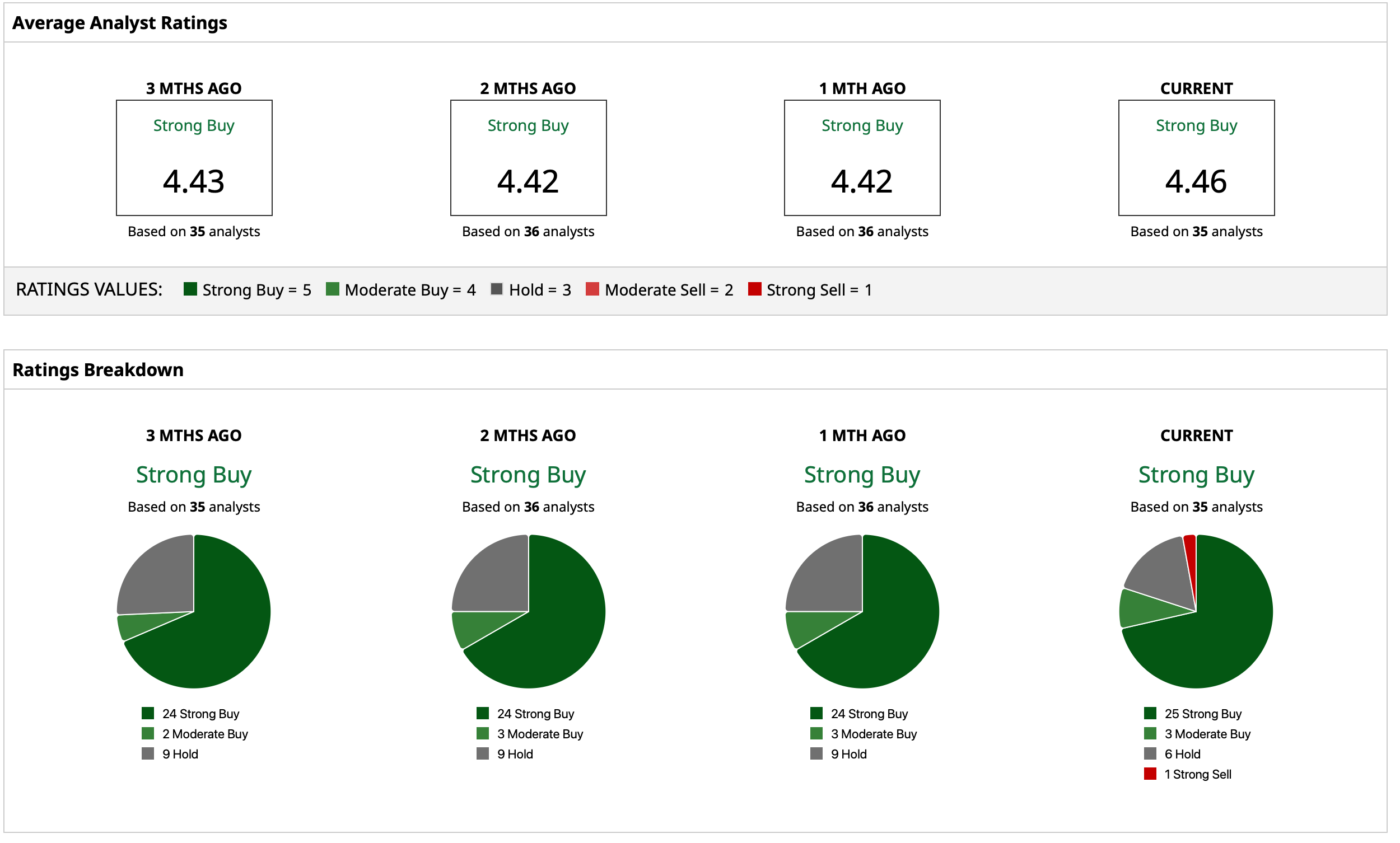

Thus, analysts have earmarked an overall rating of “Strong Buy” for MRVL stock. The mean target price of $119.53 indicates an upside potential of about 13% from current levels. Out of 35 analysts covering the stock, 25 have a “Strong Buy” rating, three have a “Moderate Buy” rating, six have a “Hold” rating, and one has a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)