Online travel stocks have had a rough stretch. The pandemic boom faded, Google’s (GOOG) (GOOGL) search changes reduced traffic, and AI has started reshaping how people plan trips. TripAdvisor (TRIP) has felt all of that pressure, with the stock falling roughly 30% from the start of 2026.

Then Bank of America came out with a new call that changed the conversation. The firm upgraded TripAdvisor to “Buy” and raised its price target to $15, which suggests about 50% upside from recent levels. The reason is not that TRIP has suddenly become a pure growth stock. It is that activist investor Starboard Value has built a 9.4% stake in the company and won board seats, giving it real influence over what happens next.

That matters because BofA believes Starboard could push TripAdvisor toward major strategic moves, including selling or spinning off assets like Viator and TheFork. Some estimates put the value of those businesses at around $2.5 billion combined.

For a stock trading near depressed levels, that is enough to get Wall Street’s attention.

A Travel Company With Two Very Different Stories

TripAdvisor is still best known as a travel review and booking platform, but the business has changed over time. Today, it has three main pieces: the legacy hotels and other bookings business, Viator for tours and activities, and TheFork for restaurant reservations.

That split is important. The old hotel business is the weakest part of the company. Google and AI-driven travel search tools have taken traffic away, and bookings in that segment continue to shrink. In the most recent quarter, the hotels and other businesses fell about 15%. To tackle this, the company launched an AI-driven planning tool in Q4, an AI-native MVP to boost engagement on its sites. It also integrated Viator bookings with ChatGPT for hotel concierges hoping to ride the AI hype.

The newer marketplace businesses are doing better. Viator and TheFork are still growing, and management has been leaning harder into those units as the future of the company.

That is why Starboard’s involvement is interesting. Activists tend to look for situations where the market is undervaluing pieces of a company. In TripAdvisor's case, the newer assets may be worth much more on their own than the market is currently giving them credit for.

A Tough Year for TRIP Stock

TripAdvisor’s stock has not been getting much love this year. TRIP began in 2026 in the mid-teens and has since fallen to around $10, leaving the shares down about 29% year-to-date (YTD). The decline has come as the ongoing war between Iran and the U.S./Israel has raised geopolitical tensions and driven oil prices higher.

This selloff, however, makes the stock inexpensive now. TRIP stock trades at about 6.5 times enterprise value to EBITDA and roughly 0.6 times sales, both of which are low compared with many travel-service peers. Its trailing price-to-earnings ratio is around 34, but that number is distorted by this year’s weaker profit base.

TripAdvisor Misses Q4 Earnings Estimate

TripAdvisor’s fourth-quarter 2025 results mostly came in below analysts' expectations. Revenue came in at $411 million, essentially flat year-over-year (YoY). Experiences, the company’s tours and activities business, rose about 10% to $204 million. The Fork grew about 18% to $57 million. But the legacy hotels and other segments dropped to about $151 million.

Profitability was weaker. Adjusted EBITDA came in at $45 million, or about 11% of sales, and earnings fell sharply from a year earlier. Still, the company produced a healthy cash flow in 2025, with $245 million in operating cash flow and $163 million in free cash flow. It also ended the year with around $1 billion in cash and equivalents. That cash position gives TripAdvisor flexibility. It has been buying back stock, and it still has room to do more.

Looking ahead, management expects another year of modest revenue growth. The company guided Q1 2026 revenue to be down about 3% to 5% YoY due to soft seasonality and a tougher hotel comparison.

For full-year 2026, TripAdvisor targets low-double-digit growth in experiences and TheFork but high-teen declines in hotels. CFO Noonan said the company still expects its marketplace businesses, including TheFork, to drive about two-thirds of revenue by late 2026. Experiences alone are forecast to be over 50% of sales by year-end.

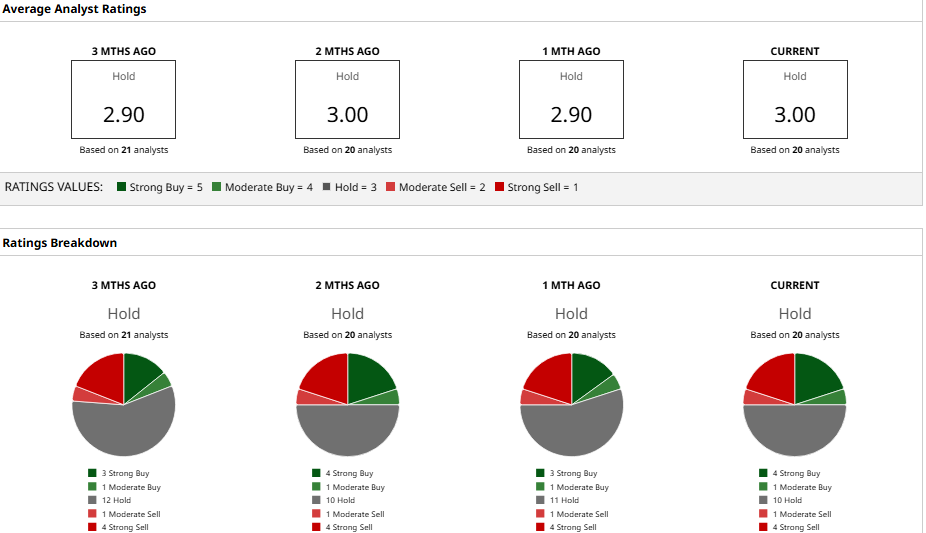

Analysts Opinion on TRIP Stock

Wall Street remains divided on TripAdvisor following the activist news.

As noted earlier, Bank of America’s Nafeesa Gupta recently turned bullish, upgrading to “Buy” with a $15 target. She argued that Starboard could push for a sale or spinoff of Viator and TheFork, unlocking hidden value.

Likewise, Goldman Sachs kept a “Buy” rating but lowered its target to $22, which is still about double today's price, citing near-term weakness while maintaining a long-term positive view.

Barclays struck a bearish pose, cutting its target to $10 with an “Underweight” rating, pointing to ongoing declines in the core hotels business. Similarly, UBS trimmed its target to $16 with a “Neutral” stance after the fourth-quarter earnings miss.

According to Barchart, the consensus is “Hold,” and the average 12-month price target among 20 analysts is about $15, which suggests an expected nearly 50% upside potential from the current price.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Rocket%20launching%20into%20space%20by%20BEST%20BACKGROUNDS%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Close-up%20shot%20of%20Rivian%20R1T_%20Image%20by%20Trong%20Nguyen%20via%20%20Shutterstock_.jpg)