"Oh crap. What do they know that we don't know?"

Nothing! To be very clear: We are not writing about bear markets today because we think a bear market is nigh. Could we be in the midst of one even as we speak? Technically, yes. But while stocks have been sagging of late, the level that the S&P 500 would need to hit to officially be in a bear market is still quite a ways away (for now). Besides, we're not in the business of making calls.

No, we're writing this for two reasons:

- The best time to absorb information about how bear markets work, and how to deal with them, is before you're thigh-high in one.

- People tend to pay more attention to bear-market screeds when the market is going through a bit of turbulence.

Check, and check.

So, let's talk about bear markets. We'll start by defining them (weirdly, not as straightforward as you'd think!), explaining how they work, then discussing how they impact investors—including a few less obvious effects that many people don't think about.

The Tea: First things first ....

What exactly is a bear market?

Let's start by defining not just a bear market, but also two other terms related to stock declines:

- Correction: This is a technical term that refers to a drop of 10% or more from a high.

- Bear market: This is a technical term that refers to a drop of 20% or more from a high.

- Crash: This is a general term that refers to a rapid and steep drop in prices. There is no specific threshold.

"I knew that!" You might, but a lot of people don't—especially as it pertains to what a crash is. Throughout our careers, we've been asked several times, "At what price has the S&P 500 officially crashed?"

The answer is that there is no concrete answer. It's just something you feel in your bones.

Young and the Invested Tip: Some funds historically do well in bear markets, while others are literally designed to benefit from them. Here's our look at 10 bear-market ETFs.

Any other rules?

Yes. Corrections and bull/bear markets are measured on a closing basis—you don't use intraday prices.

For example: If the S&P 500 trades as high as 6,600 during the day but closes at 6,550, we ignore 6,600 and use 6,550.

So, are we in a bear market now?

We already let the cat out of the bag on this one: No, we are not in a bear market.

When market watchers gauge whether U.S. stocks are in a correction, or in a bull or bear market, they typically use the S&P 500. They used to use the Dow Jones Industrial Average, but the much more broad-based S&P 500 is considered a better representation of America's diverse business base.

Well, the S&P 500 hit a record closing price of 6,978.60 on Jan. 27.

A 20% drop from 6,978.60 would put us at 5,582.88. So the S&P 500 would officially be in a bear market if we closed at or below 5,582.88.

It hasn't yet, of course. Not even close. The index's lowest day-end print since then was on March 27, when we closed at 6,368.85, which comes out to a decline of nearly 9%.

That’s close to being a correction—but it’s not yet halfway to being a bear market.

How do bear markets end?

Everyone generally agrees on the rules over when a bear market starts: the high.

We calculate the 20% decline necessary for a bear market from the market's peak. So logically, the start of a bear market has to be that peak.

Thus, if we do fall to or below 5,582.88—before the market rebounds above the Jan. 27 market high—then Jan. 27 will be considered the start of the bear market.

Everyone also generally agrees that the end of a bear market (and the start of a bull market) is when prices hit their lowest point.

Young and the Invested Tip: Volatility and lower prices often go hand in hand, which is why some investors protect themselves with low- and minimum-volatility funds like these.

Where people tend to disagree is when the end of a bear market is confirmed.

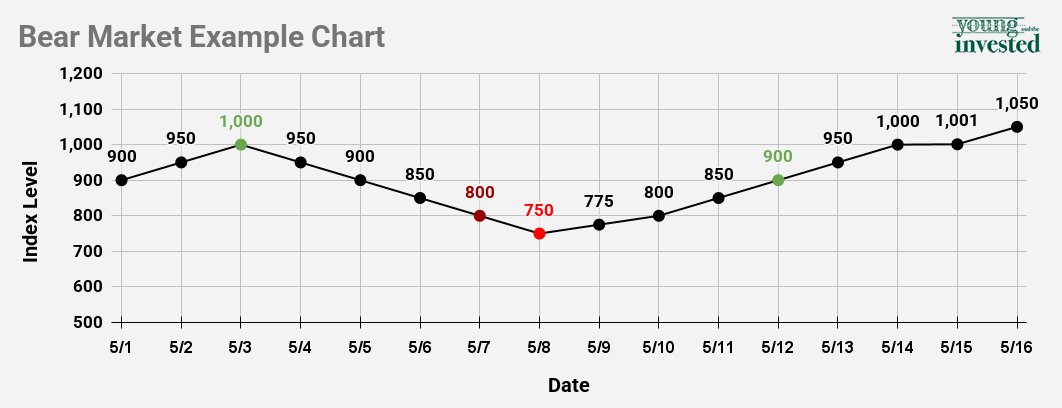

Some would say it's confirmed once the investment has risen 20% off the bear-market low. What would that look like? Well, consider the chart below, which is just an example index using hyper-simplified numbers:

Based on this definition …

- The bear market started on 5/3, when the index closed at 1,000.

- The bear market became a bear market on 5/7, when the index closed at 800, which is 20% below from the 5/3 index peak of 1,000.

- The bear market bottom was 5/8, when the index closed at 750.

- The 5/8 end of the bear market (and start of a new bull market) was confirmed on 5/12, when the index closed at 900, which is 20% above the 5/8 index low of 750.

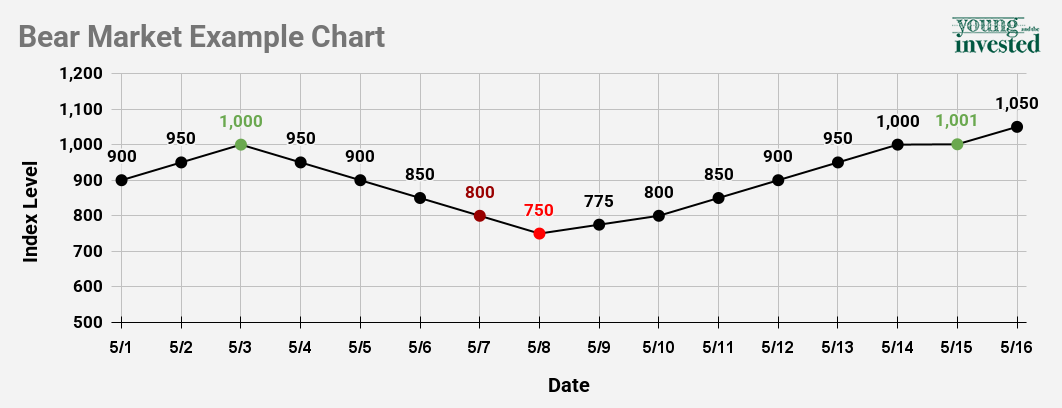

However, we follow the more common view that a bear market ends once the investment eclipses its previous peak. And here's what that would look like:

Based on this definition …

- The bear market started on 5/3, when the index closed at 1,000.

- The bear market became a bear market on 5/7, when the index closed at 800, which is 20% below from the 5/3 index peak of 1,000.

- The bear market bottom was 5/8, when the index closed at 750.

- The 5/8 end of the bear market (and start of a new bull market) was confirmed on 5/15, when the index closed at 1,001, which is above the previous index peak of 1,000 set on 5/3.

How common are bear markets?

"Bear markets can be painful, but overall, markets are positive a majority of the time," Hartford Funds writes in an analysis of S&P 500 performance between 1929 and 2024. "Of the last 95 years of market history, bear markets have comprised only about 21.4 of those years.

"Put another way, stocks have been on the rise 78% of the time."

How long do bear markets last?

A lot shorter than bull markets, that's for sure.

"For those of us getting older, we like to say that age is just a number," Ryan Detrick, Chief Market Strategist of Carson Group, wrote during the fourth quarter of 2025. "Bull markets like to say that as well. In fact, looking at the 11 bull markets since World War II, the average one lasts more than five years.

"Going back 50 years, the five bull markets that made it into their third year [like the one we're currently in] lasted an average of eight years total, and the shortest was five years."

By comparison, the average bear market lasts a little more than a year.

The Take: Now that we're done with the definitional work, let's talk about practical steps for investors when they find themselves in the midst of a much bigger drop.

What should I do in a bear market?

I'll start with something we say all the time, and that should be obvious by now:

How you should respond to a bear market is largely determined by your risk tolerance, time horizon, and investment goals. We simply can't tell you with certainty the specific actions you should take in a bear market.

There is some general advice out there that tends to be helpful, but there are significant caveats depending on your specific financial situation. Here are the two most common tips you’ll come across, and our thoughts on both:

1. Don't Panic-Sell

Study after study shows that people who panic and sell during a bear market tend to underperform investors who remain invested.

It seems counterintuitive. If you sell during a bear market, before the market hits its low, you would avoid some of the losses, right?

Sure. But people who jump out of the market in fear are often slow to return to the market, too, and in many cases, whatever outperformance they gained by getting out early is trumped by the gains they miss by returning to the market long after it has begun to bounce back.

Young and the Invested Tip: If you're in dire financial straits, you might not want to sell off positions … but you might want to temporarily slow or stop your contributions to retirement plans.

In other words: Many people are best served by simply sticking it out and not touching their portfolios.

But that doesn't mean you should never sell during a bear market. Sometimes it makes sense. And sometimes people have to.

Let's say you have a high schooler who's about to go to college. You're going to pay for their tuition using a 529 account you opened. Well … what happens if you're in a bear market? Do you tell your kid, "Sorry, you need to wait a year or two for stocks to return to a bull market"?

Or what if you're retired and rely on your 401(k) or IRA for income that pays your monthly bills? Do you call up the utility company and say, "Sorry, no can do this month. Haven't you checked the S&P 500 lately?" Of course not. Sometimes you need that income no matter what.

In fact, once you get to a certain age, some retirement plans force you to take required minimum distributions (RMDs), so you don't even get a say—you'll generally have to sell positions to take that required withdrawal.

And this is what makes bear markets so painful.

Your market experiences are different from everyone else's. If you're in your 30s and 40s and don't have any kids, and you know a little bit about previous bear markets, you probably look at the potential of a bear market like this: "Yes, this is unfortunate, but the market always bounces back. I'll be fine!"

That's because you have decades before you'll ever need to touch your portfolio.

But other people aren't so lucky. Even a short bear market, followed by a rapid recovery, can prompt painful decisions about sending kids to college, beginning a retirement, or getting essential bills paid while retired. And the longer the bear market and the recovery, the more painful the consequences can be.

2. "Buy the Dip"

If you love a company before a bear market, and then its stock price is reduced by 20% even though the company remains strong and you believe the economy will land on its feet … by all means, you should buy shares in that company while that stock is on sale!

Heck, if you feel that way about the whole American economy, it's a chance to buy the S&P 500 or other broad-based indexes on the cheap (through funds).

"Buying the dip" can be a fantastic strategy.

But everyone can't do it. And sometimes, it's not worth the cost.

We have a skewed view of dip-buying because of our past two bear markets, which were historically unusual, as far as individual investors are concerned. During the 2020 COVID bear market, millions of Americans suddenly found themselves with a sudden, unexpected source of cash—stimulus checks—that they could use to buy the sudden dip in stocks. And they did! 2020 and 2021 saw Americans open record levels of brokerage and retirement accounts.

By the time 2022's bear market started roaring, the government wasn't issuing any additional stimulus, but many Americans still had ample savings. They put that to work, but the recovery wasn't nearly as fast as what we saw in 2020.

Fast-forward to 2026, and Americans' savings have been bleeding thanks to a couple years of high inflation. Few people have extra cash just lying around.

Think about your own portfolio. Do you have a portion of it set aside in cash just waiting to be spent during a bear market? If so, great, but many people—especially those with few assets in the first place—put every cent they have to work. So, if you're one of those people, what exactly do you buy the dip with?

You could sell some of your positions. In fact, if you look at your portfolio and see that some of your holdings suddenly look a lot less promising than they once did, you could sell those positions to buy new ones. But that—reviewing your portfolio and weeding out companies that no longer look attractive—is something you should be doing on a regular basis anyways.

However, if you indiscriminately liquidate positions to raise cash … you're just selling the dip to buy the dip, which means you're not getting ahead.

—

As always, thank you for reading, and we look forward to talking again next week!

Riley & Kyle

Like what you're reading but not yet a subscriber? Get our weekly financial insights and updates delivered to your inbox every Saturday morning by signing up for The Weekend Tea today! You can also follow us on Flipboard for more great advice and insights.

/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)

/Tesla%20Inc%20logo%20by-%20baileystock%20via%20iStock(1).jpg)