/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

Alphabet (GOOGL) has had a rough few months. GOOGL stock is down about 20% from its 52-week high, dipping its toes into what Wall Street defines as a bear market. That raises a fair question for long-term investors: is this a warning sign, or a buying opportunity?

The answer isn't simple. But the fundamentals behind this pullback tell a more nuanced story than the price chart alone. The broader tech selloff has hammered AI-linked names in 2026. Macro uncertainty, concerns about the pace of return on AI investment, and antitrust pressure have all weighed on Alphabet's share price.

Alphabet's full-year 2025 revenue hit $403 billion, marking the first time the company has crossed that threshold, up 15% year-over-year (YOY). In Q4, consolidated revenue reached $113.8 billion, growing 18% compared to the same period a year earlier. Search, Alphabet's biggest revenue engine, grew 17% in the quarter. Google Cloud accelerated to 48% growth, finishing the year with an annualized run rate of more than $70 billion. Net income climbed 30% to $34.5 billion, and the company generated a record $164.7 billion in operating cash flow for the full year.

Alphabet's AI Business Is Expanding Its Moat

If there's one thing that came through clearly from both Alphabet's Q4 earnings call and CFO Anat Ashkenazi's recent appearance at the Morgan Stanley Technology, Media and Telecom Conference, it's that AI is no longer a promise.

Google Cloud's backlog surged 55% to $240 billion in Q4. That's committed future revenue from customers who have already signed deals. Nearly 75% of Google Cloud customers now use Alphabet's AI products, and they “use 1.8 times as many products as those who do not.”

Gemini, Alphabet's AI model, now has over 750 million monthly active users. The company sold more than 8 million paid seats of Gemini Enterprise in just four months after launch, while nearly 350 cloud customers each processed more than 100 billion tokens just in December.

The Gemini app is growing fast, too. One product update, a viral image-generation tool called Nano Banana, added 20 million new subscribers in roughly two weeks, as Ashkenazi noted at the Morgan Stanley conference.

Alphabet CEO Sundar Pichai said on the earnings call that queries in AI Mode run three times longer than traditional searches, and that daily AI Mode queries per user have doubled since launch in the United States. That's a sign of deeper engagement, not disruption.

The $175 Billion Question for GOOGL Stock

The one number weighing heavily on investor sentiment is capital expenditures. Alphabet plans to spend between $175 billion and $185 billion on capex in 2026, roughly double the $91.4 billion it spent in 2025. And with higher spending comes higher depreciation flowing through the income statement. In 2025, depreciation already rose by nearly $6 billion to $21.1 billion.

Ashkenazi has been direct about this. "We need to have these efforts in place on a regular basis so that we can have more money to reinvest in the business," she said at the Morgan Stanley conference.

The key counterargument is demand. Alphabet has consistently said it is supply-constrained, meaning it could sell more cloud services if it had more computing capacity. Investing now to meet that demand is the whole point.

For context, just over half of that AI compute spending is expected to go toward cloud customers this year.

Is GOOGL Stock a Buy Right Now?

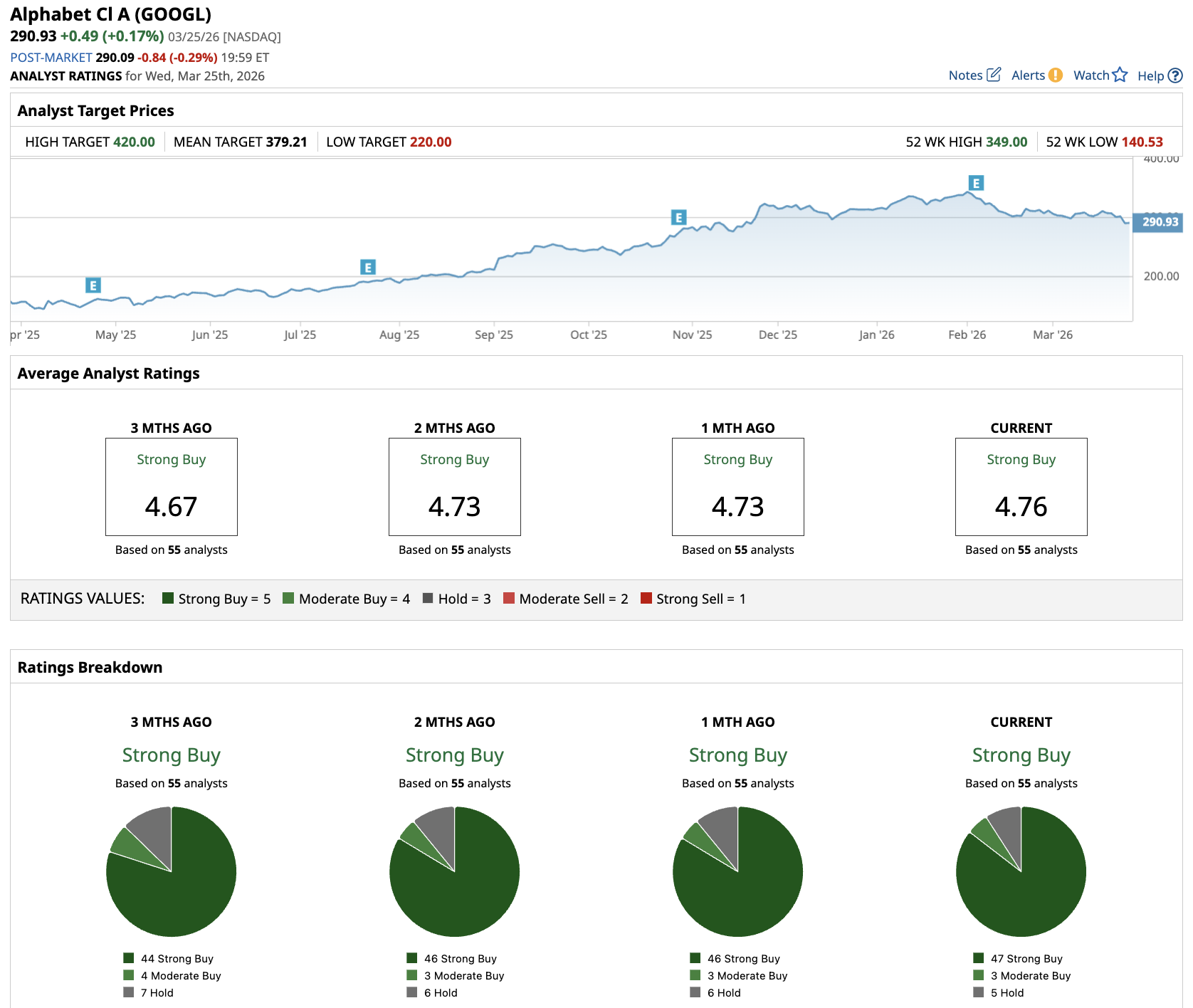

Well below its all-time high, Alphabet trades at a meaningful discount to where it was just months ago despite posting record revenues, record cash flow, and accelerating cloud growth. Out of the 55 analysts covering GOOGL stock, 47 recommend a “Strong Buy” rating, three recommend a “Moderate Buy,” and five recommend a “Hold” rating. The average price target is $379.21, implying potential upside of about 38% from the current levels.

The bear case for GOOGL stock is real — antitrust risk, rising costs, and the possibility of intensifying AI competition. None of those points should be dismissed.

But the bull case is backed by hard numbers. Record revenue. A $240 billion cloud backlog. Dominant search with expanding AI features. And a CFO who has made it clear that every dollar of Alphabet's massive capex budget is being tracked against returns.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)