/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

Artificial Intelligence (AI) stocks have been some of the market’s biggest winners over the past few years, but not every chipmaker is benefiting equally from the AI boom. Some names are still facing pressure from higher component costs, softer end markets, and shifting customer demand.

That is now putting Qualcomm (QCOM) in the spotlight after Bernstein downgraded the stock and cut its price target, saying investors may be better off owning actual AI winners instead. While Qualcomm still trades at a relatively cheap valuation, the firm sees weaker smartphone demand and rising memory costs as headwinds that could limit upside.

Bernstein points to what it calls “actual AI winners,” highlighting companies like Nvidia (NVDA) and Amazon (AMZN). Both rank among Barchart’s top-rated stocks and are widely viewed as key players powering the rapid expansion of AI infrastructure.

Nvidia (NVDA)

Nvidia remains the clearest pure-play AI leader in the market, and its business shows how quickly demand for AI infrastructure is expanding. The company sits at the center of the AI boom, with its GPUs powering training and inference workloads across hyperscale data centers. CEO Jensen Huang has described this moment as the "AI inflection point,” and has forecast that the chip revenue could reach $1 trillion by 2027. Its next-generation chips, such as Blackwell and Vera Rubin, are expected to drive this next wave of demand.

That strength shows up in the stock, too. Nvidia has roughly doubled over the past two years, yet the valuation still looks reasonable relative to its growth pace because of its recent pullback in 2026. The stock currently trades at a forward price-to-earnings (P/E) ratio in the low-20x range, which is in line with the sector median and well below its own five-year average despite the company’s explosive expansion.

The latest financial results help explain why Nvidia is a frontrunner in the AI category. The chip company posted a record $68.1 billion in revenue, up 73% year-over-year, including a record $62.3 billion from its data center segment, which surged 75%. Net income reached $42.96 billion, rising 94%, while earnings per share (EPS) climbed 98% to $1.76. For the full fiscal year 2026, revenue jumped 65% to $215.9 billion, and the company returned $41.1 billion to shareholders.

Looking forward, for Nvidia’s next fiscal year, Wall Street currently expects about $7.66 a share in earnings and $369.4 billion in revenue. These impressive numbers indicate 69% EPS growth and about 71% revenue growth year-over-year.

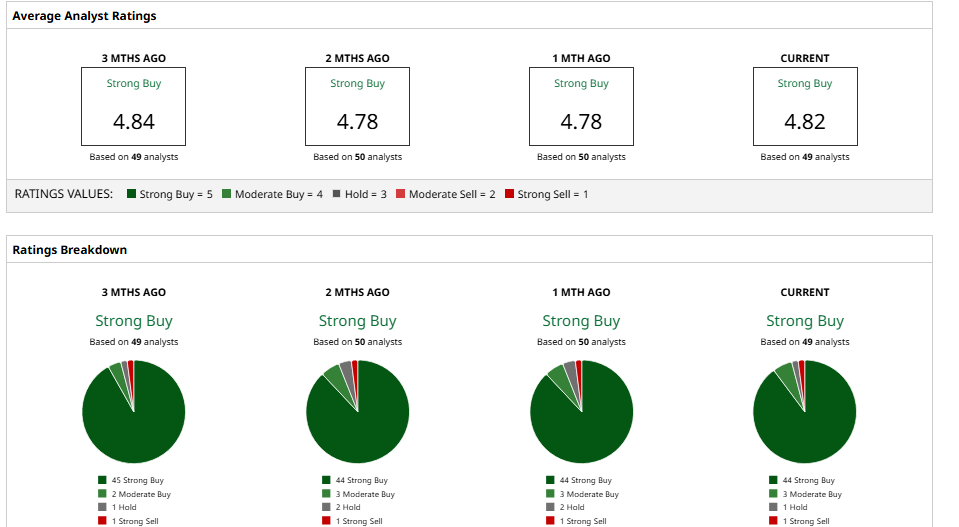

Analysts remain overwhelmingly bullish. Barchart shows a “Strong Buy” consensus rating on NVDA, with an average 12-month price target around $269, implying roughly 56% upside from current levels.

For me, NVDA;s performance has cemented its AI supremacy. Its growth is phenomenal, its margins are enormous at 75%, and it is close to monopolizing GPUs. NVDA should fit the criteria of any investor interested in AI exposure.

Amazon (AMZN)

Amazon is far more than an online retailer. Its AWS cloud business sits at the center of the AI race, and that gives the company a much bigger role in the market than its e-commerce roots might suggest. Amazon has become one of the key infrastructure players behind artificial intelligence, while also working with major AI firms and developing its own chips to support the next wave of demand.

Amazon is also pushing deeper into AI through cloud tools, custom chips, and autonomous agents designed to help customers automate tasks and build applications faster. The company is backing that strategy with heavy capital spending, including plans to pour about $200 billion into investments, mostly for AI data centers and related infrastructure, in 2026.

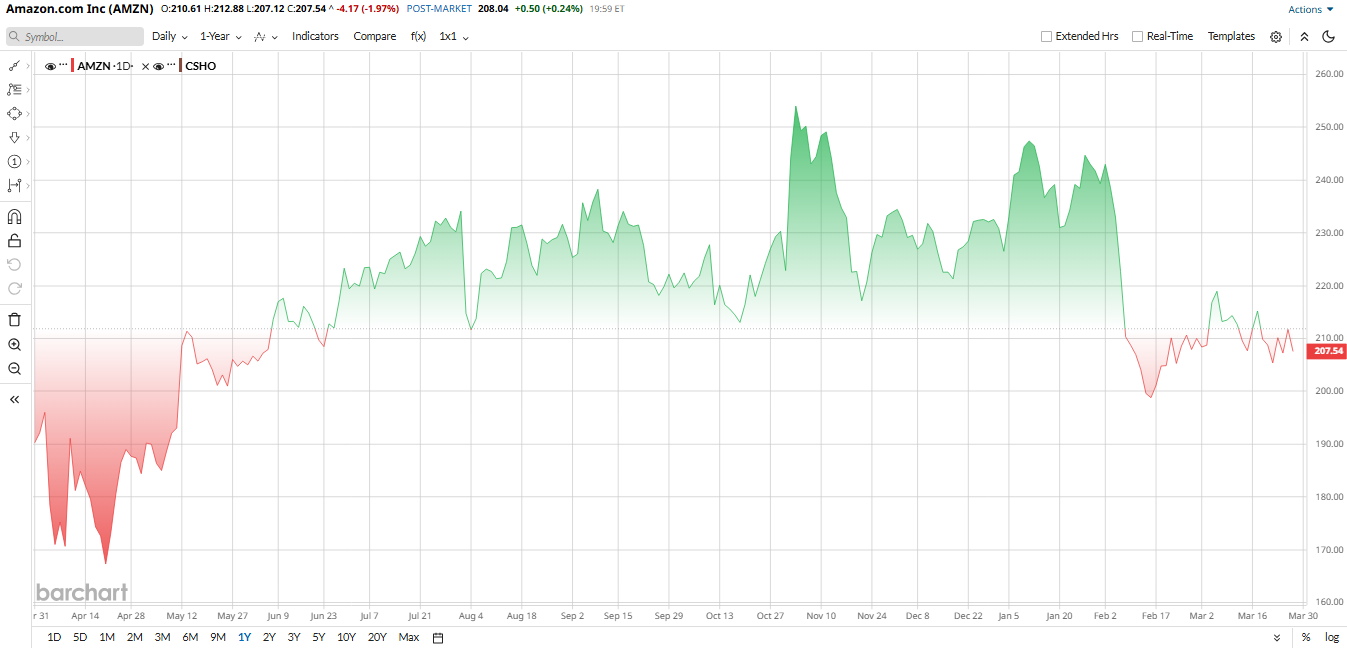

The stock, however, has not fully reflected that story, yet. AMZN shares are down about 10% year to date (YTD). They currently trade near $207, as investors worry about heavy AI spending. While the valuation is not cheap at about 26x forward earnings and roughly 3x sales, Amazon has a long history of spending heavily today to build a stronger business later.

The latest numbers help explain the optimism. In the fourth quarter of 2025, Amazon reported $213.4 billion in net sales, up 14% from a year earlier, while AWS revenue rose 24% to $35.6 billion. Net income reached $21.2 billion, and earnings per share (EPS) came in at $1.95, compared with $1.86 a year earlier. Free cash flow declined to $11.2 billion as capital spending increased, but Wall Street still sees meaningful upside driven by cloud and AI demand.

Looking ahead, the Wall Street consensus estimate for full-year 2026 is about $7.78 in EPS and $807.1 billion to $807.6 billion in revenue, representing 8% and 13% growth, respectively, year-over-year.

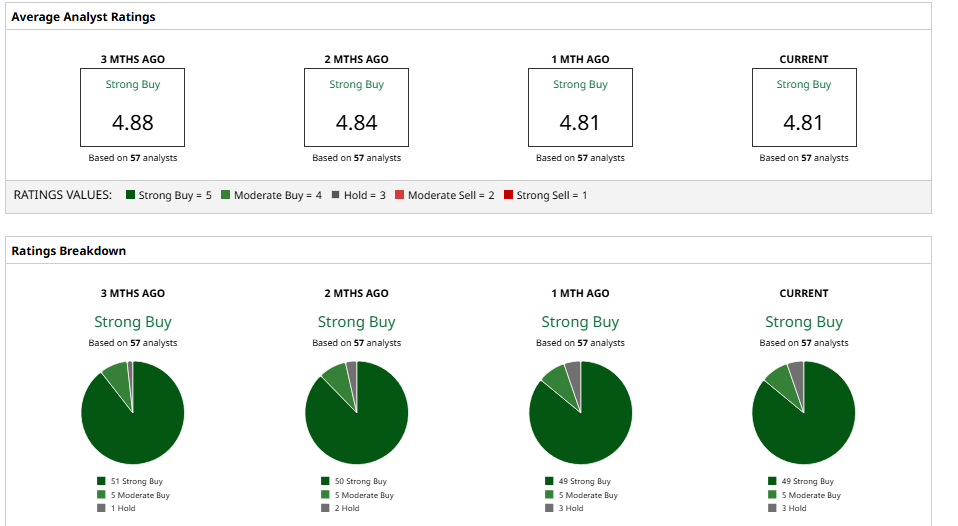

Overall, the consensus for Amazon on Wall Street is “Strong Buy,” with an average price target of about $287. That implies expected 38% upside potential over current levels.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Corning%20Incorporated%20on%20screen%20in%20front%20of%20website%20By%20Timon.jpeg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)