Geopolitical turmoil is in the driver’s seat, and it’s shaking up more than just oil charts. Rising tensions of the war involving Iran, Israel, and the United States have pushed crude prices sharply higher, breathing new life into energy stocks. Meanwhile, high-growth tech – especially artificial intelligence (AI) names – has started to feel the heat, as investors rotate toward sectors seen as more resilient in uncertain, inflationary environments.

And here’s the irony the market is slowly waking up to – AI does not exist in isolation. Every data center and chip runs on massive amounts of energy. Without that, the pace – and profitability – of AI expansion weakens. That dynamic is slowly making one wonder how it values energy relative to tech.

That brings us to Exxon Mobil Corporation (XOM). With its massive global production footprint and integrated model, Exxon has become a clear winner in this oil rally, with shares up by double-digit percentages in 2026, as higher crude prices flow straight into earnings strength. In fact, the oil company’s earnings multiple has climbed to levels that rival, and in some cases, even edge past, the chip giant NVIDIA Corporation (NVDA), the poster child of the AI trade. NVDA has stumbled, down about 8.18% this year after a stellar run that made it the world’s most valuable company. It’s a rare moment where energy is no longer the discounted trade.

And, that’s despite a massive market cap gap of around $4.34 trillion for Nvidia versus roughly $680 billion for Exxon.

With that shift in motion, where does XOM head next, and how should investors position themselves?

About Exxon Mobil Stock

Exxon Mobil is one of the world’s largest energy giants, operating across the full oil and gas value chain, from exploration and production to refining and petrochemicals. Based in Spring, Texas, the company blends scale with diversification, generating strong profits when crude prices rise through its upstream business, while its refining and chemicals segments provide steady, reliable cash flow. That balance helps Exxon stay resilient during volatile times, including geopolitical disruptions. Exxon remains a cornerstone of the global energy system, now also gradually expanding into lower-emission technologies while continuing to power economies worldwide.

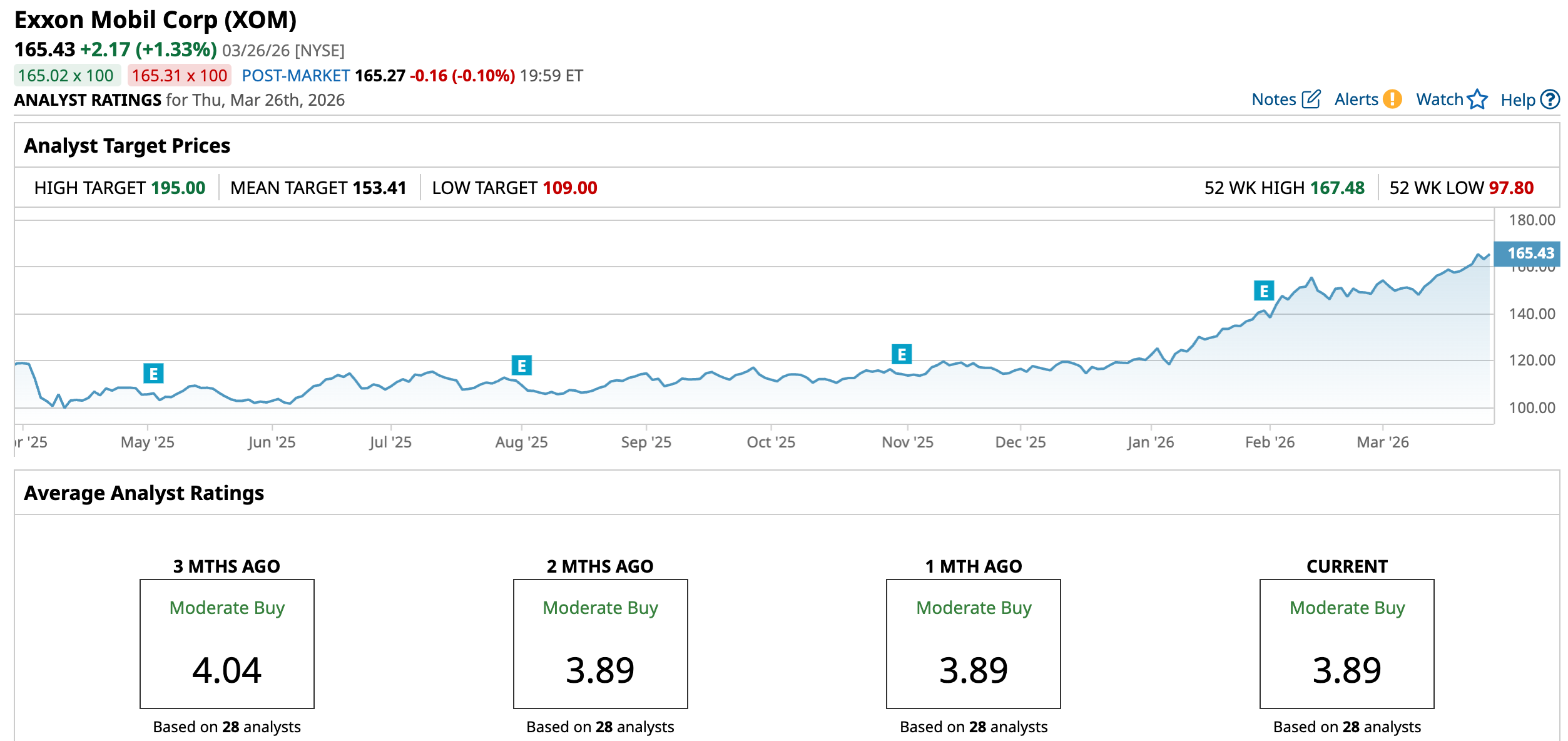

XOM has put together a strong, steady run over the past year, showcasing resilience that has turned into momentum. For much of the year, the stock moved gradually, reflecting the typical ups and downs of the energy cycle. But as we moved into 2026, the atmosphere shifted.

Rising geopolitical tensions and renewed interest in energy security sparked a sharp rally, pushing Exxon to new highs – about 21 times in 2026 alone – recently hitting a high of $167.48 on March 24. XOM stock rose 37.47% year-to-date (YTD) basis. Plus, over the past 52 weeks, the stock is up roughly 39.87%, with a strong 41.13% gain in just six months.

What stands out on the chart is how momentum has built. Volume has picked up, with more green bars showing stronger buying interest. The 14-day RSI is now hovering near the overbought zone, signaling that the rally has been powerful and fast, as readings above 70 often suggest stretched conditions.

Meanwhile, the MACD oscillator signals bullishness, with the MACD line holding above the signal line and the histogram staying positive, indicating the uptrend might still have fuel.

Valuation-wise, the XOM stock story gets interesting and a little surprising. One would expect an oil giant to trade at a discount. But right now, Exxon is doing the opposite. It’s trading at about 23.48 times forward GAAP earnings, a premium not just to its own history, but to the broader energy sector. Even its forward PEG ratio sits elevated around 1.5 times.

In comparison, those multiples are higher than the AI chip stock NVDA, priced at roughly 22.87 times forward GAAP earnings, and having a much lower forward PEG ratio of 0.57 times. In other words, XOM is being valued like a growth stock, while NVDA, despite its impressive AI story, looks relatively more “efficient” on a growth-adjusted basis. That’s a shift one doesn’t see often.

But Exxon’s case is not just about valuation, but also about what investors are getting in return. The company has paid dividends for 43 consecutive years and increased them for 27 years without a pause, earning its “Dividend Aristocrat” status. Earlier this month, it paid a $1.03 per share quarterly dividend, offering a forward annual dividend of $4.12, translating to a yield of around 2.49%. Exxon Mobil keeps things balanced with a payout ratio of around 57%, signaling it returns solid income to shareholders while still retaining enough cash to fund growth and stay resilient.

Massive cash flows allow Exxon to return billions through dividends and buybacks, while still investing in LNG and offshore projects. With a strong balance sheet and low breakeven costs, Exxon is not just riding oil prices, but is built to endure beyond them.

A Snapshot of Exxon Mobil’s Q4 Numbers

Exxon Mobil reported a fourth-quarter 2025 earnings result on Jan. 30 that showed both resilience and discipline. The company’s adjusted EPS rose 2.4% year-over-year (YOY) to $1.71 per share, coming in slightly ahead of Wall Street’s expectations. The strength came from higher production volumes and improved refining margins, even as lower crude oil and natural gas prices created some pressure. Revenues came in at $82.3 billion, slightly below last year’s $83.4 billion, but still ahead of estimates, signaling solid operational momentum.

Upstream production stood strong at 4.7 million oil-equivalent barrels per day, with unit earnings more than doubling compared to 2019 levels on a constant price basis. Exxon also executed all 10 of its key projects planned for 2025, reinforcing its long-term growth pipeline.

Geographically, Guyana and the Permian Basin stood out. In Guyana, Exxon continues to set new industry benchmarks, with the Yellowtail project coming online ahead of schedule and lifting Q4 production to around 875,000 barrels per day. In the Permian, the company hit a new quarterly record of 1.8 million barrels per day, contributing to Exxon’s highest annual upstream production in over 40 years at 4.7 million oil equivalent barrels per day. Technology deployment remains central to driving this efficiency.

The company generated $13.7 billion in operating cash flow and $5.6 billion in free cash flow. With $10.7 billion in cash and a manageable $34.2 billion in long-term debt, Exxon maintained a strong balance sheet. Further, it returned $9.5 billion to shareholders during the quarter, staying consistent with its capital return strategy.

Looking ahead to 2026, Exxon Mobil plans to stay on the front foot, with cash capital expenditures expected between $27 billion and $29 billion. And, it aims to buy back up to $20 billion worth of shares, depending on market conditions. Production remains a key driver, with the Permian projected at 1.8 million barrels per day, helping total upstream production to reach around 4.9 million in fiscal 2026.

Meanwhile, analysts anticipate Exxon Mobil keeping things steady, with EPS expected to inch up to about $7.04 in fiscal 2026, followed by a stronger annual jump of nearly 18.5% to $8.34 in 2027.

What Do Analysts Expect for Exxon Mobil Stock?

The outlook around XOM stock is starting to lean more confident, but with a clear note of caution. Bernstein’s Bob Brackett recently raised the price target to $195, while maintaining an “Outperform” rating.

His view reflects stronger oil prices and refining margins, also acknowledging that the road ahead is not exactly predictable. Geopolitical tensions, especially the prolonged war, can keep energy markets tight for longer than expected. That uncertainty actually works in favor of energy stocks. So, the broader call right now is simple. Having some exposure to energy, including names like Exxon, could make sense in this kind of environment.

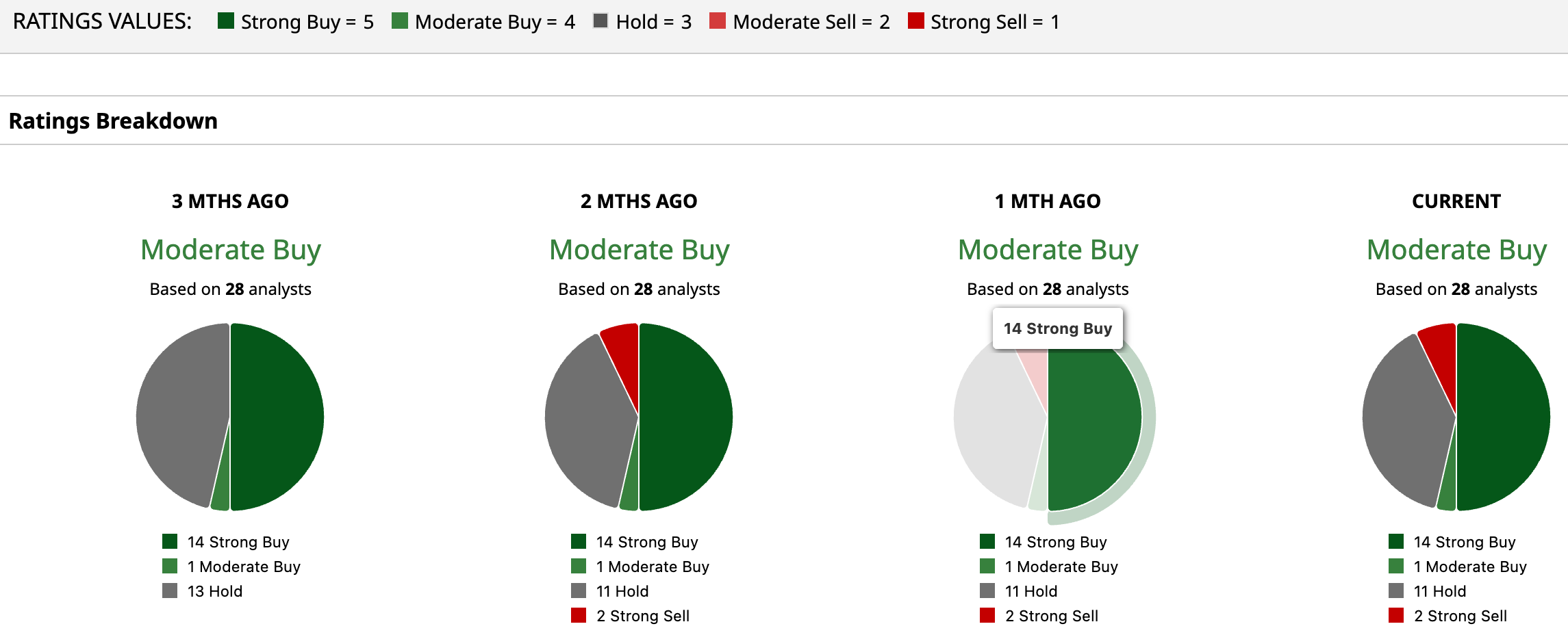

Overall, XOM has a consensus “Moderate Buy” rating from the 28 analysts covering the oil and gas stock. Among them, 14 advise a “Strong Buy,” one suggests a “Moderate Buy,” 11 analysts are playing it safe with a “Hold” rating, and the remaining two are outright skeptical with a “Strong Sell" rating.

While XOM currently trades above its average analyst price target of $153.41, Bernstein’s Bob Brackett’s Street-high target price of $195 suggests that the stock could rally as much as 17.9%.

Final Thoughts on XOM Stock

Exxon Mobil is not suddenly “bigger” than Nvidia, and that’s where a lot of the pushback originates. NVDA still commands a massive market cap versus Exxon’s. From that lens, the comparison can feel stretched, even misleading.

But the market is not only debating size, but also questioning what kind of earnings deserve a premium right now. Exxon’s profits, tied to elevated oil prices and global energy demand, look steady and immediate. NVIDIA’s, while still powerful, are tied to future AI growth expectations that have already been heavily priced in.

That’s what makes this moment interesting. Energy is reclaiming relevance in a world racing toward AI. Because behind every breakthrough, there is a layer of real-world infrastructure and energy keeping it alive.

For investors, the bigger picture is understanding that dynamic. At these levels, XOM reflects a market leaning into energy’s importance, leaving investors to decide how much of that story is already priced in.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Advanced%20Micro%20Devices%20Inc_%20logo%20on%20phone%20and%20website-by%20T_Schneider%20via%20Shutterstock.jpg)

/A%20concept%20image%20of%20a%20flying%20car_%20Image%20by%20Phonlamai%20Photo%20via%20Shutterstock_.jpg)

/Palantir%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)