/AI%20(artificial%20intelligence)/AI%20Infrastructure%20by%20FOTOGRIN%20via%20Shutterstock.jpg)

Billions of dollars just showed up at Synopsys’ doorstep, and the source is one of Wall Street’s most aggressive activists. Elliott Management has quietly built a multibillion-dollar stake in the chip design powerhouse, lighting a fresh spark under a stock that already sits at the heart of the AI hardware buildout.

Synopsys (SNPS) is no obscure niche name, playing a central role in the software tools used to design cutting-edge semiconductors. On March 23, SNPS shares climbed 3%, extending a strong run that has already pushed SNPS stock to fresh highs this year.

Now an activist with a reputation for shaking up technology companies is leaning in, and the market is starting to price in the possibility of higher margins, sharper execution, and a fresh chapter for this AI enabler. The only question is whether Elliott’s bold bet is a signal that you should follow, or a late entry into a crowded trade. Let's take a closer look.

Synopsys’ Financial Muscle

Headquartered in Sunnyvale, California, Synopsys develops software and IP that powers complex semiconductor and AI‑driven system design worldwide.

SNPS stock is priced near $410 as of this writing. Shares are down 13% year-to-date (YTD) and down 10% for the past 52 weeks.

The market capitalization sits near $79.6 billion, with SNPS trading at 41.8 times forward earnings versus a sector median of 21 times. Meanwhile, the PEG ratio of 3.52 stands well above the sector's average of 0.89, signaling that the market is already pricing in a richer growth trajectory.

Released in late February, the fiscal first‑quarter report showed net income of $65 million. That translated to EPS of $0.34 on a GAAP basis, reflecting the cost of ongoing investments and acquisition‑related charges. The report also highlighted adjusted EPS of $3.77, stripping out one‑time items.

The company posted revenue of $2.41 billion for the period, which topped Street expectations of $2.39 billion, reinforcing the idea that demand for Synopsys' design and verification tools remains strong even as some hardware names reset expectations.

However, the company also reported operating cash flow of $856.8 million, marking a 44% sequential decline and indicating weaker core operating performance compared to prior periods. Meanwhile, net cash flow stood at a loss of $759.4 million, reflecting a 24% seqeuntial improvement, suggesting improved liquidity management despite continuing overall negative cash movement during the month.

The Growth Levers Elliott Is Really Buying

Synopsys recently launched Ansys 2026 R1, its first major integrated release since the Ansys deal, combining AI, multiphysics simulation, and real‑world digital twin technology. This bundle integrates Synopsys VC Functional Safety Manager, QuantumATK, OptoCompiler, and other tools directly into Ansys workflows, tightening its grip on safety‑critical automotive, photonics, and materials‑heavy industries.

That push is complemented by a new Electronics Digital Twin Platform, an open solution that lets customers create and manage electronics digital twins in the cloud and validate up to 90% of automotive software before hardware even exists. This approach helps OEMs shrink development cycles and lower costs by shifting validation left, deepening Synopsys’ role as a core infrastructure partner.

Synopsys has also rolled out new ZeBu and HAPS platforms and capabilities that increase performance and capacity for AI‑era mega‑designs from the “data center to the edge.” These tools are designed to run “quadrillions of verification cycles” and catch subtle bugs earlier, which is critical for customers.

At the same time, Innatera — a neuromorphic computing startup focused on ultra‑low‑power edge AI — selected Synopsys simulation, PathFinder‑SC, and Totem to design brain‑inspired microcontrollers and validate power integrity and electrostatic discharge (ESD) robustness. That kind of design‑in at the edge complements Synopsys’ data‑center and automotive exposure and shows how its tools participate across the AI stack.

On the portfolio side, Synopsys has agreed to sell its Processor IP Solutions business to GlobalFoundries, shedding ARC CPU, DSP, NPU, and ASIP assets so it can focus IP resources on interface and foundation IP and higher‑value, AI‑driven opportunities from cloud to edge.

What Do the Pros Think SNPS Stock Is Worth?

The upcoming earnings release for investors watching Elliott’s new bet is scheduled for May 27, covering the quarter ending April 2026. For the current quarter, the average earnings estimate is $2.25, down from $2.59 in the same period last year. That translates to an expected year‑over‑year (YOY) decline of about 13%.

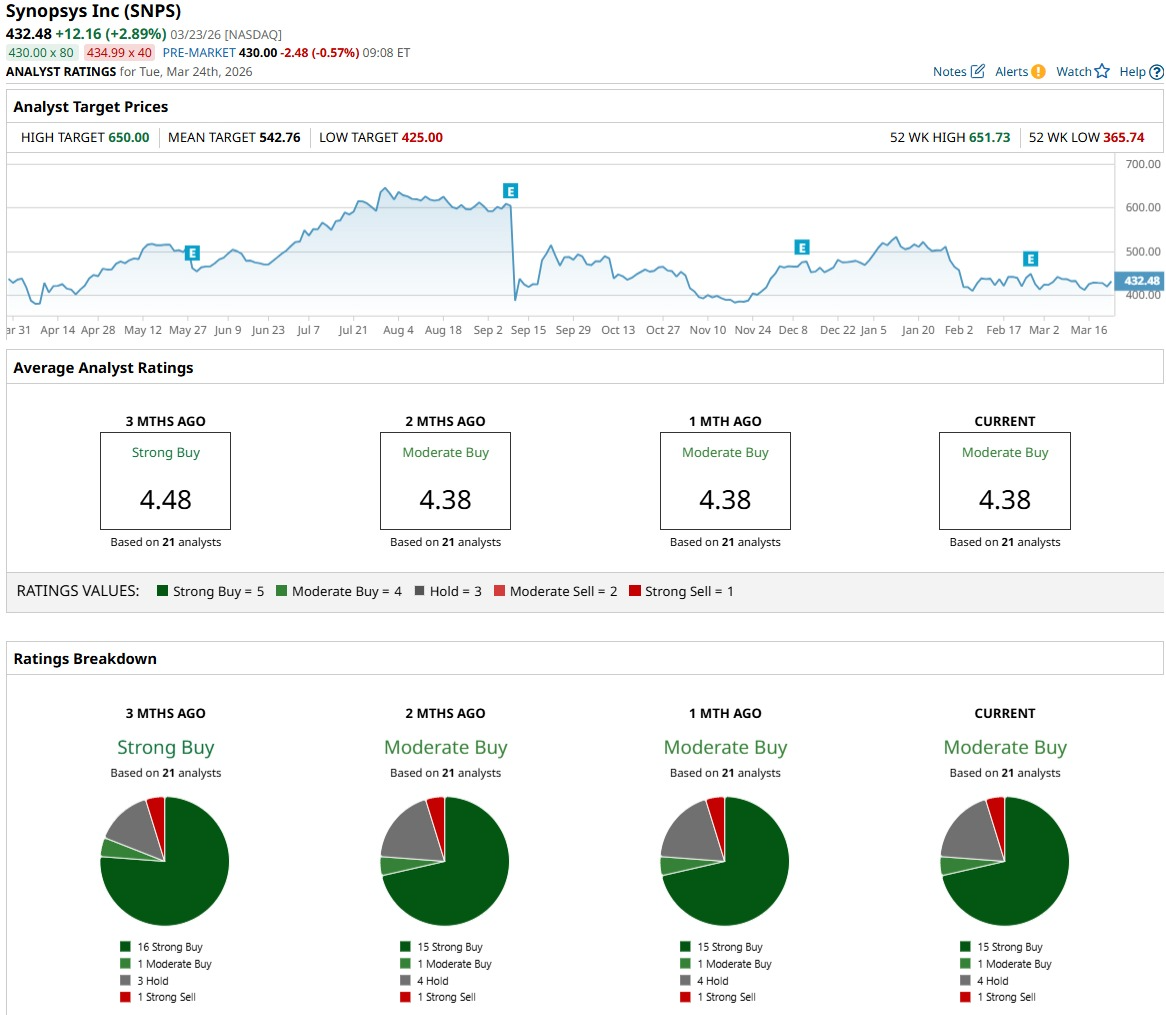

The consensus view from the 21 analysts following SNPS stock is a “Moderate Buy,” which is a strong vote of confidence. The average 12‑month price target sits at $542.76, implying roughly 33% upside from current levels, a sizable potential gain. This shows that Wall Street largely sees Elliott’s involvement as an extra layer of discipline and possible upside rather than a red flag.

Conclusion

Elliott is clearly betting that Synopsys’ AI and chip‑design moat can keep supporting a premium multiple, and the numbers mostly back that up. SNPS stock looks pricey on near‑term earnings, but long‑term growth drivers and a history of upside surprises still tilt the risk‑reward toward the bullish side. Over the next year, the direction looks more likely to be gradually higher than meaningfully lower, with any pullbacks attracting fresh interest.

For those comfortable with the valuation, SNPS stock still lines up as a buy rather than a sell.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20the%20SpaceX%20sign%20on%20a%20black%20building%20by%20IanDewarPhotography%20via%20Adobe%20Stock.jpeg)

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)