Target Hospitality (TH) is looking more and more like a completely different company. In fact, Oppenheimer recently upgraded TH stock to an "Outperform" rating from “Perform” with a price target of $11. The rationale behind the move is that Target's efforts to expand into remote lodging related to data-center development may provide a more exciting growth path. With shares now trading near $9.50, Oppenheimer's price target represents a potential gain of roughly 16% from current levels.

This shift didn’t happen overnight. The market is clearly starting to focus more attention to companies involved in the physical buildout of the AI space, and that includes power infrastructure, land acquisition, and workforce development in areas that are difficult to serve. That's exactly what Target Hospitality has been doing for the past year — repositioning itselft to address this space. Recent contract wins indicate that these efforts are finally starting to gain traction.

About Target Hospitality Stock

Target Hospitality provides modular accommodations, hospitality services, and other workforce housing solutions to customers across North America. Based in The Woodlands, Texas, the company has traditionally focused on the energy space as well as government-related markets. However, Target Hospitality is now looking to capitalize on what may be a much larger opportunity in workforce housing related to large-scale data-center development. With a market capitalization of $959 million, the company is still considered a relatively underfollowed small-cap name.

TH stock has quietly had a great run. The stock currrently trades near $9.50 per share, which is just shy of its 52-week high but well above its 52-week low. That means that TH has had a 59% run from its low and is within striking distance of its 52-week high of $9.90. That’s a pretty attractive setup, particularly when it’s driven by new business momentum rather than pure speculation.

Valuation is where things get more nuanced. While the firm is not yet profitable and thus doesn’t lend itself to a forward price-to-earnings (P/E) multiple comparison to peers, we can look to its price-to-sales (P/S) multiple of 2.89 times. While not cheap for a company with negative net margins, it’s not unreasonable if the firm's new data center and power community deal helps drive a multi-year rerating in its revenue quality and visibility.

Target Hospitality Misses on EPS But Finds Bigger Growth Catalysts

Target Hospitality’s fourth-quarter and full-year 2025 results were somewhat mixed in nature but were clearly trumped by what investors were more interested in with regards to forward growth. In its full-year 2025 results, Target reported revenue of $320.6 million. Net loss was $37.1 million for fiscal 2025 and adjusted EBITDA was $53.2 million. Meanwhile, Q4 revenue increased to $89.8 million from $83.7 million in the same period last year. While this was better than what Wall Street had expected, EPS missed expectations as the firm reported a net loss.

The more important thing to take away from the results was guidance and backlog. The company expects 2026 revenue to come in between $320 million and $330 million, with adjusted EBITDA between $60 million and $70 million. This is higher than what had been previously expected, which is part of why shareholders have been able to overlook the earnings miss. Not every quarter is as important as the trajectory of a company, and this might be one of those situations.

After all, the direction of the business is clearly changing. Since February 2025, the company has secured over $740 million in multi-year contract awards. The most recent announcements include a $129 million, 1,400-bed multi-year contract to support a multi-gigawatt power plant in West Texas — which is related to hyperscale AI data-center development — as well as a $23 million, 400-bed multi-year contract near Pecos, Texas.

In addition, the company expanded its data-center community contract and highlighted an active pipeline exceeding 20,000 beds, pointing to why Oppenheimer went bullish on TH stock. Target Hospitality is no longer just a legacy lodging story — it's becoming an enabler of the AI infrastructure buildout in areas where labor and housing are in short supply.

What Do Analysts Expect for Target Hospitality Stock?

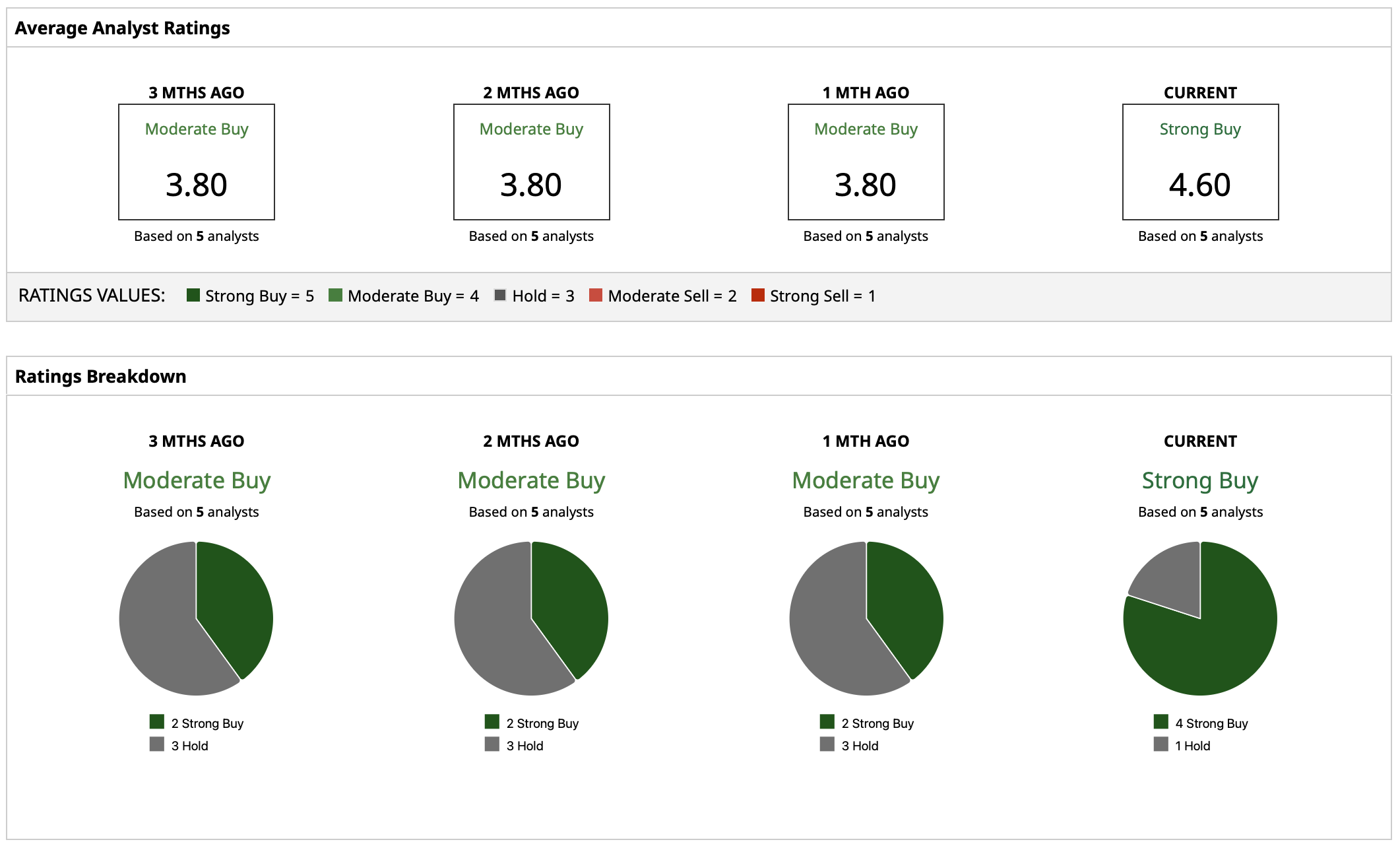

There is relatively little analyst coverage on TH stock, which is probably part of the reason to like shares with a “Strong Buy” consensus rating. The stock has analyst targets ranging from $11 to $12, with a mean estimate of $11.25 pointing to potential upside of approximately 18%. The high estimate of $12 suggest potential upside of about 27% from here.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)