/Meta%20Platforms%20Inc_%20by%20PJ%20McDonnell%20via%20Shutterstock.jpg)

Meta Platforms (META) suffered a setback late last week when it reported delays in the launch of its new foundational AI model, Avocado. According to reports, the company’s AI model underperforms leading competitors like Alphabet’s (GOOGL) Google, OpenAI, and Anthropic across multiple benchmarks, including writing, coding, and reasoning. Despite showing great improvements over its previous versions, Meta believes the model is not worthy of a launch right now.

Meta Platforms said that it will need at least until May to launch Avocado. This is disappointing for META stock shareholders, as Meta was projected to spend $135 billion on AI investments in 2026, almost twice what it spent in 2025. The company also has a history of big failures, with its metaverse project registering more than $70 billion in operating losses. Having said that, this is a price worth paying when a company has the ambition of leading today’s open source AI developments.

In the coming days, analysts will react to the impact of Meta's AI investments, and the company will need to compensate for the delays somewhere, bringing more clarity for shareholders.

About Meta Platforms Stock

Meta Platforms is the owner of popular social platforms like Facebook, Instagram, and WhatsApp. The company offers highly targeted advertising capabilities to businesses, based mainly on data collected from the billions of users that use its apps every day. Meta Platforms is headquartered in Menlo Park, California.

META stock had a volatile 2025, and it has only returned 3% over the last 12 months. The stock has suffered mainly due to the uncertainty surrounding its AI investments, despite the fact that it was one of the few companies that had a measurable return on investment (ROI) on its AI investments in the early part of the AI revolution. The Avocado debacle shows why investors may be hesitant to back Meta’s AI bets, even when the company is in a strong financial position to do so.

Wall Street has often criticized Meta for its huge investments in new ventures. When these ventures lose money, the company takes the blame. However, few point out that the reason it can afford to make these mistakes is its dominance in the social media arena. The firm owns WhatsApp, Facebook, Threads, and Instagram. Earlier in the year, it reported that more than 3.5 billion people use at least one of its platforms. With such a vast user base, the company can tap into multiple avenues to make up for money lost in any of its new ventures.

Despite that strength, META stock trades at a forward price-to-earnings (P/E) ratio of 20.6 times, which is below its five-year average. The company is expected to grow its earnings slightly in fiscal 2026, followed by an estimated 15% growth in fiscal 2027. META is by no means overvalued despite the Big Tech firm being one of the leading developers of AI technologies in the world. With a cash pile of $81.6 billion as of Dec. 31, 2025, the company has the financial strength to continue investing.

Meta to Accelerate AI-Driven Product Expansion

On the earnings call for fourth-quarter 2025 results, CEO Mark Zuckerberg called 2026 a year of “major AI acceleration.” The delay in the release of Avocado seems to have dented those plans, but investors can still look forward to some exciting developments.

For one, the company intends to merge its social media algorithms with large language models, helping develop “personal super intelligence,” an AI that understands personal context. Much the company’s investment will now also be diverted to its wearables projects. This is an exciting development because Meta could unlock great value if it can make its wearables ecosystem a profitable one with AI on the edge.

Reality Labs, the business segment that manages Meta's wearables and VR projects, is expected to continue operating at a loss this year as well. In Q1 2026, Meta is expected to bring in a revenue of $55 billion at the midpoint, with foreign currency tailwind expected to provide a 4% boost to its growth. As always, the company continues to fight multiple battles in multiple jurisdictions on the legal and regulatory front. The firm is also constrained when it comes to compute capacity, so efficiency through partnerships is an important way to proceed from here for Meta.

What Are Analysts Saying About Meta Stock?

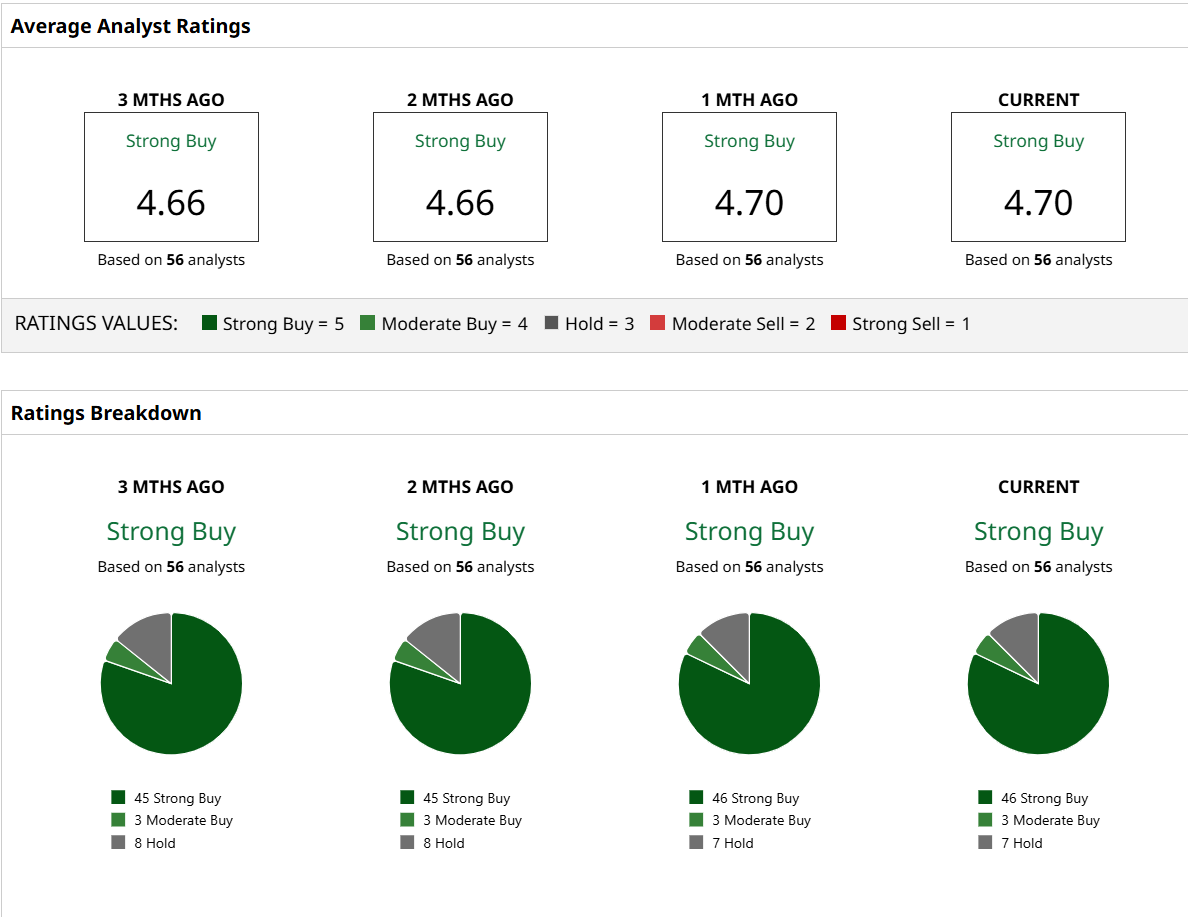

Jefferies analyst Brent Thill recently retained a price target of $1,000 for META stock. Out of 56 analysts with coverage, 46 analysts have a “Strong Buy” rating on the stock, reflecting the bullish sentiment on Wall Street. META stock has a mean target price of $864.04, offering 39% potential upside from current levels.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)