/AI%20(artificial%20intelligence)/AI%20by%20TierneyMJ%20via%20Shutterstock.jpg)

Sydney-based software company Atlassian Corporation (TEAM) has announced it will cut 10% of its workforce, or about 1,600 jobs, as it grapples with fears about artificial intelligence (AI). The company has been facing the same concern plaguing software firms: the fear that AI will become a significant competitor to software.

Beaten-down Atlassian is trying to restructure itself to be more AI-focused, with CEO Mike Cannon-Brookes saying that the cost-saving measures are there to “self-fund further investment in AI and enterprise sales.” The company is trying to increase demand for its Rovo AI features. Moreover, it aims to achieve sustained profitability, which has eluded it.

Therefore, should you consider investing in Atlassian now?

About Atlassian Stock

Headquartered in Sydney, Australia, Atlassian develops collaboration and productivity software for teams worldwide. Its core operations center on tools such as Jira for project management, Confluence for documentation, and Trello for task management, enabling efficient workflows across software development and business operations. The company has a market capitalization of $20.09 billion.

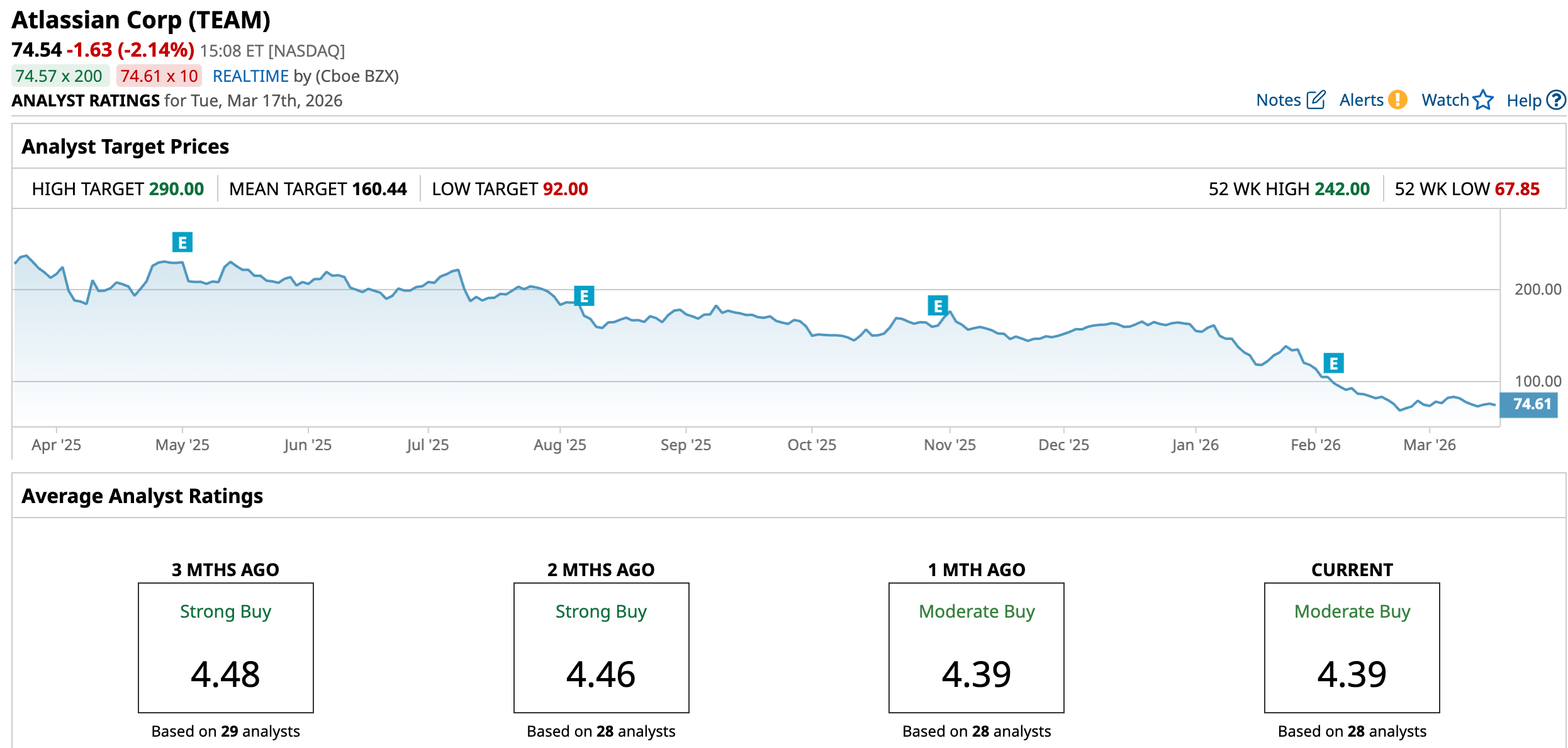

Atlassian’s stock has come under pressure due to several factors, including fears of AI disruption to software tools and concerns about its persistent unprofitability. Over the past 52 weeks, the stock has declined 66.24%, while it has been down 53.98% year-to-date (YTD).

Last month, the stock experienced a massive selloff amid AI fears, as investors were concerned about the company’s vulnerability given its focus on small- and medium-sized businesses and its lack of GAAP-based profitability. It had reached a 52-week low of $67.85 on Feb. 24, but is up 10% from that level.

The selloff has brought down Atlassian’s valuation. On a forward-adjusted basis, the stock’s price-to-earnings ratio of 16.00x is lower than the industry average of 21.59x.

Atlassian Q2 FY2026 Beats Expectations

On Feb. 5, Atlassian reported its second-quarter results for fiscal 2026 (quarter ended Dec. 31, 2025), which beat analysts’ expectations. The company’s total revenue increased 23.3% year-over-year (YOY) to $1.59 billion, beating the $1.54 billion Wall Street analysts had expected. The majority of this revenue came from subscriptions, which grew 24.3% annually to $1.51 billion.

Atlassian’s GAAP operating loss narrowed from $57.48 million in Q2 FY2025 to $47.75 million in Q2 FY2026. The company’s non-GAAP operating income increased from $335.15 million to $430.23 million. Its non-GAAP EPS increased from $0.96 to $1.22, topping the $1.12 analysts expected.

Wall Street analysts have a cautiously positive view about Atlassian’s bottom line trajectory. For the third quarter of fiscal 2026, its EPS is expected to increase by 124% YOY to $0.06. Moreover, for fiscal 2026, the company’s loss per share is projected to decrease by 98.8% annually to $0.01, followed by a significant YOY worsening of 500% to $0.06 loss per share for fiscal 2027.

What Analysts Think About Atlassian’s Stock

This month, analysts from Mizuho maintained an “Outperform” rating on Atlassian’s shares, while lowering the price target from $205 to $185, as the company announced a major restructuring to eliminate a significant portion of its workforce. However, the analysts also expect these cost savings to drive higher margins and GAAP-based profitability.

In February, analysts at Citi lowered their price target for Atlassian from $210 to $160, while maintaining a “Buy” rating. While Citi analysts believe that the company’s fundamentals are “sound,” they cited “sector turmoil” as the reason for the price target cut. In the same month, Macquarie analyst Steve Koenig maintained an "Outperform" rating while lowering the price target from $240 to $150.

Oppenheimer lowered the firm’s price target from $275 to $150, while maintaining an “Outperform” rating on the stock. The firm’s analysts cited AI headwinds for the price target reduction. Ryan MacWilliams at Wells Fargo reduced the firm’s price target on Atlassian from $216 to $155 and maintained its “Overweight” rating, noting that the broader SaaS sector remains challenging.

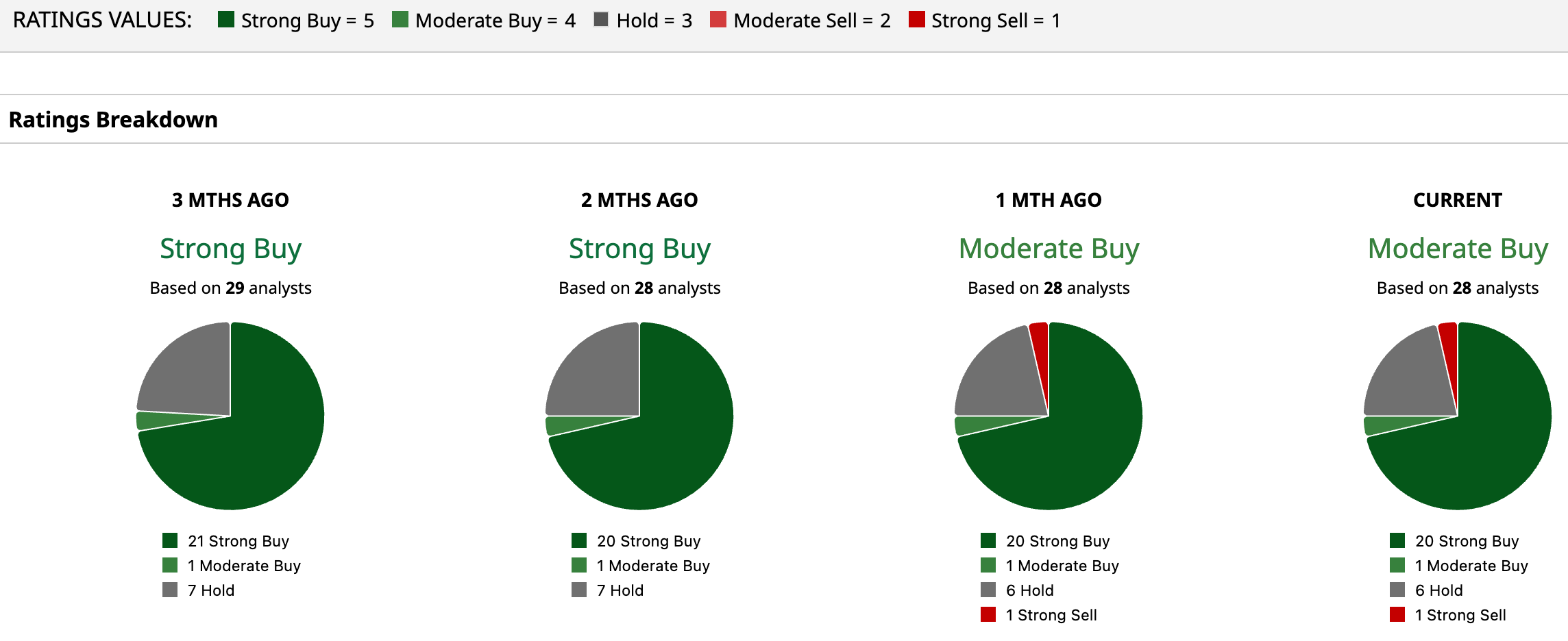

Atlassian remains a reasonably popular name on Wall Street despite the selloff, with analysts awarding it a consensus “Moderate Buy” rating. Of the 28 analysts rating the stock, 20 have given it a “Strong Buy” rating, one a “Moderate Buy,” six a middle-of-the-road “Hold,” and one a “Strong Sell.” The consensus price target of $160.44 represents a 115% upside from current levels. Moreover, the Street-high price target of $290 indicates a 289% upside.

Key Takeaways

AI might not prove to be the significant threat to software that the market is anticipating. While the market’s possible overreaction gradually passes, Atlassian has been bolstering itself with AI. And while the restructuring would result in short-term costs, the move might be beneficial in the long term. As Wall Street analysts keep their faith in the company’s prospects, it might be worth a look.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)