/Ulta%20Beauty%20Inc%20shop%20location%20by-%20M_%20Suhail%20via%20iStock.jpg)

Shares of Ulta Beauty (ULTA) have recently come under pressure after the beauty retailer delivered quarterly results that fell slightly short of Wall Street’s expectations and issued a cautious outlook for the year ahead. The company reported fourth-quarter EPS of about $8.01 on revenue of around $3.9 billion, but the earnings figure missed analyst estimates, while management’s fiscal 2026 guidance also came in below expectations.

The softer guidance, combined with concerns about rising operating costs, intensifying competition, and a more cautious consumer environment, triggered a sharp selloff in the stock and erased its earlier gains. However, despite the near-term disappointment, many analysts remain constructive on Ulta’s long-term prospects given its solid brand portfolio, loyal customer base, and leadership in the growing beauty category.

Let’s analyze whether this dip created an attractive entry point, or if it is a warning sign of slowing growth ahead.

About Ulta Beauty Stock

Ulta Beauty is a leading specialty beauty retailer that sells cosmetics, skincare, fragrance, haircare products, and beauty tools through its nationwide store network, e-commerce platform, and in-store salon services. The company operates hundreds of retail locations and carries both prestige and mass-market beauty brands alongside its own private-label offerings. Ulta Beauty is headquartered in Bolingbrook, Illinois, and has grown into one of the largest beauty retail chains. The company has a market cap of roughly $23.8 billion.

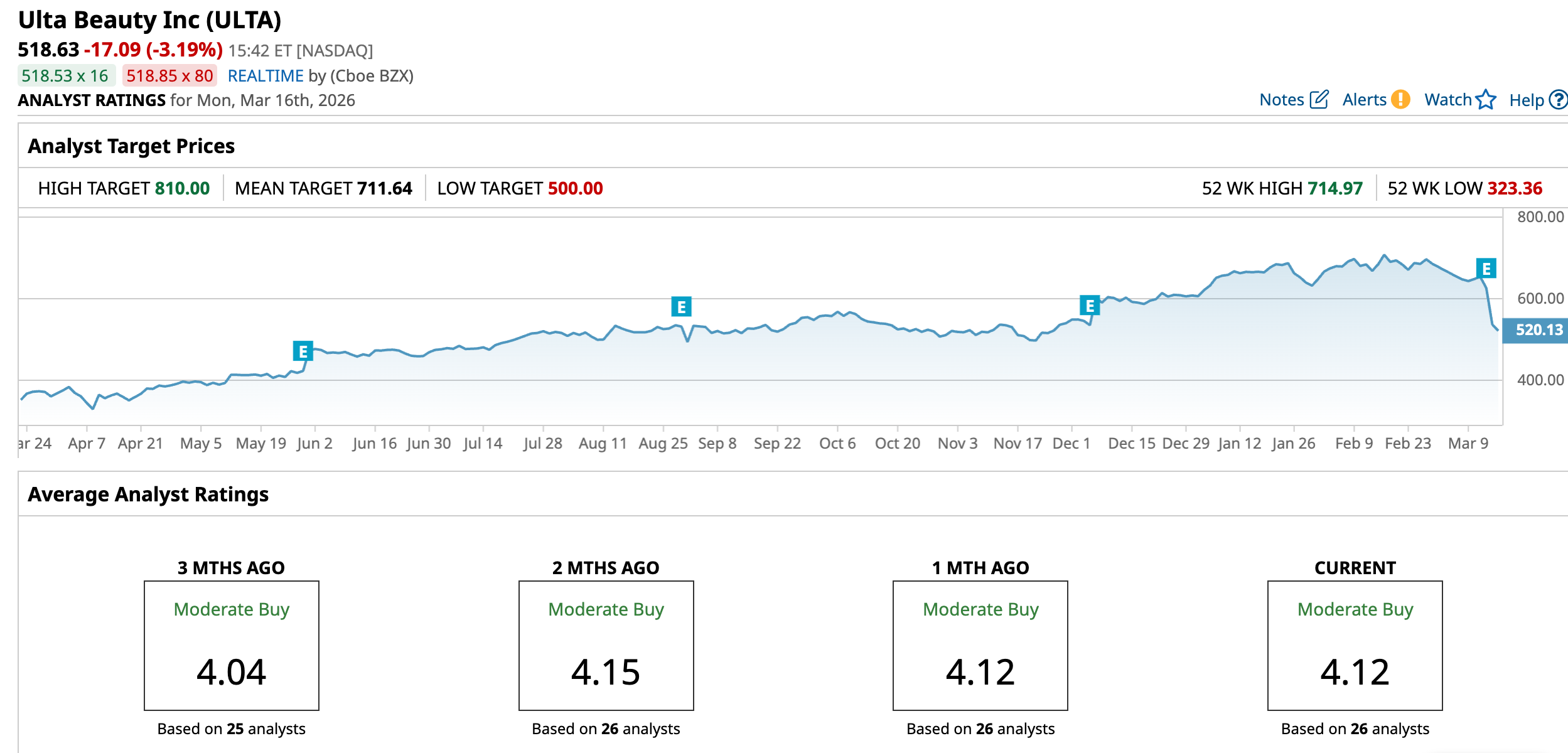

Shares of Ulta Beauty have experienced notable volatility in 2026 after a strong run over the past year. Over the past 52 weeks, the stock has delivered an impressive gain of 47%, reflecting strong demand in the beauty category and Ulta’s solid operating performance. However, the stock has pulled back in 2026, declining about 13.14% year-to-date (YTD) as investors reassess the company’s near-term growth outlook.

The most significant decline occurred following the company’s latest earnings release, which triggered a sharp selloff. Ulta shares plunged 14.24% in extended trading on March 12 after the results, as investors reacted to earnings miss and management’s more cautious outlook for fiscal 2026, including softer comparable sales expectations and margin pressure. The post-earnings drop erased much of the stock’s earlier gains this year and pushed it well below its recent highs of $714.97, reached on Feb. 18. The stock closed the last session at $521.95.

The stock is currently trading at 18.82 times forward earnings, which is a premium to industry peers.

Mixed Financial Performance

Ulta Beauty released its fourth-quarter and fiscal 2025 results on March 12, 2026, reporting strong sales growth but some margin pressure due to higher operating costs and investments. For the fourth quarter of fiscal 2025, the company generated net sales of $3.9 billion, representing an 11.8% year-over-year (YOY) increase from $3.5 billion in the prior-year quarter, while comparable sales rose 5.8%, driven by a 4.2% increase in average ticket and a 1.6% rise in transactions.

However, profitability declined as expenses climbed, with earnings per share (EPS) of $8.01, down from $8.46 a year earlier, and slightly below estimates. Its operating margin contracted to 12.2% from 14.8% due largely to higher advertising spending, corporate investments, and incentive compensation.

For the full fiscal year 2025, Ulta Beauty delivered net sales of $12.4 billion, an increase of 9.7% YOY, while comparable sales grew 5.4%, supported by both higher ticket sizes and transaction growth. Full-year EPS reached $25.64, slightly up from $25.34 in fiscal 2024, although profitability was pressured by rising operating costs, with operating margin declining to 12.4% from 13.9% in the prior year.

Furthermore, Ulta Beauty provided fiscal 2026 guidance calling for net sales growth of 6% to 7%, comparable sales growth of 2.5% to 3.5%, and operating income growth of 6% to 9%. The company expects EPS in the range of $28.05 to $28.55, while planning capital expenditures of about $400 million to $450 million to support new store openings, digital initiatives, and operational improvements.

In addition, the consensus EPS estimate of $28.43 for fiscal 2027 indicates an increase of 10.49% YOY, before surging by another 11.8% annually to $31.66 in fiscal 2028.

What Do Analysts Expect for Ulta Beauty Stock?

Despite the sour market reaction to the earnings release, Ulta Beauty received a “Buy” rating reiteration from UBS with an $810 price target following its fourth-quarter results.

Plus, Ulta Beauty received a “Buy” rating reaffirmation from D.A. Davidson, which also maintained its $650 price target.

On the other hand, Piper Sandler lowered its price target on Ulta Beauty to $725 from $775 but maintained an “Overweight” rating, citing spending concerns.

Ulta Beauty stock has a consensus “Moderate Buy” rating overall. Out of 26 analysts covering the stock, 15 recommend a “Strong Buy,” one gives a “Moderate Buy,” nine analysts stay cautious with a “Hold” rating, and one has a “Strong Sell” rating.

While the average analyst price target of $711.64 suggests an upside of 37.2%, UBS’ Street-high target price of $810 suggests as much as 56.2% upside ahead.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)