/Meta%20Platforms%20by%20Primakov%20via%20Shutterstock.jpg)

Meta Platforms (META) stock has been relatively subdued this year, seeing 3% upside in the last 52 weeks. While fundamentals remain strong, markets concerns related to massive capital spending have persisted.

Amid the sideways price action, Meta has continued to focus on investments that are likely to accelerate growth. This includes bolstering its superintelligence efforts and driving growth from the hardware business.

From the perspective of inorganic growth, Meta recently announced the acquisition of Moltbook, an AI agent social networking platform. Further, the Moltbook team is expected to join Meta’s Superintelligence Labs.

Meta Platforms has already been working on strengthening its Superintelligence Lab to accelerate new AI model development. Overall, this acquisition is likely to support the company's efforts to compete against AI rivals like OpenAI, among others.

About Meta Platforms Stock

Headquartered in Menlo Park, California, and originally founded as Facebook, Meta Platforms rebranded in 2021 to emphasize its focus on building beyond 2D screens. The company develops products that enable people to connect and share, sporting a suite of social apps such as Facebook, Messenger, Instagram, and WhatsApp.

Currently, Meta is focused on building “personal superintelligence” for users. The objective is to integrate AI into existing apps and also leverage AI for advanced wearable products. For example, Meta is already dominating the smart glasses market that’s driven by AI-enabled models.

For fiscal 2025, Meta Platforms reported revenue growth of 22% year-over-year (YOY) to $201 billion. For the same period, operating cash flow was robust at $115.8 billion, providing high financial flexibility for investments in innovation.

However, even with the robust growth, META stock has corrected by almost 16% in the last six months. This seems like a good opportunity for investors to accumulate shares as Meta focuses on “advancing personal superintelligence” in 2026.

Ample Growth Opportunities

As of Q4 2025, Meta reported Family Daily Active People (DAP) of 3.58 billion. This presents a big user base for monetization. Average revenue per person in Q4 was robust at $16.56. With Meta focusing on building personal superintelligence, it’s likely that revenue per user will continue to swell, which will help ensure top-line growth and cash flow upside.

Another important point to note is that, while Family of Apps revenue has been a growth and cash flow driver, Meta's Reality Labs has witnessed sustained operating losses. However, for Reality Labs, CEO Mark Zuckerberg noted that the company is directing most of its investment "towards glasses and wearables going forward.” Last year, the sales of glasses more than tripled. As growth accelerates for wearables, it’s likely that the segment will be a value creator in the next few years.

In terms of geographical presence, Meta reported about 68% of its revenue from the U.S., Canada and Europe in Q4 2025. Accordingly, there seems to be scope for growth from emerging markets, which have a significant number of active users.

For 2026, Meta has guided for capital expenditures in the range of $115 billion to $135 billion. However, the market concerns over big investments by hyperscalers seem to be discounted in the stock. As growth sustains through innovation, the outlook for META stock is likely to be optimistic.

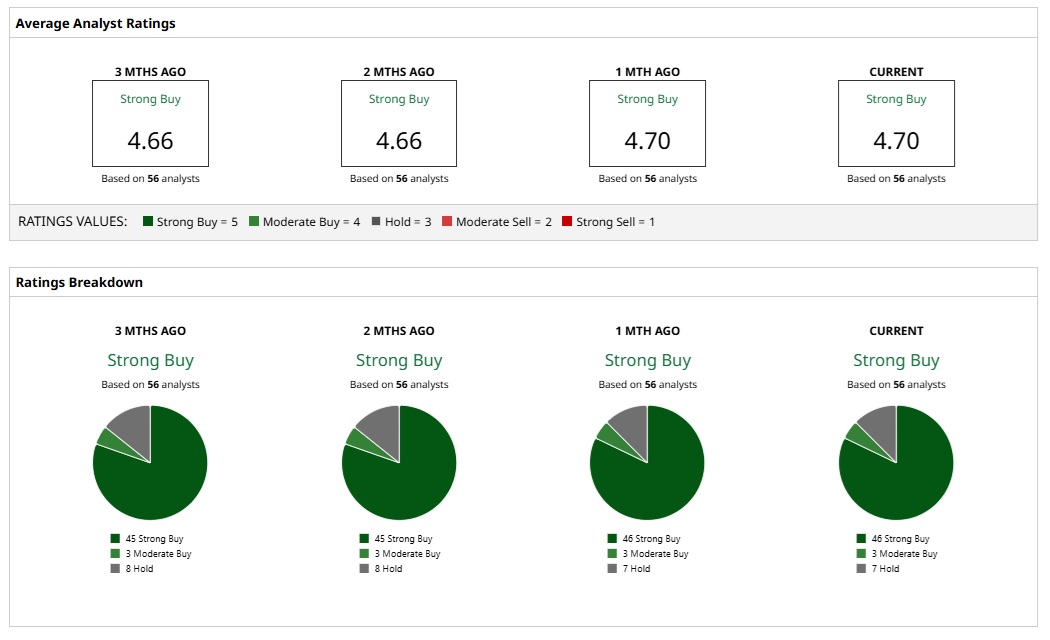

What Do Analysts Say About META Stock?

Based on 56 analysts with coverage, META stock is a consensus “Strong Buy.” While 46 analysts assign a “Strong Buy” rating, three analysts have a “Moderate Buy" rating, and seven analysts call META a “Hold.”

Analysts have a mean price target of $864.04, implying about 35% potential upside from here. Further, the most bullish price target of $1,144 suggests that META stock could rise as much as 79% from current levels.

A forward price-to-earnings (P/E) ratio of 22 times and a P/E-to-growth ratio of 1.01 indicate that META stock is attractively valued. With Meta Platforms bolstering its superintelligence efforts and pursuing inorganic growth opportunities, the outlook appears positive for the coming years.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)