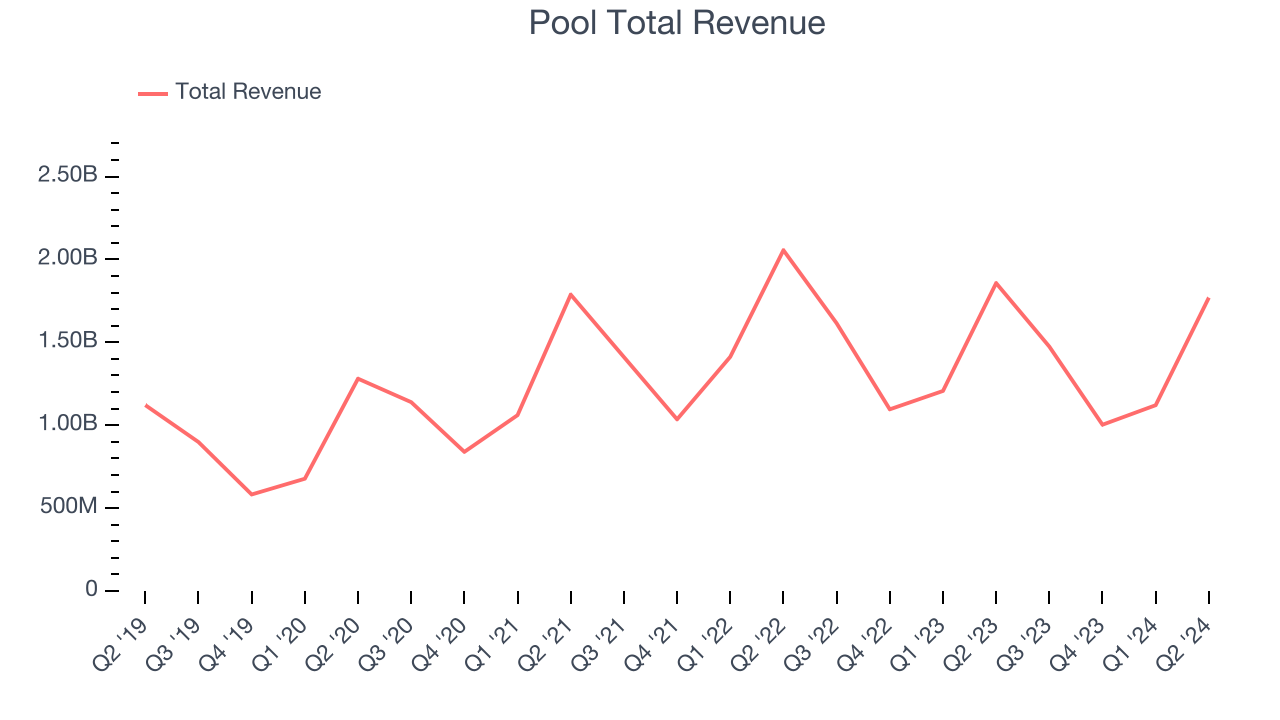

Swimming pool distributor Pool (NASDAQ:POOL) reported Q2 CY2024 results topping analysts' expectations, with revenue down 4.7% year on year to $1.77 billion. It made a GAAP profit of $4.99 per share, down from its profit of $5.91 per share in the same quarter last year.

Is now the time to buy Pool? Find out by accessing our full research report, it's free.

Pool (POOL) Q2 CY2024 Highlights:

- Revenue: $1.77 billion vs analyst estimates of $1.74 billion (1.5% beat)

- EPS: $4.99 vs analyst estimates of $4.90 (1.7% beat)

- Gross Margin (GAAP): 30%, down from 30.6% in the same quarter last year

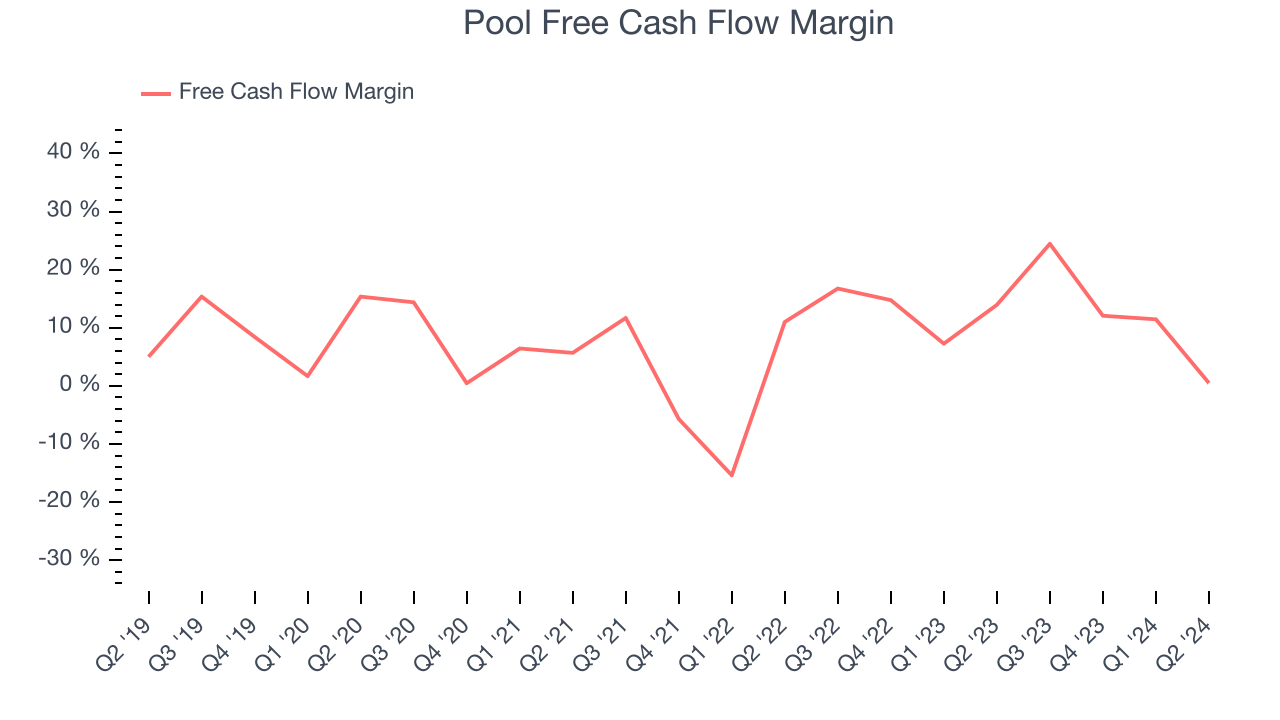

- Free Cash Flow of $8.77 million, down 93.2% from the previous quarter

- Market Capitalization: $12.54 billion

“The demand for maintenance products supported a solid quarter given the trend for lower consumer spending on high dollar discretionary items. Our second quarter net sales of $1.8 billion, down 5% from the second quarter of 2023, showed an improving trend from the decrease of 7% that we saw in the first quarter of 2024. Slightly better than expected sales in the last week of June improved our sales for the first half of the year to a 6% decline compared to the around 6.5% highlighted in our June 24th release. Gross margin of 30.0% reflects the structural improvements we are making in our business to expand margin, particularly considering the lower contribution from building materials product sales during the second quarter of 2024. Looking ahead, our team is focused on providing an exceptional customer experience and, with our strong balance sheet, we remain committed to our strategic growth investments, capacity creation efforts and innovation,” commented Peter D. Arvan, President and CEO.

Founded in 1993 and headquartered in Louisiana, Pool (NASDAQ:POOL) is one of the largest wholesale distributors of swimming pool supplies, equipment, and related leisure products.

Specialized Consumer Services

Some consumer discretionary companies don’t fall neatly into a category because their products or services are unique. Although their offerings may be niche, these companies have often found more efficient or technology-enabled ways of doing or selling something that has existed for a while. Technology can be a double-edged sword, though, as it may lower the barriers to entry for new competitors and allow them to do serve customers better.

Sales Growth

A company's long-term performance is an indicator of its overall business quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years. Over the last five years, Pool grew its sales at a weak 11.8% compounded annual growth rate. This shows it failed to expand in any major way and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Pool's history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 4.7% annually.

This quarter, Pool's revenue fell 4.7% year on year to $1.77 billion but beat Wall Street's estimates by 1.5%. Looking ahead, Wall Street expects revenue to decline 1.3% over the next 12 months.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

Pool has shown decent cash profitability, giving it some flexibility to reinvest. The company's free cash flow margin averaged 12.5% over the last two years, slightly better than the broader consumer discretionary sector.

Pool broke even from a free cash flow perspective in Q2. The company's margin regressed as it was 13.4 percentage points lower than in the same quarter last year, but we wouldn't read too much into it because working capital and capital expenditure needs can be seasonal, leading to quarter-to-quarter swings. Long-term trends trump short-term fluctuations.

Over the next year, analysts predict Pool's cash profitability will fall. Their consensus estimates imply its free cash flow margin of 11.5% for the last 12 months will decrease to 9.5%.

Key Takeaways from Pool's Q2 Results

It was encouraging to see Pool narrowly top analysts' revenue and EPS expectations this quarter. Zooming out, we think this was a decent quarter, showing the company is staying on target. The stock traded up 2.6% to $334.69 immediately after reporting.

So should you invest in Pool right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)

/Intel%20Corp_%20Santa%20Clara%20campus-by%20jejim%20via%20Shutterstock.jpg)