Over the past 12 months, we have published several articles arguing that past-due student loans are very likely to affect the entire retail credit industry. As a reminder, federal student loan payments were paused for 43 months starting in March 2020, pushing delinquencies below 1%. After repayments resumed in September 2023, a one-year "on-ramp" period prevented missed payments from affecting credit reports. That protection expired in October 2024. Since then, more than 17% of student loan borrowers have fallen at least 90 days past due on their payments at least once. As it takes 270 days of missed payments to enter federal student loan default, 4Q25 was the first quarter when new defaults began appearing on credit reports.

According to the Fed’s estimates, roughly 1 million federal student loan borrowers defaulted during 4Q25, with an additional 2.6 million borrowers defaulting during 1Q26. The Fed also notes that borrowers in the now-defunct SAVE repayment plan entered repayment but were placed into forbearance during the on-ramp due to litigation. Very few have re-entered repayment since missed payments were reported to credit bureaus. This delay means that a second wave of defaults might emerge as these 7 million borrowers reach the nine-month mark in the repayment period.

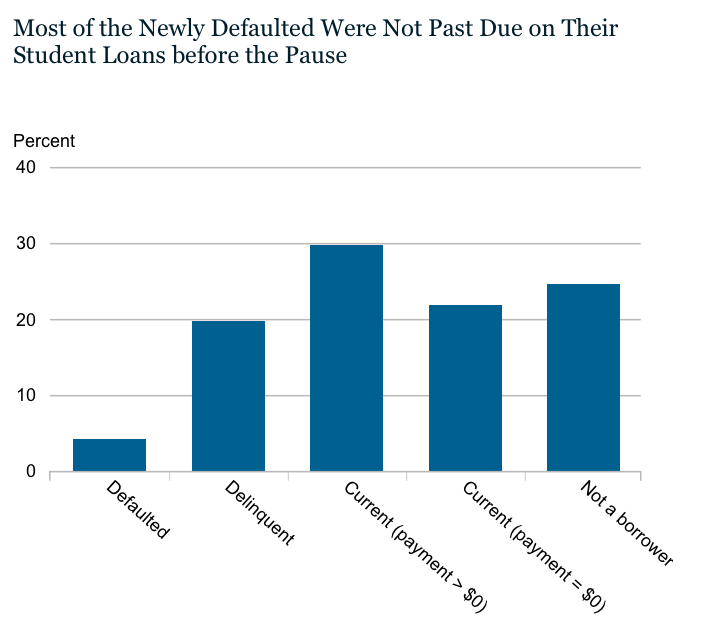

The NY Fed has recently published a study on the situation with student loans, which revealed quite a few interesting observations. First, the study challenges the popular narrative, often repeated by the media and investment banks, that current credit quality is merely normalizing to pre-pandemic levels. As the chart below shows, most recent defaulters were not past due before the pause. Only about 4% were already in default before the pause, and the borrowers who defaulted over the past two quarters were not concentrated among those who were struggling with payments before the pandemic: more than three-quarters were current or did not have a student loan payment due in 2019.

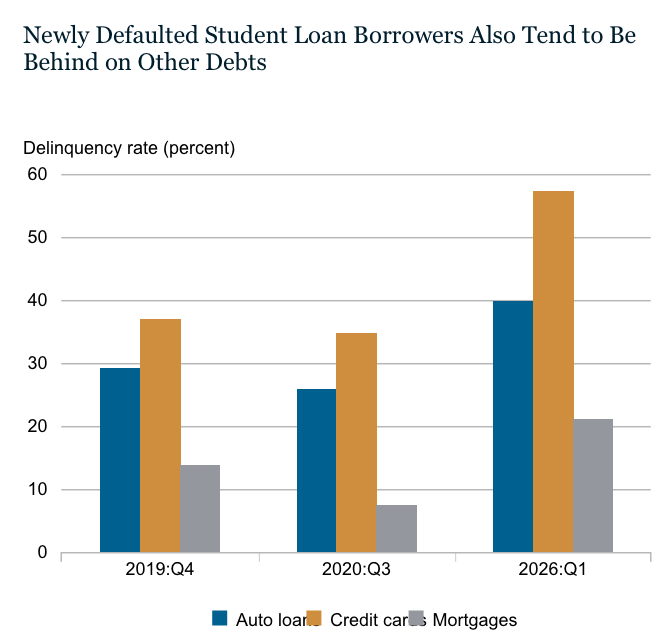

Unsurprisingly, defaulted student loan borrowers are also having issues with their other credit products. They now have very high delinquency rates across all credit products: nearly 40% of those with auto loans are past due, 56% of those with at least one credit card are past due, and 20% of those with a mortgage are past due.

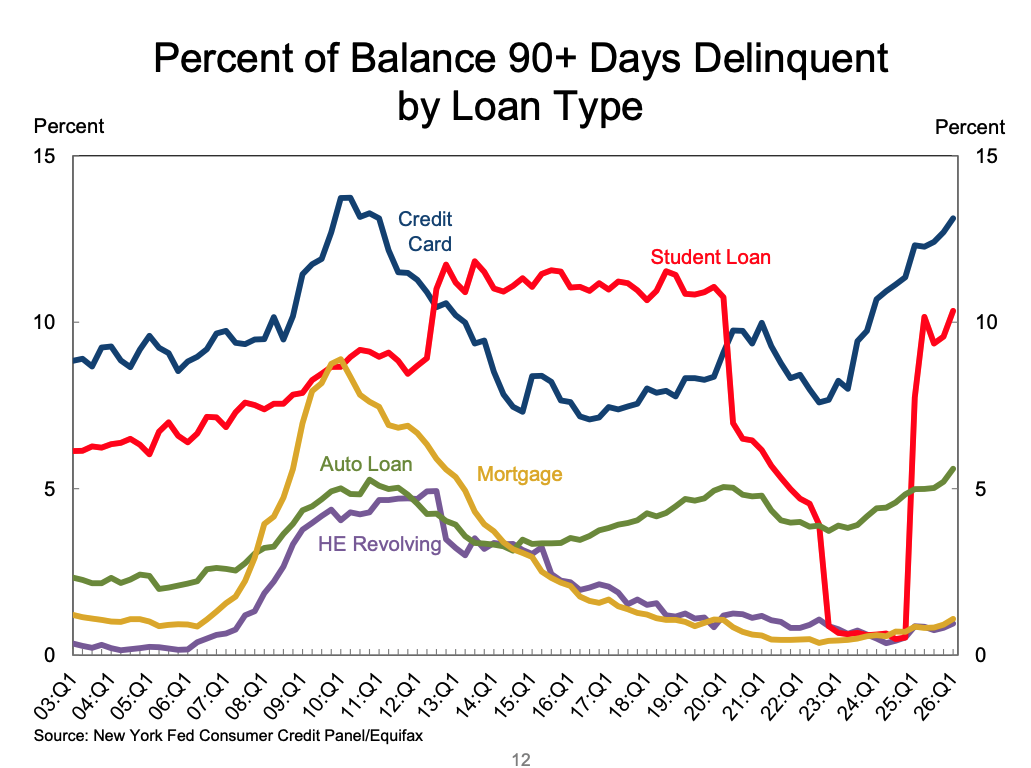

The Fed says that delinquent and newly defaulted borrowers make up only 2% of the credit population, and balances held by defaulted or delinquent student loan borrowers represent 2.7% of auto loans, 2% of credit cards, and 1% of mortgages. However, a second wave of defaults could still emerge as SAVE-plan borrowers re-enter repayment, although its size remains uncertain. Importantly, these newly defaulted student loan borrowers are adding to already very weak credit-quality trends. As the chart below shows, the share of credit cards that are 90+ days delinquent is just a tad below the GFC peak, while the respective share of auto loans is higher.

This weakness in retail lending may help explain the record-low readings of consumer sentiment.

Bottom line

Believe it or not, there are more major issues on the larger bank balance sheets as compared to smaller banks, which we have covered in past articles. Moreover, consider that there was one major issue which caused the GFC back in 2008, whereas today, we currently have many more large issues on bank balance sheets. These risk factors include major issues in commercial real estate, rising risks in consumer debt (approaching 2007 levels), underwater long-term securities, over-the-counter derivatives, high-risk shadow banking (the lending for which has exploded), and elevated default risk in commercial and industrial (C&I) lending. So, in our opinion, the current banking environment presents even greater risks than what we have seen during the 2008 GFC.

Almost all the banks that we have recommended to our clients are community banks, which do not have any of the issues we have been outlining over the last several years. Of course, we're not saying that all community banks are good. There are a lot of small community banks that are much weaker than larger banks. That’s why it's absolutely imperative to engage in a thorough due diligence to find a safer bank for your hard-earned money. And what we have found is that there are still some very solid and safe community banks with conservative business models.

So, I want to take this opportunity to remind you that we have reviewed many larger banks in our public articles. But I must warn you: The substance of that analysis is not looking too good for the future of the larger banks in the United States, and you can read about them in the prior articles we have written.

Moreover, if you believe that the banking issues have been addressed, I think that New York Community Bank is reminding us that we have likely only seen the tip of the iceberg. We were also able to identify the exact reasons in a public article which caused SVB to fail. And I can assure you that they have not been resolved. It's now only a matter of time before the rest of the market begins to take notice. By then, it will likely be too late for many bank deposit holders.

At the end of the day, we're speaking of protecting your hard-earned money. Therefore, it behooves you to engage in due diligence regarding the banks which currently house your money.

You have a responsibility to yourself and your family to make sure your money resides in only the safest of institutions. And if you're relying on the FDIC, I suggest you read our prior articles, which outline why such reliance will not be as prudent as you may believe in the coming years, with one of the main reasons being the banking industry’s desired move towards bail-ins. (And, if you do not know what a bail-in is, I suggest you read our prior articles.)

It's time for you to do a deep dive on the banks that house your hard-earned money in order to determine whether your bank is truly solid or not. You can feel free to review our due diligence methodology here.

Avi Gilburt is founder of ElliottWaveTrader.net and SaferBankingResearch.com.

/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

/Palantir%20(PLTR)%20by%20Piotr%20Swat%20via%20Shutterstock.jpg)

/NVIDIA%20Corp%20logo%20on%20phone%20and%20AI%20chip-by%20Below%20the%20Sky%20via%20Shutterstock.jpg)