Shares of Zscaler (ZS) spent much of this year stuck in the same storm battering the broader software sector. Investors feared rapid advances in artificial intelligence (AI) could encourage companies to build more tools in-house instead of paying for services from firms such as Zscaler.

The anxiety already kept pressure on the stock before the latest selloff opened the floodgates. On Wednesday, May 27, Zscaler’s shares nosedived more than 31.5% for one of the worst single day declines in the company’s history after guidance failed to impress Wall Street.

Revenue and profit both topped analyst expectations, yet investors clearly wanted more fuel in the tank for the road ahead. Management also revealed that Zscaler lost two sales leaders during the quarter. CFO Kevin Rubin said the company adopted a “prudent approach” toward guidance during the transition period, which only added more smoke to an already nervous market.

At the same time, Zscaler warned that memory shortages, rising prices, and climbing infrastructure costs would increase capital expenditures as a percentage of revenue by 200 basis points during FY2027.

Investor sentiment toward software stocks has already turned shaky as AI threatens to shake up traditional business models across the sector. Now, a brutal one-day plunge paired with cautious guidance places ZS stock firmly under the microscope as investors search for signs of stability instead of another shoe waiting to drop.

About Zscaler Stock

Headquartered in San Jose, California, Zscaler is a cloud-native security firm built entirely on Zero Trust architecture from the ground up, which means no user, no device, and no application gets trusted by default, regardless of where they are coming from or who they claim to be.

The roughly $20.325 billion market cap company protects users and internet traffic, secures private application access without relying on traditional virtual private networks (VPNs), prevents data leaks across cloud and software-as-a-service (SaaS) environments, and delivers security tools specifically designed for AI applications.

Also, it offers vulnerability management, threat detection, asset exposure monitoring, and managed response services through one unified cloud platform. Even so, shareholders have watched the stock sink like a stone in the current environment.

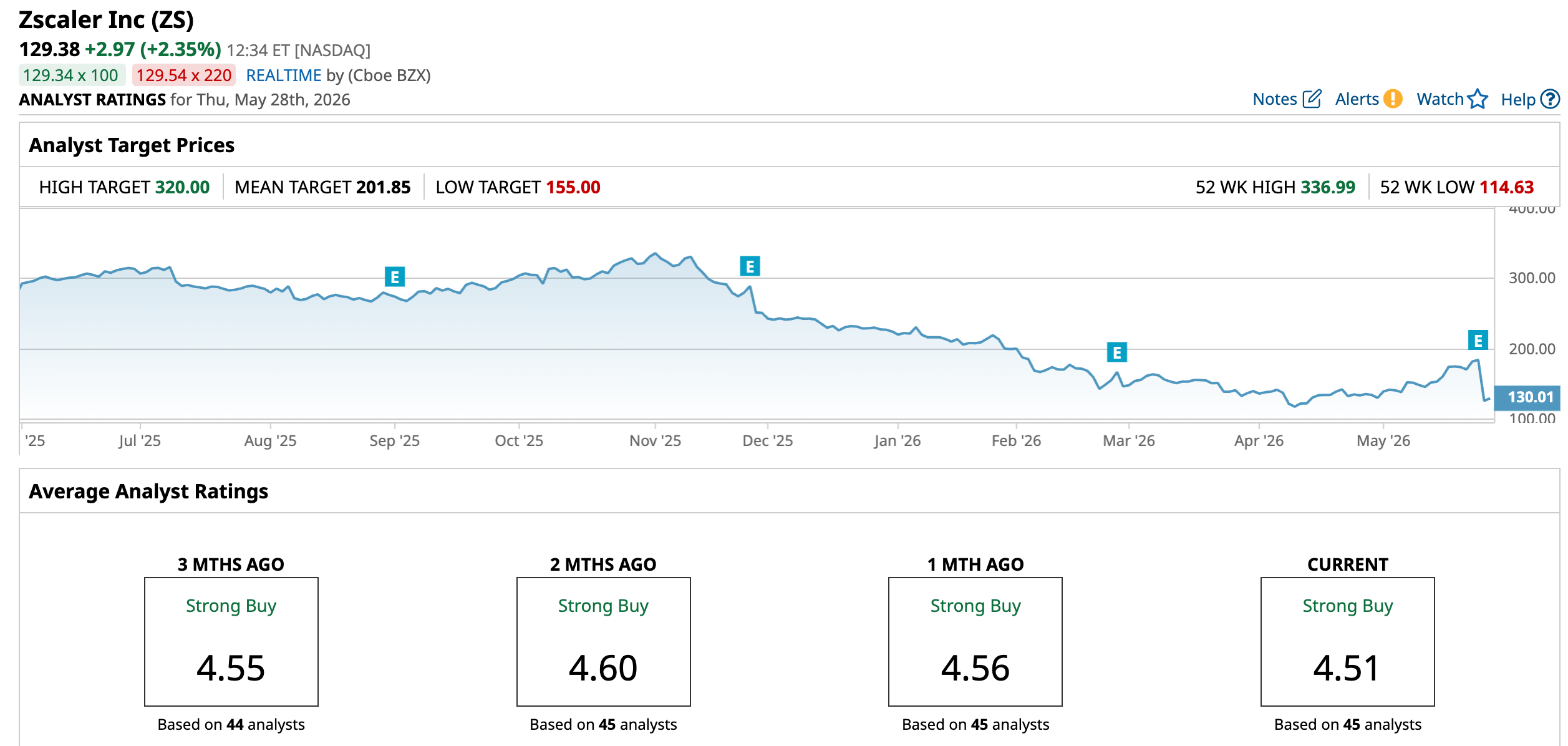

Over the last 52 weeks, ZS stock shed 49.76% of its value. In 2026 alone, the stock is down 43.34%. And in just the past five trading sessions, it lost another 26.95%, almost all of it driven by the market's reaction to the company's most recent financial guidance and the business prospects attached to it.

On the valuation side, ZS stock currently trades at 6.14 times sales. The figure still sits above the industry average, although the multiple now looks cheaper compared to the company’s own five-year average valuation.

Zscaler Surpasses Q3 Earnings

On May 26, Zscaler reported its Q3 FY2026 results, and on paper, the numbers were genuinely good. Revenue climbed 25.4% year-over-year (YOY) to $850.5 million, clearing analyst expectations of $835.6 million. Adjusted EPS grew 28.6% from the year-ago value to $1.08, beating Wall Street's estimate of $1.01.

Management pointed to strong adoption of its Zero Trust Secure Access Service Edge platform, expanding traction in the public sector, and solid performance across the Americas as the engines behind the quarter's momentum.

However, Zscaler has started feeling the pinch from rising infrastructure expenses as AI demand is tightening the screws across the broader technology supply chain. The company stepped on the gas with data center equipment purchases to lock in prices before costs could climb higher.

This step now carries a bigger price tag. Management expects current quarter capital expenditures to reach a high-single digit percentage of revenue after earlier guidance pointed toward a mid-single digit percentage.

The company also nudged its FY2026 outlook higher. Zscaler now expects revenue between $3.32 billion and $3.33 billion alongside adjusted EPS of $4.10 to $4.11. Previous guidance called for revenue between $3.31 billion and $3.32 billion with earnings ranging from $3.99 to $4.02 a share.

Even with those upgrades on the table, investors zeroed in on softer-than-expected fiscal fourth quarter revenue guidance. Zscaler forecast Q4 revenue between $875 million and $878 million, landing slightly below analyst expectations of $878.6 million. Q4 earnings guidance of $1.08 to $1.09 a share still topped Wall Street estimates, though traders clearly did not bite.

On the other hand, analysts expect Q4 FY2026 loss per share to narrow 75% YOY to $0.01. Full fiscal 2026 loss per share could shrink 81.3% from the previous year to $0.03. FY2027 could finally flip the script with EPS reaching $0.08, marking a sharp 366.7% jump from the prior year.

What Do Analysts Expect for Zscaler Stock?

Several Wall Street analysts wasted little time trimming their price targets after the earnings report and cautious guidance rattled confidence. Meta Marshall from Morgan Stanley lowered her target for ZS stock to $145 from $155 while maintaining a “Hold” rating.

Several other firms also sharpened the knives. Roger Boyd at UBS lowered his target to $225 from $260 after pointing toward the company’s cautious outlook. However, one analyst stands in Zscaler’s corner. Jonathan Ruykhaver from Cantor Fitzgerald remains the most bullish analyst covering ZS stock. He currently carries a “Buy” rating alongside a $300 price target.

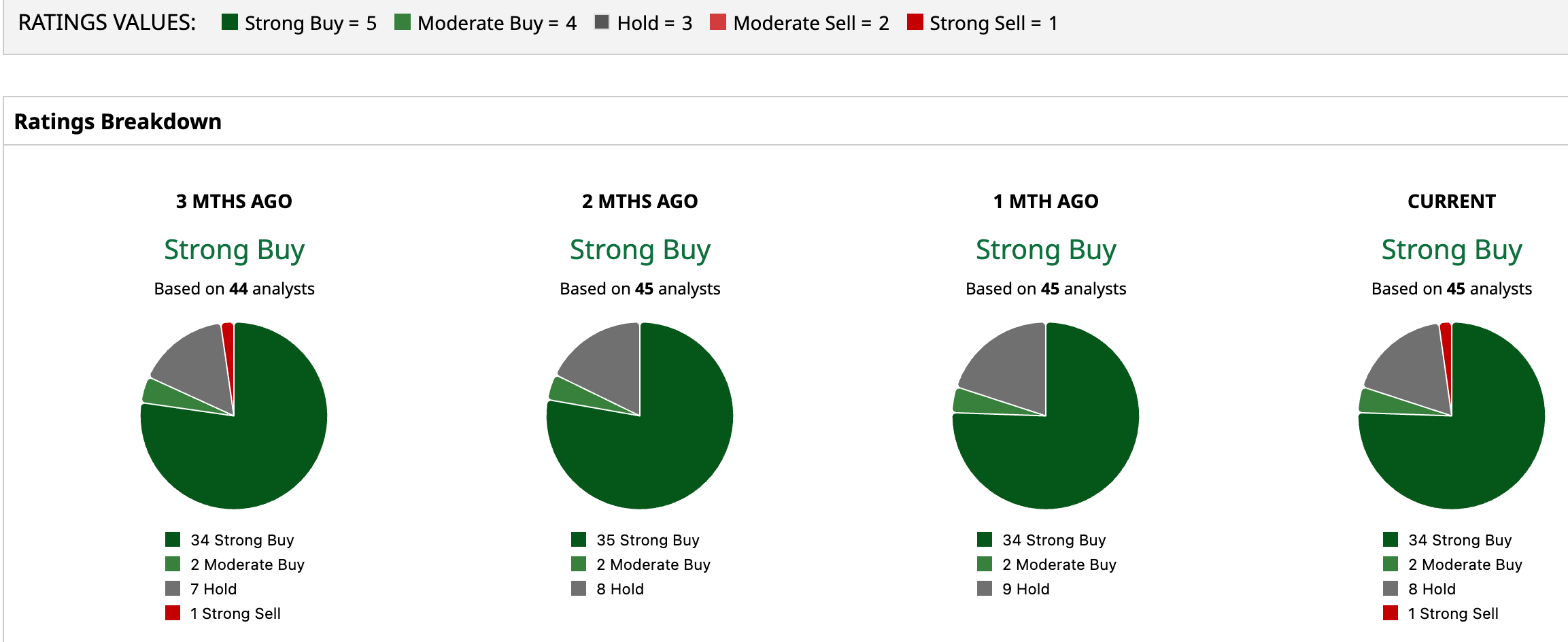

Currently, ZS stock carries an overall rating of “Strong Buy.” Among 45 analysts covering the shares, 34 maintain “Strong Buy” ratings, two recommend “Moderate Buy,” eight stick with “Hold” ratings, and one analyst carries a “Strong Sell” recommendation.

The broader analyst community also still sees room for upside. The stock’s average price target of $201.85 represents potential upside of 56%. Meanwhile, the Street-High target of $320 implies a gain of 147.3% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)