While the rest of Wall Street stayed busy chasing the next artificial intelligence (AI) chip darling, Stanley Druckenmiller was doing what he does best, picking winners before the crowd even catches on.

Through his Duquesne Family Office, Druckenmiller scooped up 1.89 million shares of Caris Life Sciences (CAI) during Q1 FY2026, a precision medicine company most investors have never come across, parking $33.87 million into the position.

The move signals serious confidence in cancer diagnostics from one of the sharpest minds in the business. Caris now takes up about 1% of his total portfolio, earning its place as one of his key healthcare bets as he broadens his biotech exposure well beyond traditional tech giants.

What makes the bet worth paying attention to is what Caris has actually been delivering. The company stepped into public markets in June 2025, pricing its IPO at $21 per share and pulling in roughly $424 million under the ticker CAI. Since then, it has barely paused for breath.

In Q1 FY2026, Caris posted a roughly 79% revenue surge while crossing into profitability, marking a genuine inflection point after years of heavy capital investment. In the same quarter, the company backed more than 6,100 ordering oncologists, and completed 52,800 cases, a 15% year-over-year (YOY) growth.

Druckenmiller clearly sees the bigger picture in this patient-centric approach to fighting cancer through data-driven insights.

About Caris Life Sciences Stock

To understand why this company has caught a billionaire's eye, it helps to know what it actually does. The Irving, Texas-based Caris Life Sciences is an AI-powered precision medicine company focused on cancer diagnostics and molecular research. The company delivers tissue-based and blood-based genomic profiling through whole genome, whole exome, and transcriptome sequencing.

Caris currently commands a market cap of $4.23 billion. Its platforms help physicians connect patients with targeted therapies, identify cancers earlier, monitor residual disease, and support biopharma drug discovery along with clinical development programs.

However, the stock has taken a serious beating since its debut. Caris’ shares have fallen 42.51% year-to-date (YTD), with the past three months alone delivering a 20.58% decline, and the most recent month piling on with another 26.98% plunge.

Even so, the market is pricing the stock at a meaningful premium to industry averages. CAI stock currently trades at 102.42 times forward adjusted earnings and 4.21 times sales, reflecting just how much growth the market expects it to deliver.

A Closer Look at Caris Life Sciences’ Q1 Earnings

Caris’ growth expectation got a solid shot in the arm on May 7, when the company released its Q1 FY2026 results. Total revenue jumped 78.8% YOY to $216.2 million, with Molecular Profiling Services doing most of the heavy lifting, climbing to $211 million in the quarter for an 84.8% surge YOY.

The top-line momentum also pulled gross margins significantly higher, reaching 65% on a GAAP basis, up sharply from 47% in Q1 of the prior year. The net loss, meanwhile, narrowed significantly to $553 thousand.

Beneath the headline numbers, the operational story was even better. The company kept investing at pace while holding the line on financial discipline, generating positive adjusted EBITDA of $26.2 million alongside positive free cash flow of $22.5 million, marking the fourth consecutive quarter that Caris delivered on both fronts.

The consistency gave the balance sheet room to breathe as well, with cash on hand rising to just above $825 million. Building on that financial momentum, the company refinanced its credit facility on attractive terms, locking in a new $400 million debt facility with a strong set of structural advantages.

Looking forward, analysts project FY2026 EPS at $0.10, a 130.3% YOY increase. Meanwhile, FY2027 EPS estimates sit at $0.37, pointing to 270% growth from the previous year.

What Do Analysts Expect for Caris Life Sciences Stock?

Wall Street has not given up on Caris Life Sciences despite the selloff, with analysts still calling for meaningful upside even as some quietly lower their targets.

Patrick Donnelly from Citigroup lowered his price target on CAI stock from $35 to $28. Still, he kept a “Buy” rating, signaling that he believes Caris still has enough firepower left in the tank despite recent pressure on the shares. Meanwhile, Mark Massaro at BTIG cut his price target to $32 from $38 while maintaining his “Buy” rating.

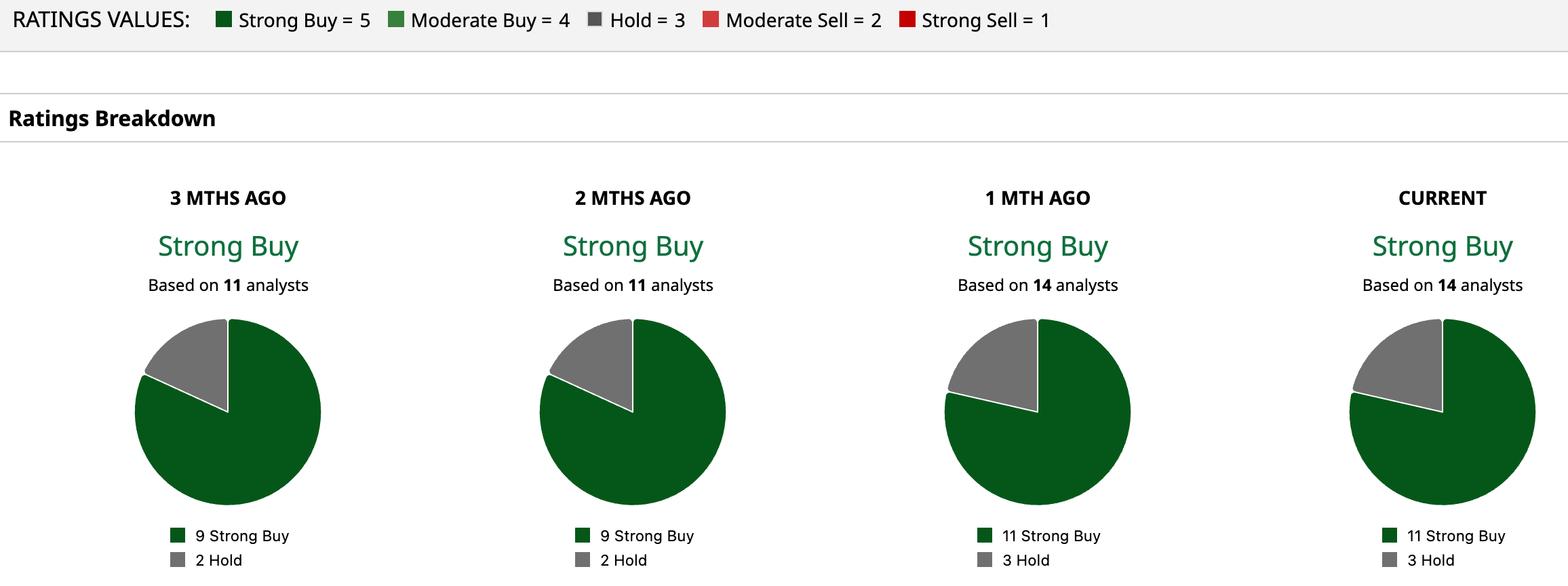

Wall Street has collectively assigned CAI stock an overall rating of "Strong Buy." Of the 14 analysts covering the stock, 11 assign it a "Strong Buy," while the remaining three sit on the fence with a "Hold."

The stock’s average price target of $28 represents potential upside of 78.6%. Meanwhile, the Street-High target of $36 could suggest a gain of 129.6% from current levels, if Caris keeps its growth engine humming and continues delivering strong clinical profiling demand.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/McDonald's%20Corp%20arches%20by-%20TonyBaggett%20via%20iStock.jpg)