Alignment Healthcare, Inc. (ALHC), a fast-growing Medicare Advantage company, produced strong revenue and adjusted EBITDA results in Q1. That may be the underlying reason for the huge, unusual ALHC call option activity today.

ALHC is at $16.44 in midday trading, well below its April 30 peak of $22.50 (before the after-market Q1 earnings release). Some institutional investors may be taking advantage of this drop by buying large amounts of call options.

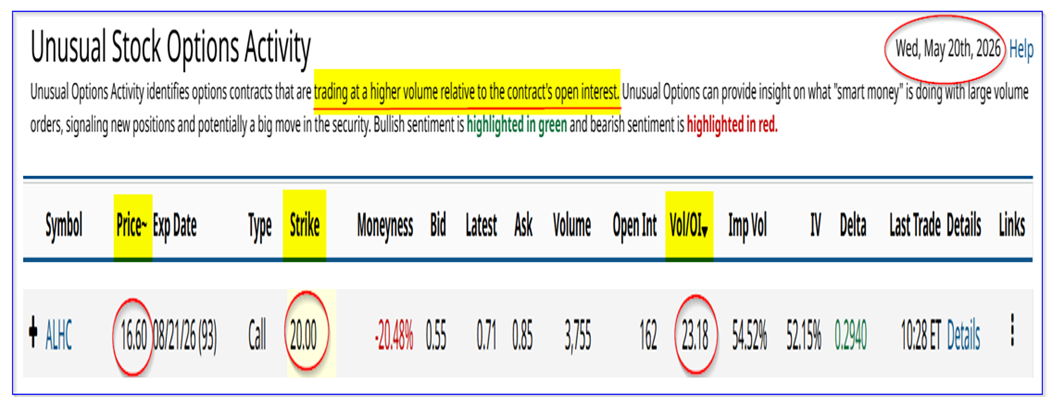

This can be seen in today's Barchart Unusual Stock Options Activity Report. It shows that over 3,700 call options contracts have traded at the $20.00 strike price expiring Aug. 21, 93 days from now.

That shows that the buyers of these calls are very bullish on ALHC. They are willing to pay 71 cents at the midpoint for these call options. That means the all-in cost for an investor in these call options is $20.71, or +26% over today's price, over the next 3 months.

Moreover, the buyers of these calls may not have to exercise these options to make a profit. They could take advantage of any increase in the premium if ALHC rises towards the strike price.

The point is that they see ALHC as undervalued here. After all, as of April 30, it was up to $22.50, so the $20.00 strike price could be seen as a good buy-in point. Let's look at its underlying value.

Alignment Healthcare's Strong Results and Forecast

Alignment Healthcare focuses on seniors who choose its Medicare Advantage program as subscribers. The U.S. government (i.e., the Centers for Medicare and Medicaid Services, or CMS) pays Alignment for every Medicare Healthcare (Plan C) member. This is because its Plan acts as an alternative to traditional Medicare plans, whose healthcare services CMS would otherwise cover.

Alignment does not charge a subscription fee to its members, so 100% of its revenue comes from CMS. As a result, it has to grow premium revenue by increasing its membership.

Last quarter, its revenue rose 33.3% YoY as its membership ranks rose 30.9% from 217,900 last year Q1 to 284,800 in Q1 2026, as shown in its 10-Q filing.

As a result, its adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization), a cash-flow measure, was $37.9 million, up 87.6% YoY. This was also higher than the high-end $36 million in adj. EBITDA projected in last quarter's outlook.

That makes its existing outlook seem conservative. For example, Alignment is now projecting between $50 and $60 million in adj. EBITDA for Q2. That would represent a 45% increase over the Q1 adj. EBITDA (i.e., $55m/$37.9m). If it comes in higher than that, it could be over 50% QoQ growth.

Moreover, it implies that the adj. EBITDA margin could rise from 3.1% last quarter to 4.2% (i.e., $55m/$1,305m revenue forecast).

As a result, the underlying value of ALHC stock could be higher.

ALHC Adj. EBITDA Projections and Price Targets

For example, analysts now project revenue this year will rise to $5.19 billion in 2026 (up +31.4% from $3.949 in 2025), and $6.51 billion in 2027. That implies over the next 12 months (NTM), the average revenue could rise to $5.85 billion, up 48.1% over 2025.

As a result, if Alignment Healthcare's adj. EBITDA margin hits 4.2%, the adj. EBITDA could reach $246 million:

0.042 x $5.85 billion = $245.7 million

That would be 53% higher than the high-end $160 million adj. EBITDA projection for 2026 that management provided in its Q1 earnings release.

As a result, using a 20x multiple on this forecast, Alignment Healthcare's market value could rise to over $4.9 billion:

20 x $245.7 million adj. EBITDA = $4,914 million

That is 45% higher than today's market cap of $3.39 billion, using Yahoo! Finance's calculation.

In other words, the price target (PT) could be $23.84 per share:

$16.44 price today x 1.45 = $23.84 PT

Other analysts believe ALCH is undervalued as well. For example, 14 analysts surveyed by Yahoo! Finance believe ALHC is worth $25.15 per share, or 52% higher. Similarly, Barchart's mean analyst survey PT is $25.15.

This could explain why some investors are buying 93-day call options. They may see ALHC as deeply undervalued. That could also be if its Q2 earnings come in stronger than expected, as its Q1 report did.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)