/Palo%20Alto%20Networks%20Inc%20HQ%20sign-by%20Tada%20Images%20via%20Shutterstock.jpg)

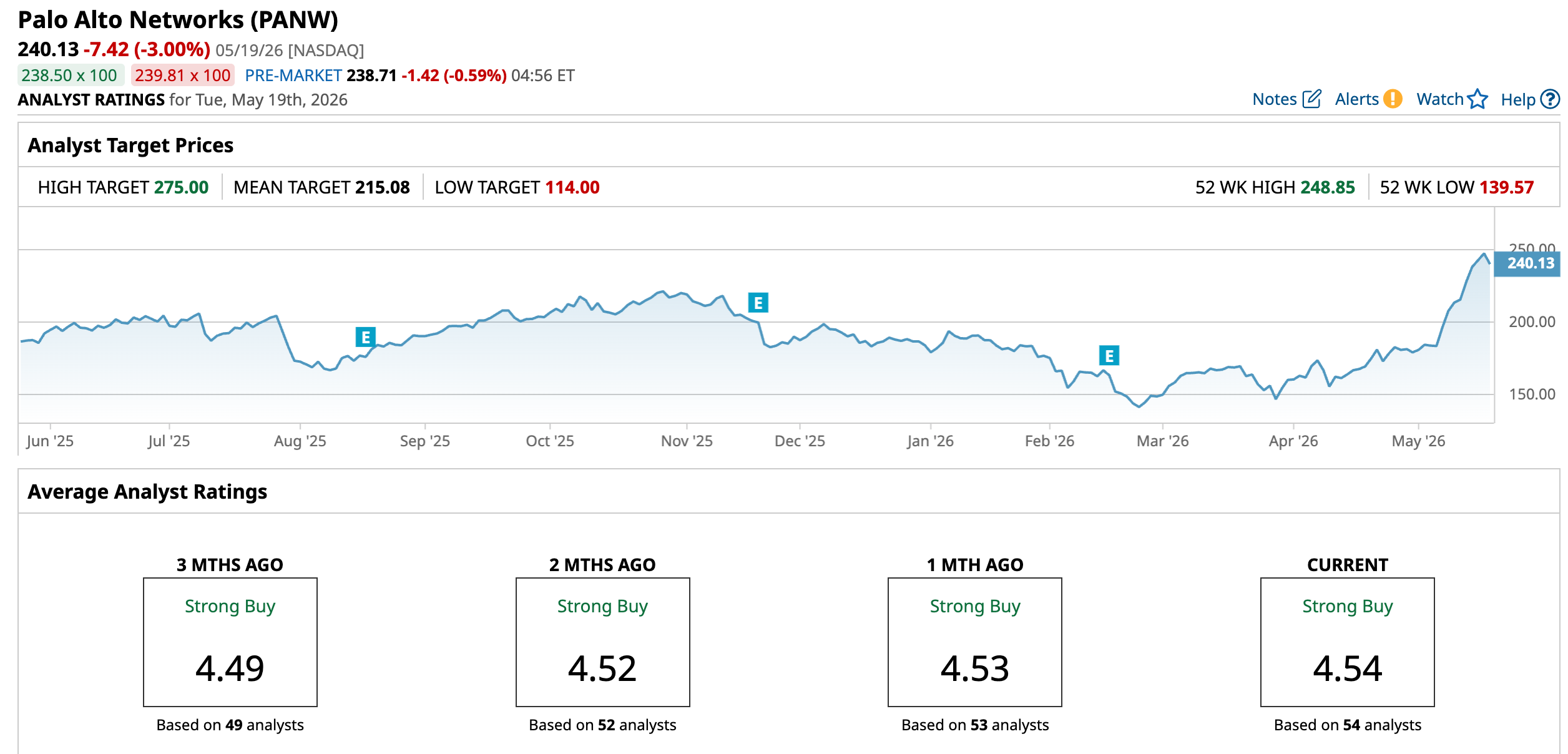

Cybersecurity giant Palo Alto Networks (PANW) is set to report its third-quarter earnings for fiscal 2026 on June 2 after the market closes. Ahead of that crucial date, Oppenheimer analyst Ittai Kidron lifted the price target on the stock from $245 to the current Street-high of $275, while maintaining an “Outperform” rating.

The adjustment was made after the CyberArk IMPACT 2026 event, where the firm unveiled Idira, its next-generation identity security platform, following Palo Alto Networks' $25 billion acquisition of CyberArk in February and its entry into the identity space.

At this juncture, we take a deeper look into Palo Alto Networks…

About Palo Alto Networks Stock

Palo Alto Networks is a global cybersecurity company that builds and operates integrated security platforms to protect organizations across networks, cloud environments, and endpoints. Headquartered in Santa Clara, California, the company focuses on delivering advanced firewall, cloud security and security operations solutions that help enterprises defend against modern cyber threats while enabling secure digital transformation. The company has a market capitalization of $202 billion.

Palo Alto Networks has benefited from increasing demand for cloud‑native security, zero‑trust frameworks, and its integrated platform, which helps organizations defend distributed networks and endpoints more efficiently. Over the past 52 weeks, the stock has gained 23.6%, while it has been up 30.36% year-to-date (YTD). The company’s shares reached a 52-week low of $139.57 on Feb. 24, but are up 72% from that level.

Palo Alto Networks' 14-day relative strength index (RSI) has risen to 78.40, which puts the stock in the overbought territory. On a forward-adjusted basis, its price-to-earnings (non-GAAP) ratio of 67.07 times is considerably higher than the industry average of 24.36 times.

Palo Alto Networks Beat Q2 Estimates on Strong AI‑driven Cybersecurity Demand

The growth driver in Q2 FY2026 (quarter ended Jan. 31) for Palo Alto Networks has been the trend of platformization, which refers to consolidating multiple cybersecurity tools and processes into a unified platform. There was a 35% year-over-year (YOY) growth in total platformizations, with about 110 net new platformizations during the quarter. NRR among platformized customers was healthy at 119%, with low single-digit churn.

AI has been the main driver of this trend, as AI customers seek to modernize and standardize their cybersecurity stack. The trend of adopting AI security has been steady. Moreover, the CyberArk and Chronosphere acquisitions are set to be significantly accretive. Palo Alto Networks' demand can be gauged by the company’s RPO climbing by 23% YOY to $16 billion. Additionally, its next-gen security ARR grew 33% to $6.33 billion.

Palo Alto Networks' Q2 revenue increased by 15% YOY to $2.59 billion, with subscriptions and support offerings being the major revenue drivers. Additionally, the top-line figure topped the $2.58 billion that Wall Street analysts had expected. Its non-GAAP operating margin inflated from 28.4% to 30.3%. Palo Alto Networks' non-GAAP EPS for the quarter was $1.03, up 27% YOY and above the $0.93 that Street analysts had expected.

And Wall Street analysts expect PANW's bottom line to grow robustly. For the ongoing fiscal year, profit is expected to increase by 30.5% annually to $2.14 per diluted share, followed by a 6.1% growth to $2.27 in the next fiscal year. Analysts expect its EPS to remain unchanged YOY at $0.43 for Q3.

What Do Analysts Think About Palo Alto Networks’ Stock?

In addition to Oppenheimer analysts, several other analysts remain bullish on Palo Alto Networks' stock.

Mizuho analysts see the company continuing to benefit from its subscription and product revenues following favorable recent checks. The analysts see strength in Prisma SASE, XSIAM and Prisma Browser. While the company expects remaining performance obligations (RPOs) to grow by 32%-33% YOY in Q3, Mizuho analysts believe the actual RPO figure could exceed the high end of that range. While maintaining a bullish “Outperform” rating, the analysts also raised the price target to $265 from $200.

Barclays analysts also raised the price target from $200 to $220 and maintained an “Overweight” rating, following “strong organic checks” going into the upcoming earnings. Also backed by channel checks with partners and customer contacts that came back positive, BTIG analysts raised PANW's price target from $200 to $216 while keeping a “Buy” rating.

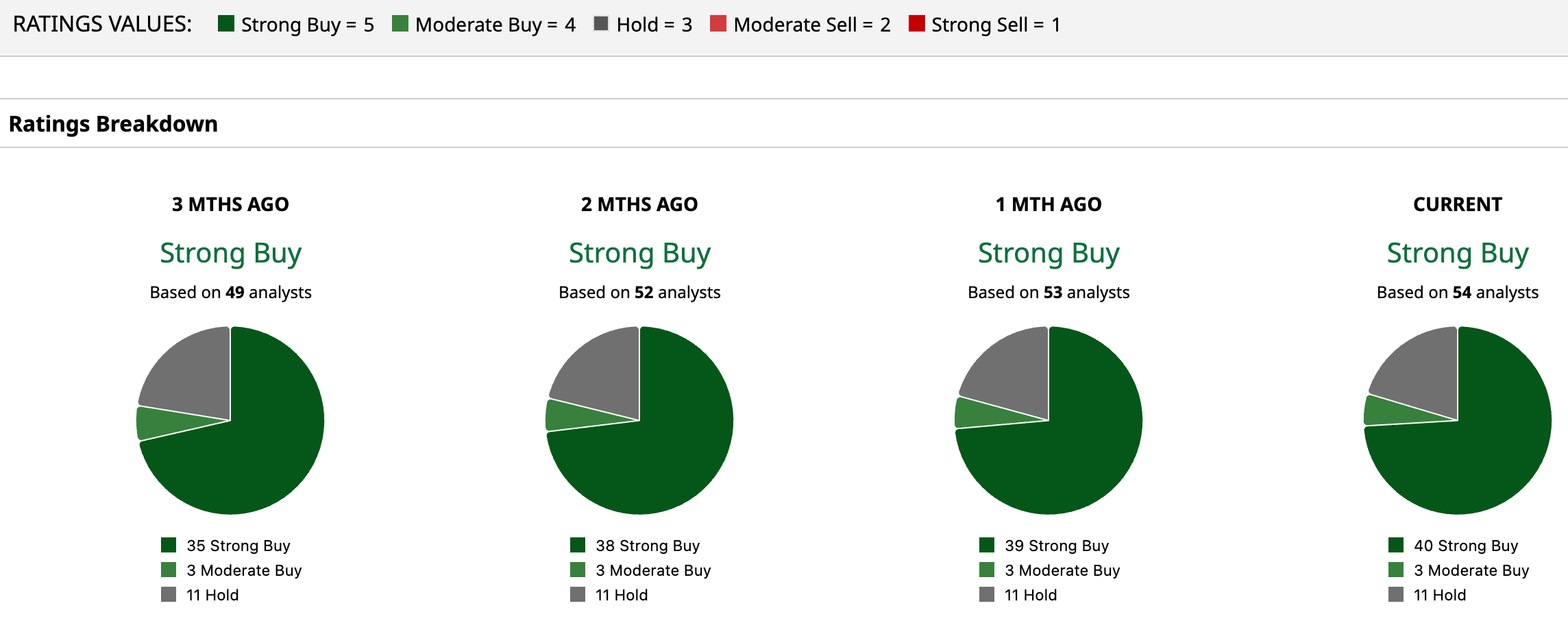

Palo Alto Networks remains a popular name on Wall Street, with analysts awarding it a consensus “Strong Buy” rating overall. Of the 54 analysts rating the stock, a majority of 40 analysts have given it a “Strong Buy” rating, three analysts gave a “Moderate Buy,” while 11 analysts are taking the middle-of-the-road approach with a “Hold” rating. The consensus price target of $215.08 represents a 10.4% downside from current levels. However, the Street-high price target of $275 indicates an 14.5% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)