Every time an enterprise spins up a new artificial intelligence (AI) deployment, it also hands hackers a brand-new attack surface, and someone has to lock that door. Rising digital threats and increasingly sophisticated AI-driven attacks are forcing companies across every industry to open their wallets wider on security tools.

CrowdStrike Holdings (CRWD) plants its flag right at the center of this spending boom. The company has engineered its AI security business into one of its most powerful long-term growth engines, and Founder and CEO George Kurtz made no effort to hide his satisfaction. In the company's most recent earnings release he declared FY26 the best year in CrowdStrike's history.

Management fingered AI as the primary magnet pulling enterprise customers toward its Falcon platform because today's businesses need security that simultaneously covers AI workloads, AI agents, cloud infrastructure, and employee AI usage all sitting neatly under one roof. The consolidated demand is Falcon's sweet spot.

So, anyone still asleep on AI turning into CrowdStrike’s biggest moneymaker might want to wake up by Wednesday, June 3, when Q1 FY2027 earnings hit after market close.

About CrowdStrike Stock

Based in Austin, Texas, CrowdStrike provides cloud native cybersecurity through its Falcon platform, which detects threats and stops breaches across on premise, virtualized, and cloud environments while securing endpoints such as laptops, servers, virtual machines, and IoT devices.

Today, CrowdStrike carries a market cap of $156.9 billion and offers 33 cloud modules on the Falcon platform through a software-as-a-service (SaaS) model spanning multiple large security markets.

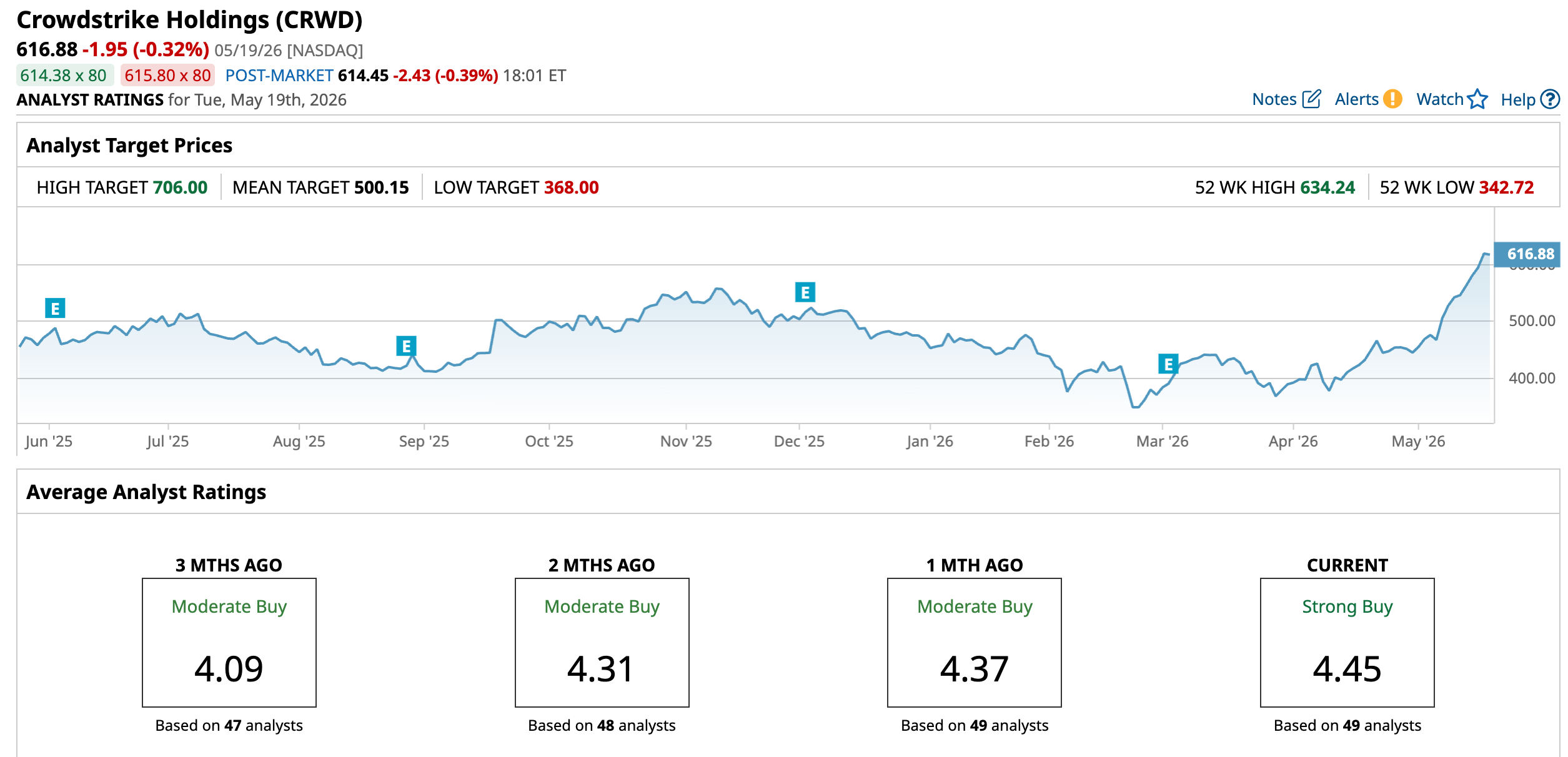

The stock has rewarded its believers handsomely along the way. CRWD stock surged 38.83% over the past 52 weeks. The rally continued into 2026, with the shares climbing 31.6% year-to-date (YTD) before tacking on another 45.5% jump in the last month alone.

Naturally, that kind of run pushes valuations into premium territory. CRWD stock is now trading at 127.48 times forward adjusted earnings, which sits above the industry benchmark but actually comes in at a discount relative to the stock's own five-year average multiple.

CrowdStrike Surpasses Q4 Earnings

On March 3, CrowdStrike posted Q4 FY2026 results that comfortably beat Wall Street expectations. This led the stock to rise 1.7% that day before surging another 4.2% in the following trading session.

The numbers behind the move were hard to argue with. Revenue grew 23.3% year-over-year (YOY) to $1.31 billion, beating analyst estimates of $1.30 billion, while adjusted EPS climbed 38.3% from the previous year’s period to $1.12, topping the Street's forecast of $1.10.

Also, the company crossed $5.25 billion in ending annual recurring revenue (ARR), becoming the fastest and the only pure play cybersecurity software company to reach that mark, driven by a record $1.01 billion in net new ARR and its first-year surpassing $1 billion in net new ARR growth.

Profitability told the same strong story. Non-GAAP income from operations climbed 44.9% YOY to $325.8 million, non-GAAP net income came in at $289.1 million, up 40.8% from the last year’s quarter, and free cash flow grew 56.9% from the year-ago value to $376.4 million.

With the momentum in its corner and a record Q1 pipeline entering FY2027, management has raised its FY2027 ARR outlook with strong conviction, viewing the AI revolution as a generational growth opportunity while staying fully confident in delivering durable, profitable growth on the path to its goal of $20 billion ending ARR in FY2036.

In addition, the guidance reflects confidence. For Q1, CrowdStrike’s management expects revenue between $1.360 billion and $1.364 billion, with adjusted EPS between $1.06 and $1.07. For the full year, fiscal 2027 revenue is projected between $5.87 billion and $5.93 billion, with adjusted EPS between $4.78 and $4.90.

Analysts are forecasting even bigger things further out. Q1 FY2027 EPS is expected to surge 156.5% YOY to $0.13. The FY2027 bottom line could jump 2,650% from the prior year to $1.02, and FY2028 EPS is forecasted to rise 64.7% YOY to $1.68.

What Do Analysts Expect for CrowdStrike Stock?

The analyst community is largely throwing its weight behind CrowdStrike heading into June 3. BTIG analyst Gray Powell raised the price target on CRWD stock to $621 from $499 and held a “Buy” rating ahead of Q1 FY2027 results, pointing to channel checks that signal CrowdStrike's platform consolidation pitch is winning more enterprise security wallets.

KeyBanc's Eric Heath went a step further, raising the CRWD’s price target to $700 from $525 and reiterating an “Overweight” rating, citing improving demand signals.

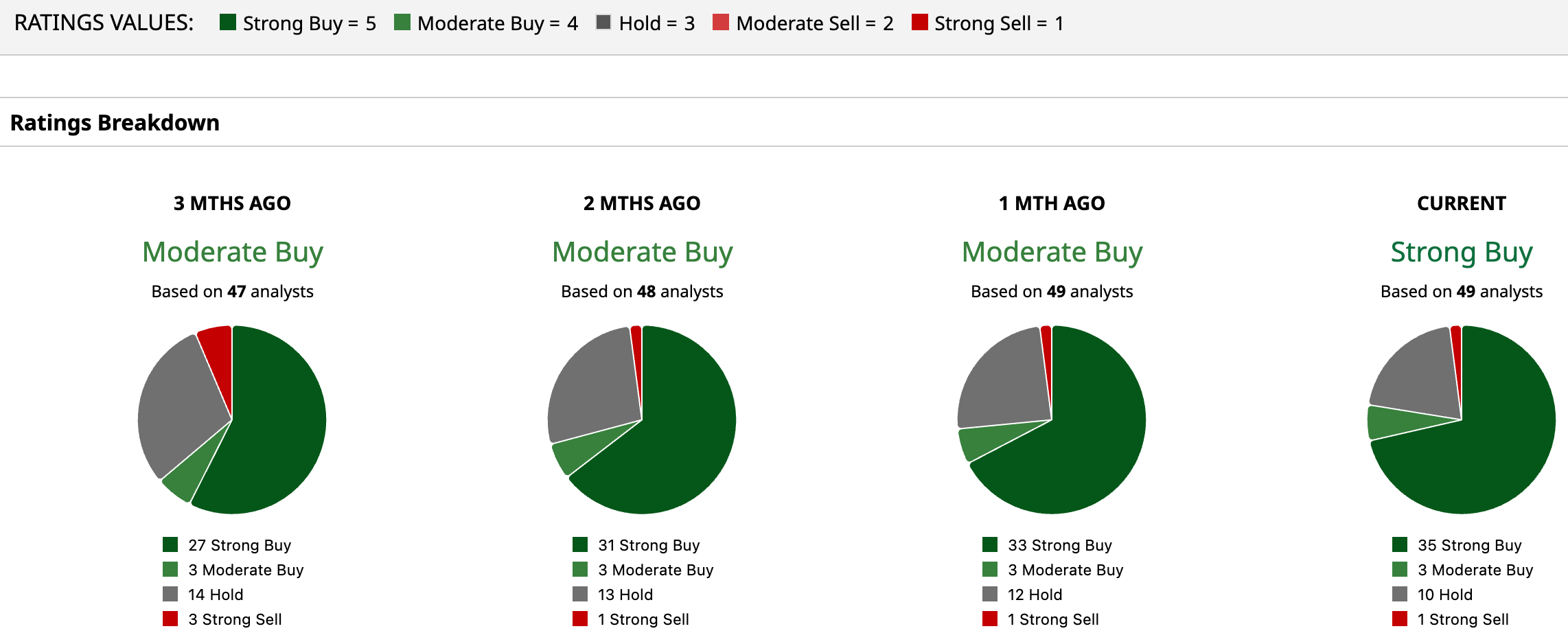

The broader Wall Street picture lines up with that bullish tone as the stock carries an overall rating of “Strong Buy.” Among the 49 analysts covering the stock, 35 rate it a "Strong Buy," three assign a "Moderate Buy," 10 stick with "Hold," and one calls for a "Strong Sell."

Interestingly, CrowdStrike stock already trades above the average analyst price target of $500.15. Meanwhile, the Street-High target of $706 suggest a gain of 14.5% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/Friends%20choosing%20a%20movie%20on%20a%20streaming%20service%20by%20Stock-Asso%20via%20Shutterstock.jpg)