Thin Herds, High Stakes: What Has Been Driving the Cattle Tape

The foundation underneath this market is straightforward and structural. The U.S. cattle herd stood at 86.2 million head as of January 1, 2026, its smallest size since 1951. The beef cow herd has been contracting for eight consecutive years, and the cattle cycle is now in its 13th year of the same downcycle. Supply recovery cannot be rushed; a cow takes nine months to gestate and another 18 to 24 months for the calf to reach slaughter weight, meaning most analysts do not expect meaningful new supply to reach the market before 2028.

On top of this already-tight backdrop, the market received a significant additional supply shock beginning in May 2025 when the U.S. suspended live cattle imports from Mexico after New World Screwworm cases were detected as far north as Oaxaca and Veracruz. Mexico historically supplies approximately 62% of all U.S. live cattle imports, primarily lightweight feeder cattle destined for stocker and feedlot operations. As of mid-May 2026, APHIS confirmed 1,701 active New World Screwworm cases in Mexico, with 139 active cases in the bordering state of Tamaulipas, including 7 within 96 to 97 miles of the U.S. border. The border closure remains in effect and continues to remove an estimated 1.2 million head annually from the Southern feedlot supply pipeline. Nebraska wildfires earlier in 2026 added a further layer of disruption, destroying grazing land and forcing cattle to market ahead of schedule.

Against this background, the most market-moving developments of the past week centered on Washington. On May 12, the Trump administration acknowledged it was "fine-tuning" executive orders that had been expected to temporarily suspend tariff-rate quotas on all beef-exporting nations for 200 days, a move that would meaningfully increase import volumes. The original announcement on May 11 rattled futures, prompting fund liquidation and algorithm-driven selling. The subsequent delay and reframing of the executive orders brought buyers back, with live cattle futures climbing Wednesday as market participants took comfort in the implied slowing of the import relief package. Trump's previous efforts to bring beef prices down, including quadrupling imports from Argentina in late 2025 and removing a 40% punitive tariff on Brazilian beef a month later, had little lasting impact on prices, which were still up 12.1% year-over-year in the April Consumer Price Index. The USDA is now projecting a record 5.8 billion pounds of beef imports in 2026, up 25% from 2024. Beef demand, by contrast, remains historically robust; the LMIC beef demand index reached 138 in 2025, its highest level ever recorded.

Geopolitically, the ongoing U.S.-Iran conflict is relevant primarily through its energy channel. The breakdown of peace talks over the weekend of May 10 to 11 sent crude oil sharply higher, injecting inflationary pressure across commodity markets broadly and supporting the broader macro bid in agricultural futures. That energy dynamic remains a background factor supporting the general commodity complex.

What has the Market done?

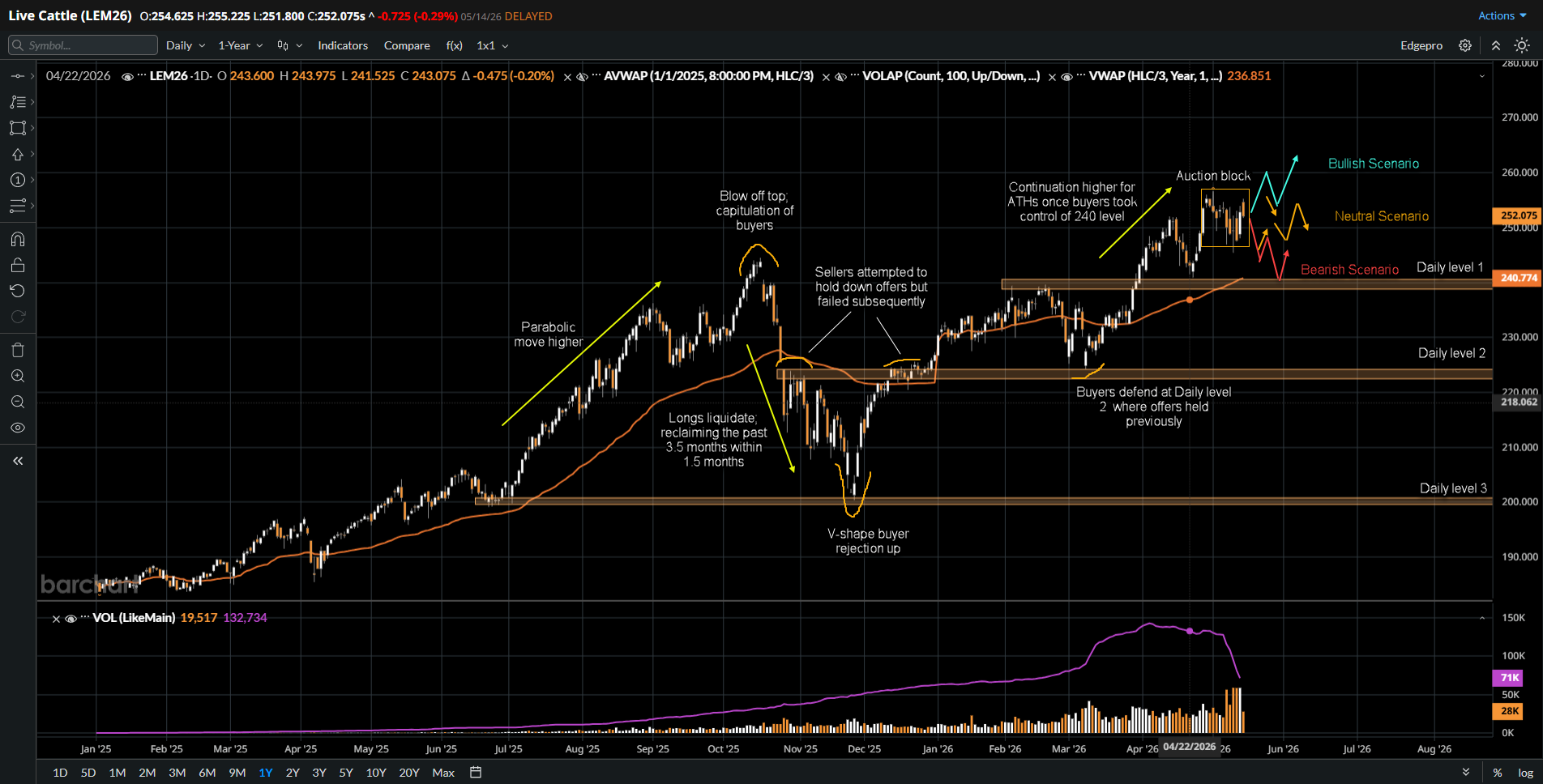

- Market was in an uptrend throughout 2025 and entered a parabolic move higher during the second half of the year, as a historically tight cattle supply, combined with record beef demand to attract aggressive speculative fund participation.

- The market experienced a blow-off top in mid-October and printed fresh all-time highs on the December contract above the 244 level before buyers capitulated, triggering aggressive liquidation as participants began pricing in the risk of government intervention to suppress beef prices.

- Price rotated sharply lower and took just 1.4 months to move back toward the 200 level, where buyers aggressively defended the area, the structural floor supported by the same underlying supply deficit that had driven the original advance.

- That defense triggered a sharp rejection and V-shape recovery as buyers stepped back into the market, reasserting the fundamental case for tight cattle supplies with no meaningful new stock expected before 2028.

- Live cattle expanded higher and fully reclaimed the prior selloff, with the recovery underpinned by three compounding supply shocks hitting simultaneously in early 2026, the ongoing Mexico border closure removing an estimated 1.2 million head annually, Nebraska wildfires pushing cattle to market early, and continued feedlot placements running well below year-prior levels.

- Sellers emerged near the 240 level, creating rotational price action lower, as concerns around potential government import relief began to surface again in early 2026.

- Buyers stepped up bids near 220 and regained control, with the structural supply narrative overwhelming the policy noise; cash trade at the time continued to confirm tighter-than-expected slaughter volumes and firm packer demand.

- The market has now resumed higher and pushed into fresh all-time highs, with the April 2026 contract printing 252.25, a new all-time high for any live cattle futures contract, and cash trade crossing 250.00 per hundredweight in the North for the first time in history, confirming buyers remain in control of broader trend structure.

What to Expect in the Coming Weeks

The key level to watch is 240 (daily Level 1 and the developing yearly VWAP).

Bullish Scenario

- If buyers are able to break to new ATHs and push through to the 260 level, and sustain above the AB block on pullbacks, expect continuation higher for fresh all-time highs into the summer grilling season peak demand window.

- A possible macro trigger for this scenario would be the Trump administration formally abandoning or significantly watering down the beef import executive orders, removing the near-term supply relief overhang that has been the primary source of seller pressure. A continued stalemate in U.S.-Iran ceasefire negotiations sustaining elevated energy prices could also add a broader inflationary bid to the commodity complex, supporting cattle alongside other ag markets.

Bearish Scenario

- If buyers are not able to defend the 245 area (Auction block low), expect a move down to the 240 level (daily Level 1), which would be confluent with the projected 2026 yearly VWAP, where buyers are expected to respond.

- A possible macro trigger for this scenario would be a signed executive order formally suspending tariff-rate quotas on beef imports from all exporting nations for 200 days, as originally drafted. Fund and algorithmic liquidation would likely accelerate on a break below 245, with buyers expected to respond at the VWAP / Level 1 confluence around 240, keeping the broader uptrend structure intact.

Neutral Scenario

- A possible two-way auction within the Auction block as the market compresses and builds value higher before further directional resolution. Price could range between 245 and 255 as the market waits for clarity on the import tariff situation and digests current cash trade levels.

- A possible macro trigger for this scenario would be the White House continuing to "fine-tune" its executive actions without actually signing anything, keeping both bulls and bears uncertain. Steady cash trade in the 256 to 260 range with no dramatic improvement or deterioration in feeder cattle availability or New World Screwworm border status would also support a sideways, value-building consolidation.

Conclusion

Live cattle futures remain in a structural uptrend, underpinned by the most severe supply deficit in over 70 years and beef demand that has consistently refused to buckle despite record retail prices. The market has demonstrated its willingness to defend value at every meaningful pullback, and buyers have responded each time with conviction. As long as price holds above the developing 2026 yearly VWAP at 240, the broader bull trend remains intact and any weakness in the coming weeks is best framed as a pullback within that trend rather than a structural reversal. In the near term, the market remains acutely sensitive to Washington's next move on beef import tariffs, with the delayed executive order on tariff-rate quotas acting as the primary wildcard that could dictate whether the next few weeks see continuation to 260, a brief pullback to the 240 VWAP level, or a period of two-way auction as the market builds value and waits for resolution. The fundamental tailwind from summer grilling season demand is approaching, and the supply picture is not getting easier anytime soon.

We provide the infrastructure you need to quantify your discipline and ensure every decision is backed by the confidence of seeing exactly what drives your performance. Start trading with the clarity you deserve. Open an Account today.

Disclaimer:

This article is provided for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis presented reflects the author’s market observations and opinions at the time of writing and is not a recommendation to buy or sell any futures contract, security, or financial instrument. Futures trading involves significant risk and is not suitable for all market participants. Losses may exceed initial margin deposits, and market conditions can change rapidly.

Any scenarios, levels, or market expectations discussed are hypothetical in nature and are intended solely to illustrate potential market behavior. They do not represent actual trading results and should not be interpreted as guarantees of future performance. Past performance, market behavior, or historical price action are not indicative of future outcomes.

Readers are solely responsible for their own trading decisions and risk management. Always conduct independent research, consider your financial situation and risk tolerance, and consult with a qualified financial professional, if necessary, before engaging in futures or derivatives trading.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)