Shares of Rocket Lab Corporation (RKLB) are soaring after the space company delivered a blowout earnings report that reinforced investor confidence in its long-term growth story and, more importantly, in the highly anticipated debut of its next-generation Neutron rocket later this year. Rocket Lab stock has skyrocketed following the results as Wall Street cheered record revenue, a rapidly expanding $2.2 billion backlog, and surging demand for future Neutron launches.

With Neutron positioned to compete in the lucrative medium-lift market currently dominated by SpaceX’s Falcon 9, bullish investors are betting the company could unlock a much larger commercial and defense opportunity if the launch is on schedule. Rocket Lab recently signed its largest launch agreement ever, including five dedicated Neutron missions stretching into 2029, signaling strong customer demand ahead of the planned debut.

About Rocket Lab Stock

Rocket Lab is a space infrastructure and launch company focused on small- and medium-lift rockets, satellite manufacturing, spacecraft components, and end-to-end space systems for commercial, government, and defense customers. The company is headquartered in Long Beach, California and operates launch facilities in New Zealand and the United States. Rocket Lab has become one of the fastest-growing players in the commercial space industry through its Electron launch vehicle and the upcoming Neutron rocket, which is expected to significantly expand its addressable market. Following a sharp rally in the stock, the company’s market cap stands at $67 billion.

Shares of Rocket Lab have been on an extraordinary run lately, transforming the company into one of the market’s hottest momentum names amid growing enthusiasm around its Neutron rocket program and expanding defense contracts. The stock has surged 79% year-to-date (YTD) and is up 472% over the past 52 weeks, massively outperforming both the broader market and most aerospace peers.

The rally intensified following Rocket Lab’s blockbuster first-quarter earnings report, with shares exploding 34.2% in a single session on May 8 after the company posted record revenue, raised guidance, and announced its largest launch agreement ever.

Momentum continued into the following trading session. On May 11, RKLB jumped another 11.3% as investors continued to price in optimism surrounding the planned Neutron launch later this year. Additionally, RKLB touched a fresh 52-week high of $123.94 on May 11, with trading volume surging far above normal levels. Over the past five trading days alone, Rocket Lab shares have delivered gains of 47.5%.

The stock is trading at a premium at price-to-sales (TTM) at 96.12 times compared to industry peers at 1.96 times.

Neutron Launches Can Be a Solid Boost

Rocket Lab’s Neutron program is widely viewed as the company’s most important long-term growth catalyst and a potential game changer for its competitive position in the global launch market. Designed as a reusable medium-lift rocket capable of carrying up to 13,000 kilograms to orbit, Neutron is intended to compete directly with SpaceX’s Falcon 9 for commercial satellite deployments, national security missions, and constellation launches.

The company said the rocket remains on track for its debut launch later this year, with management highlighting continued progress on Archimedes’ engine, reusable fairing systems, second-stage development, and first-flight hardware integration during its latest earnings release.

Evidently, investor enthusiasm around Neutron has intensified following Rocket Lab’s announcement of its largest launch contract ever. The deal is viewed as a major validation of customer demand for the rocket even before its inaugural flight and expands the company’s total launch manifest to more than 70 missions.

Strong Quarterly Performance

Rocket Lab reported fiscal first-quarter 2026 results on May 7, delivering another record-setting quarter that significantly exceeded Wall Street expectations. The company generated record quarterly revenue of $200.3 million, representing a 63.5% year-over-year (YOY) increase. Adjusted EBITDA loss narrowed substantially to $11.8 million, while loss per share improved to $0.07 from $0.12 a year earlier and exceeded expectations.

Additionally, non-GAAP gross margin reached 43%, compared to 33.4%. Product revenue climbed 57.8% YOY to $127.5 million, driven by continued strength in space systems and satellite components, while services revenue rose significantly to $72.9 million.

One of the biggest highlights from the quarter was Rocket Lab’s explosive backlog growth. Total backlog surged to a record $2.2 billion, up 20.2% sequentially, reflecting rapidly increasing demand across launch services, defense programs, and space systems.

Management disclosed that the company signed 31 new Electron and HASTE launch contracts during the quarter, along with five dedicated Neutron launch agreements, pushing Rocket Lab’s total launch manifest above 70 contracted missions. Remarkably, Rocket Lab said it sold more launches in the first quarter of 2026 than it did during all of 2025.

The quarter also included several major strategic and defense-related contract wins. Rocket Lab announced its largest launch agreement in company history with a confidential customer that booked five dedicated Neutron launches and three Electron launches between 2026 and 2029.

On the other hand, the company is active in hypersonic testing under the MACH-TB program and expanded its collaboration with Raytheon (RTX) to support the U.S. Space Force’s Space Based Interceptor initiative tied to the “Golden Dome for America” missile defense effort.

Operationally, Rocket Lab continued advancing its broader space infrastructure ambitions beyond launch services. During the quarter, the company completed its acquisition of Mynaric AG, giving Rocket Lab a stronger foothold in optical communications. The company also entered into a definitive agreement to acquire Motiv, adding robotics, motion-control systems, and satellite component manufacturing capabilities that management believes will improve vertical integration and reduce supply-chain dependence.

Furthermore, the company forecast Q2 2026 revenue between $225 million and $240 million, implying another sequential record quarter. Management expects non-GAAP gross margin of 38% to 40%, and adjusted EBITDA loss between $20 million and $26 million as the company continues investing heavily in the development of its Neutron medium-lift rocket.

Analysts forecast a loss per share of $0.22 for fiscal 2026, an improvement of 42.1%, followed by a 68.18% advance to -$0.07 in 2027.

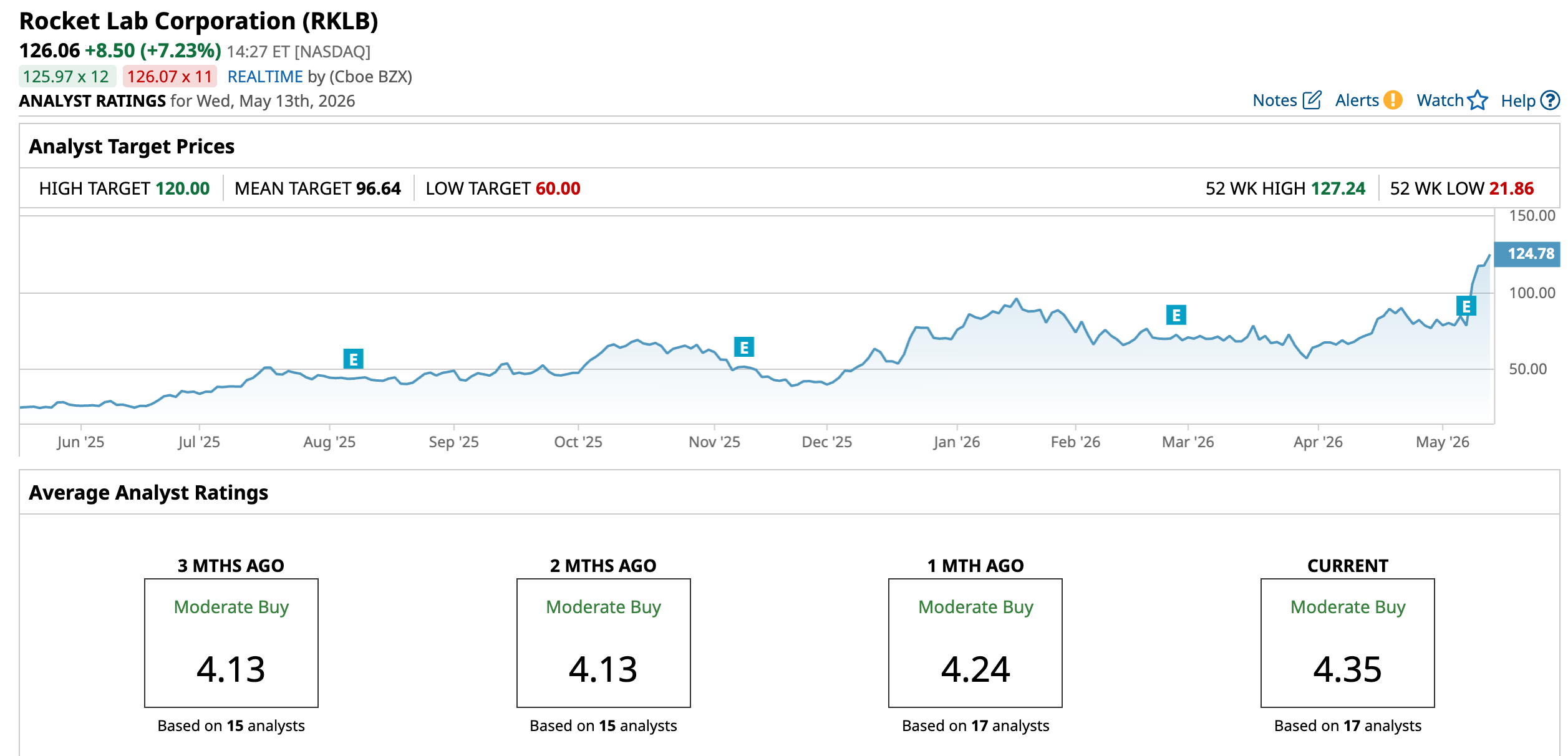

What Do Analysts Expect for Rocket Lab Stock?

This month, Cantor Fitzgerald raised its price target on Rocket Lab to $96 from $85 while maintaining an “Overweight” rating. The firm highlighted Rocket Lab’s Electron, Haste, and upcoming Neutron rockets, along with its commercial and government relationships across domestic and international markets, as major long-term growth drivers.

Also, Citizens raised its price target on Rocket Lab to $95 from $85 while maintaining a “Market Outperform” rating following the company’s strong fiscal first-quarter 2026 results.

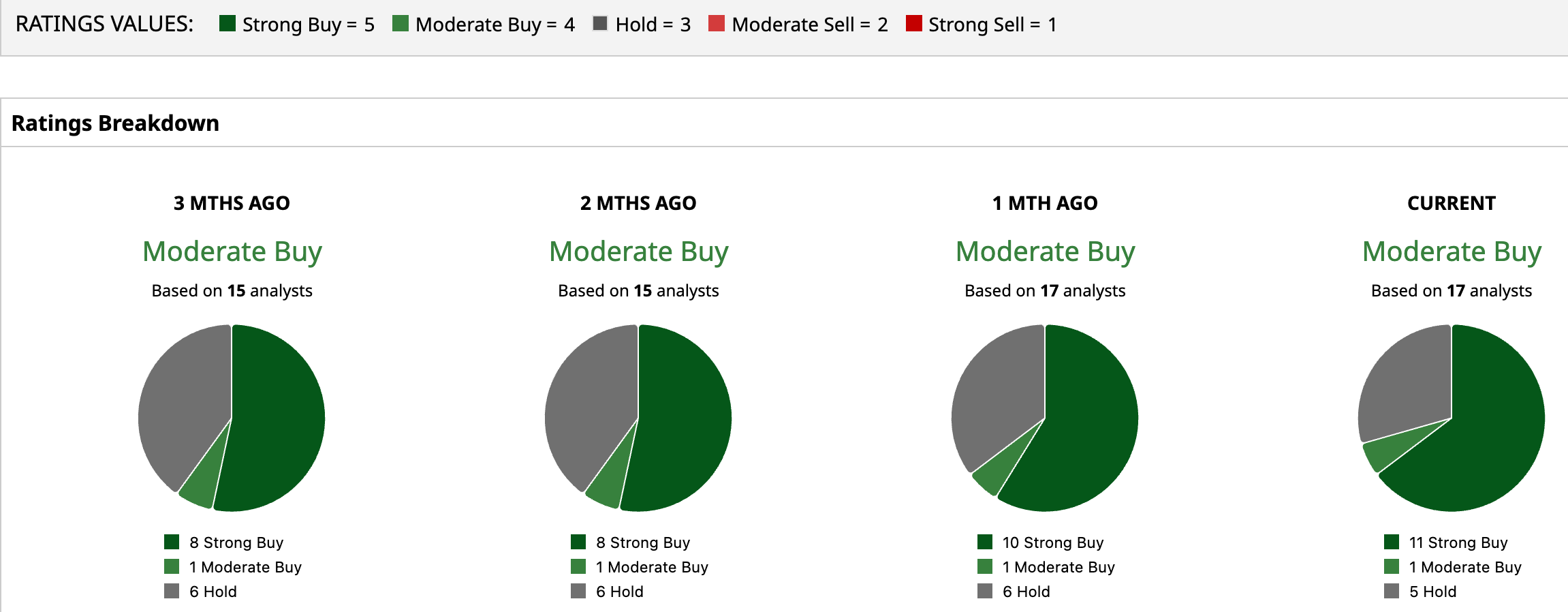

Overall, RKLB has a consensus “Moderate Buy” rating. Of the 17 analysts covering the stock, 11 advise a “Strong Buy,” one gives a “Moderate Buy,” and five suggest a “Hold.”

RKLB has already surged past its average analyst price target of $96.64 as well as the Street-high target price of $120, suggesting its solid momentum.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)