Coinbase (COIN) is cutting roughly 700 jobs, or about 14% of its total workforce. The announcement hit earlier this week and sent shares down 2.5%. But if you looked past the headline, the company's first-quarter earnings told a more nuanced story.

The layoffs were driven by a rough stretch for the broader crypto market and a push by management to rebuild Coinbase from the ground up as an artificial intelligence (AI) native company.

Whether COIN stock is worth buying, holding, or avoiding right now depends heavily on which of those forces you believe will define the company's next chapter.

Coinbase Is Focused on Cost Savings

Coinbase CEO Brian Armstrong laid out the rationale in a memo shared publicly on X earlier this week.

He described the cuts as necessary to position the firm for its next phase of growth while navigating the current market downturn. Armstrong cited two pressures hitting simultaneously: a pullback in crypto markets and AI rapidly reshaping how the company operates internally.

According to an SEC filing, the restructuring is expected to largely wrap up in the second quarter of 2026, with Coinbase incurring between $50 million and $60 million in related expenses.

Armstrong was direct. He said crypto is still on the verge of its next wave of adoption, but that the business remains volatile quarter to quarter. His goal is to emerge from this period leaner, faster, and more efficient.

Amrstrong also pointed to AI as a structural shift, not just a cost-cutting tool. "The pace of what's possible with a small, focused team has changed dramatically," he wrote, adding that Coinbase needs to return to the focused intensity of its founding days, with AI at its core.

A Mixed Performance in Q1

In Q1 of 2026, Coinbase reported revenue of $1.4 billion, down 21% year-over-year. It also posted a net loss of $394 million alongside $303 million in adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA), which marked its 13th straight positive quarter on that metric.

Chief Financial Officer Alesia Haas noted that the total crypto market cap and total crypto trading volume both fell more than 20% quarter over quarter, so the revenue decline tracked closely with market conditions rather than Coinbase losing ground competitively.

In fact, Coinbase reached a new all-time high in crypto trading market share during Q1. It was the 12th consecutive quarter of net native unit inflows. When markets get rocky, Haas said, customers tend to consolidate their activity on platforms they trust.

Clear Street analyst Owen Lau told CNBC the first quarter was expected to be weak given the crypto bear market. "The company wants to tell investors that management is actively managing the cost base to deliver positive adjusted EBITDA through the cycle," he said.

Coinbase Expands Product Moat

Buried inside the softer headline numbers were several meaningful bright spots.

- Coinbase's retail derivatives business hit more than $200 million in annualized revenue in Q1, a new high.

- Prediction markets, launched just two months before the quarter ended, were already generating more than $100 million in annualized revenue as of March.

- Stablecoin revenue came in at $305 million. The average amount of USDC held in Coinbase products reached a new all-time high of $19 billion.

- Coinbase distributes more than 25% of all USDC in existence and captures roughly half of all USDC economics. And crucially, that contract with Circle auto-renews every three years and cannot be terminated.

- The company now has 12 products generating more than $100 million in annualized revenue. Subscription and services revenue made up 44% of net revenue, a stabilizing factor when trading volumes soften.

On the AI front, the numbers are harder to value but potentially significant. Over 90% of on-chain agentic transaction volume during Q1 occurred on Base, Coinbase's own blockchain. USDC was used in 99% of those agent-to-agent transactions.

Armstrong called Coinbase the center of the agent economy, and Q1 data at least starts to back that claim up.

Is COIN a Good Stock to Buy Right Now?

It is not Coinbase's first time cutting costs during a downturn. The company made significant reductions during the 2022 crypto winter and came out the other side with its business intact and growing.

The bull case for COIN stock rests on a few things coming together: regulatory changes through the CLARITY Act, continued stablecoin adoption, derivatives and prediction markets scaling further, and AI infrastructure demand funneling through Base and USDC.

If these trends accelerate, the company's diversified revenue base and dominant market share position it well.

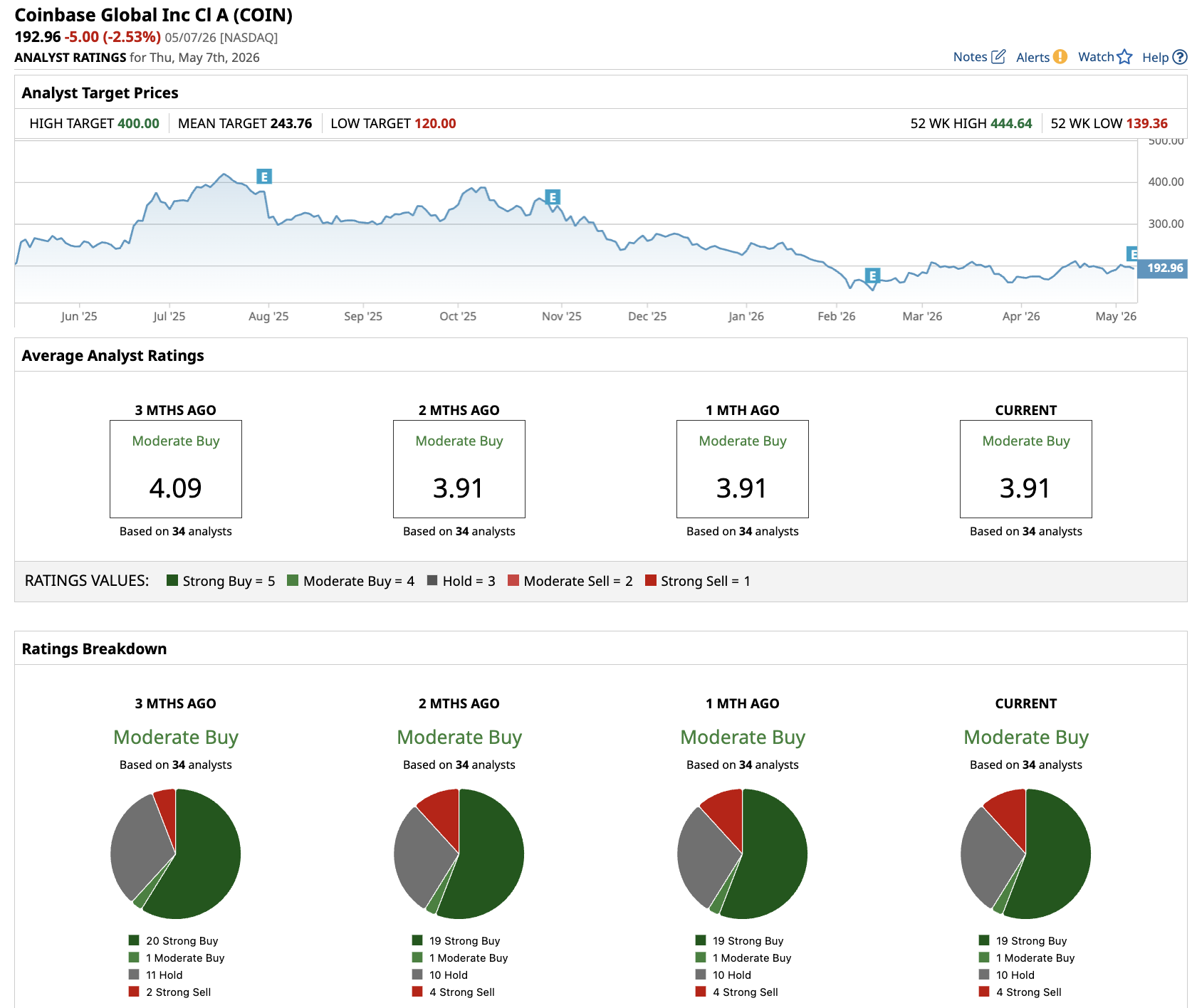

Out of the 34 analysts covering COIN stock, 19 recommend “Strong Buy," one recommends “Moderate Buy,” 10 recommend “Hold,” and four recommend “Strong Sell." The average Coinbase stock price target is $244, above the recent price of $193.

The risk is that crypto prices stay suppressed longer than expected, compressing the transaction revenue that still drives a meaningful share of total sales.

For investors with a longer time horizon, Coinbase's Q1 results suggest a company that is managing what it can control while betting on where finance is heading. But in the short term, this remains a volatile stock tied to an inherently volatile market.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)