/NVIDIA%20Corp%20logo%20on%20phone-by%20Evolf%20via%20Shutterstock.jpg)

After a strong earnings season, AI stocks have risen sharply as demand for AI infrastructure remains strong. This year, the tech-heavy Nasdaq Composite Index ($NASX) is up 12.25%, or more than 3,000 points. Wedbush’s Dan Ives believes that the Nasdaq can climb to 30,000 points this year if another bumper earnings season rolls in.

However, there have been concerns that the AI rally has gone too far, close to bubble territory, especially as sentiment grows that there is little hope of peace negotiations between the U.S. and Iran at the moment. Michael Burry of “Big Short” fame also believes the same, warning that the AI boom is beginning to look like the last stages of the dot-com bubble.

Against this backdrop, Bernstein analyst Stacy Rasgon believes that the AI-fueled semiconductor sector still has more room to run. Bernstein analysts remain bullish on chip behemoth Nvidia Corporation (NVDA) , stating that the stock is screening cheap right now. On a forward basis, NVDA’s price-to-earnings (non-GAAP) ratio of 26.31 times is only 5.9% higher than the 24.85 times industry average.

Nvidia, synonymous with AI now, has been bolstering its position in the market amid competitors gaining market share. In the fourth quarter of fiscal 2026, the company unveiled its Nvidia Rubin platform and entered a strategic partnership with Meta Platforms (META).

In fact, the company has been aggressively investing, pledging over $40 billion while broadening its holdings to include additional publicly traded stocks. Recent investments include a pledge of up to $2.1 billion to data center operator IREN Limited (IREN) and a $3.2 billion commitment to glass-maker Corning Incorporated (GLW).

As the chip giant steps up its game, we take a closer look at Nvidia prior to its upcoming earnings.

About Nvidia Stock

There’s not much that needs to be said about Nvidia because the company has been dominating the AI era for quite some time. Its cutting-edge graphics processing units (GPUs) and software platforms, such as CUDA, are fueling machine learning, data centers, autonomous vehicles, and robotics.

Nvidia is a near-monopoly in the GPU market, with a market share of 85%. Such dominance has propelled it to become the most valuable company, possessing a massive market capitalization of $5.23 trillion.

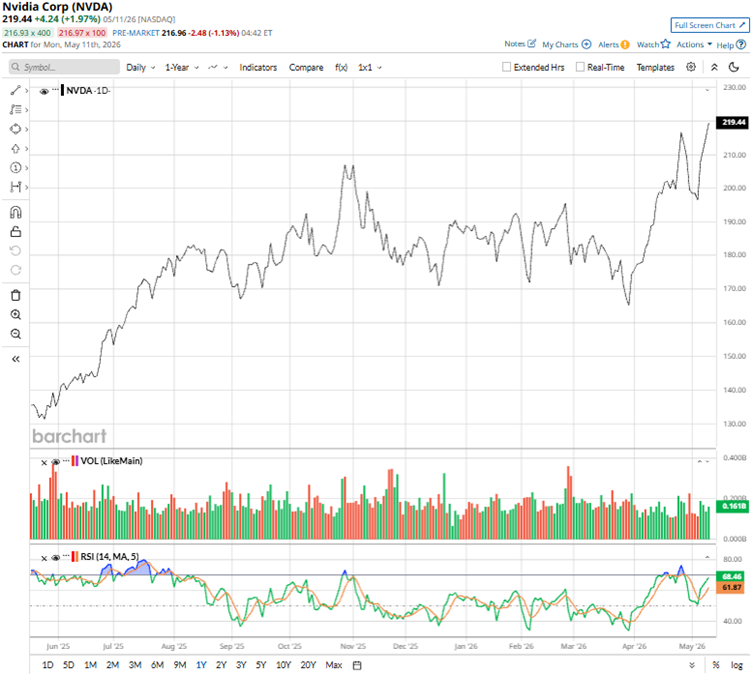

Unrelenting AI demand is still creating tailwinds for Nvidia’s stock. Explosive demand for Nvidia's GPUs, such as the H100 and newer Blackwell chips, powers AI training for hyperscalers, driving a huge surge in data center operations. Over the past 52 weeks, the stock has gained 79.5%, while it has been up 18.38% year-to-date (YTD). Powered by the strong demand for AI infrastructure, NVDA’s stock reached an all-time high of $222.30 on May 11, but is down 0.7% from that level.

Nvidia’s 14-day relative strength index (RSI) of 69.26 indicates that the stock is closer to the overbought territory.

Nvidia Crushed Q4 FY2026 Expectations on AI Chip Frenzy

Nvidia reported record results for the fourth quarter of fiscal 2026 (quarter ended Jan. 25), driven by the growing data center and AI demand. The company’s revenue grew 73% year-over-year (YOY) to a record $68.13 billion, surpassing the $66.21 billion that Wall Street analysts had expected. Of course, the Compute & Networking segment pulled the majority of the weight in the top line, growing 71% YOY to $61.65 billion.

Nvidia’s data center revenue for the quarter climbed 75% from the prior-year period to a record $62.31 billion, ahead of $60.69 billion expectations. Within this business, the networking subsegment (responsible for inter-GPU connections) grew by 263% to $10.98 billion, which shows that its NVLink technology is gaining traction.

Profitability has also been on an uptick. For the fourth quarter, Nvidia’s non-GAAP operating income was $46.11 billion, up 81% YOY. Its non-GAAP EPS grew 82% to $1.62, beating the $1.53 figure that analysts had expected.

Nvidia’s guidance was better than expected. Despite not counting any data center revenue from China, the company expects first-quarter fiscal 2027 revenue (to be reported on May 20, after the market closes) to be $78 billion, plus or minus 2%, which is better than the $72.60 billion anticipated.

Wall Street analysts are robustly optimistic about Nvidia’s future earnings. They expect the company’s EPS to climb by 120.8% YOY to $1.70 for Q1 FY2027. For fiscal 2027, EPS is projected to surge 71.6% annually to $7.84, followed by 34.1% growth to $10.51 in fiscal 2028.

What Analysts Think About Nvidia’s Stock

In addition to the Bernstein analysts’ bullish view, Wall Street has favored Nvidia as the industry darling. Analysts at Benchmark reiterated a bullish “Buy” rating and a $250 price target after the company announced an expanded partnership with Marvell Technology (MRVL). Rosenblatt analysts also kept a “Buy” rating and a $325 price target following the company’s presentation at the GTC-2026 conference, highlighting visibility to more than $1 trillion of orders for Blackwell and Rubin platforms from 2025 through 2027.

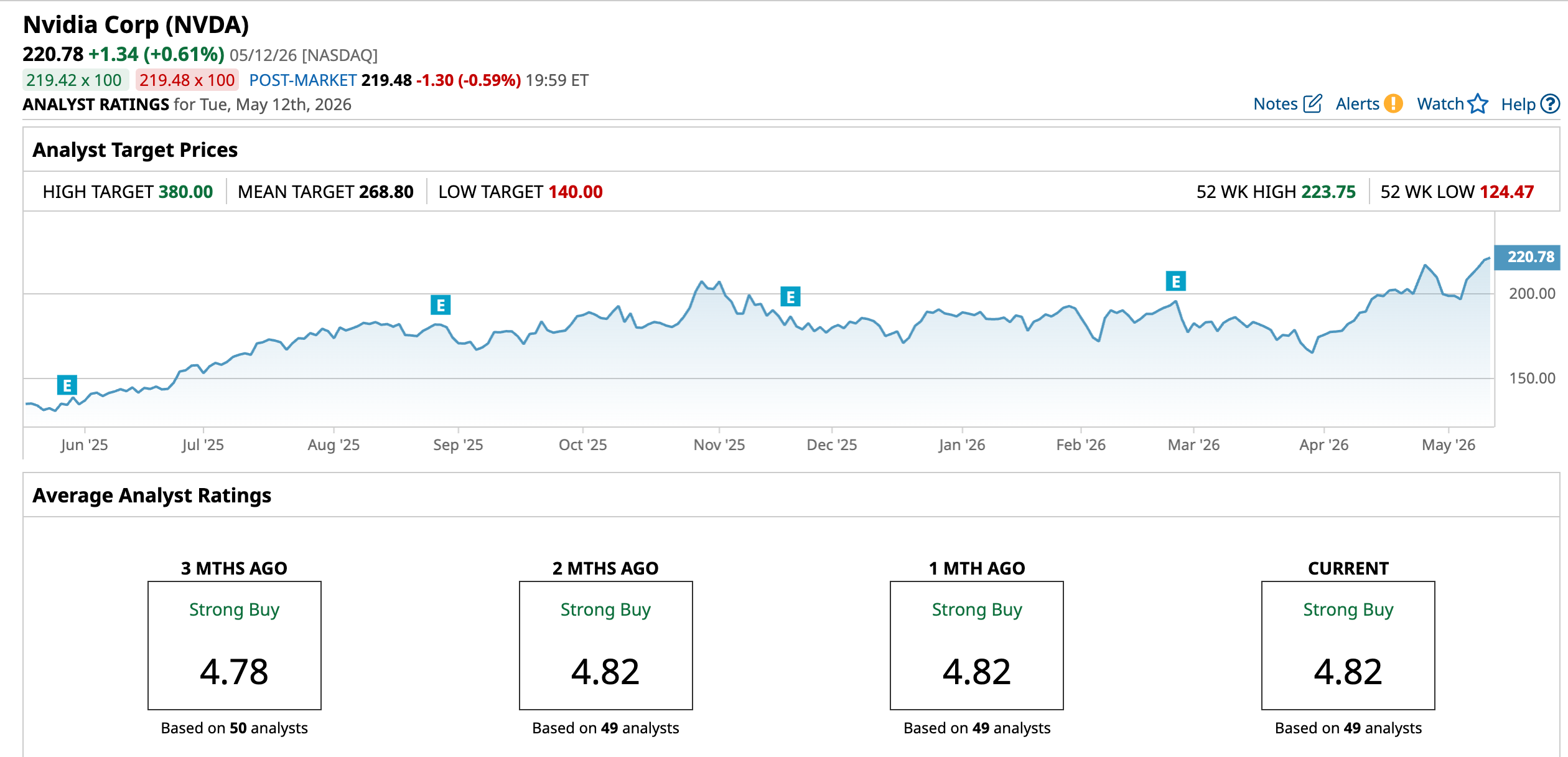

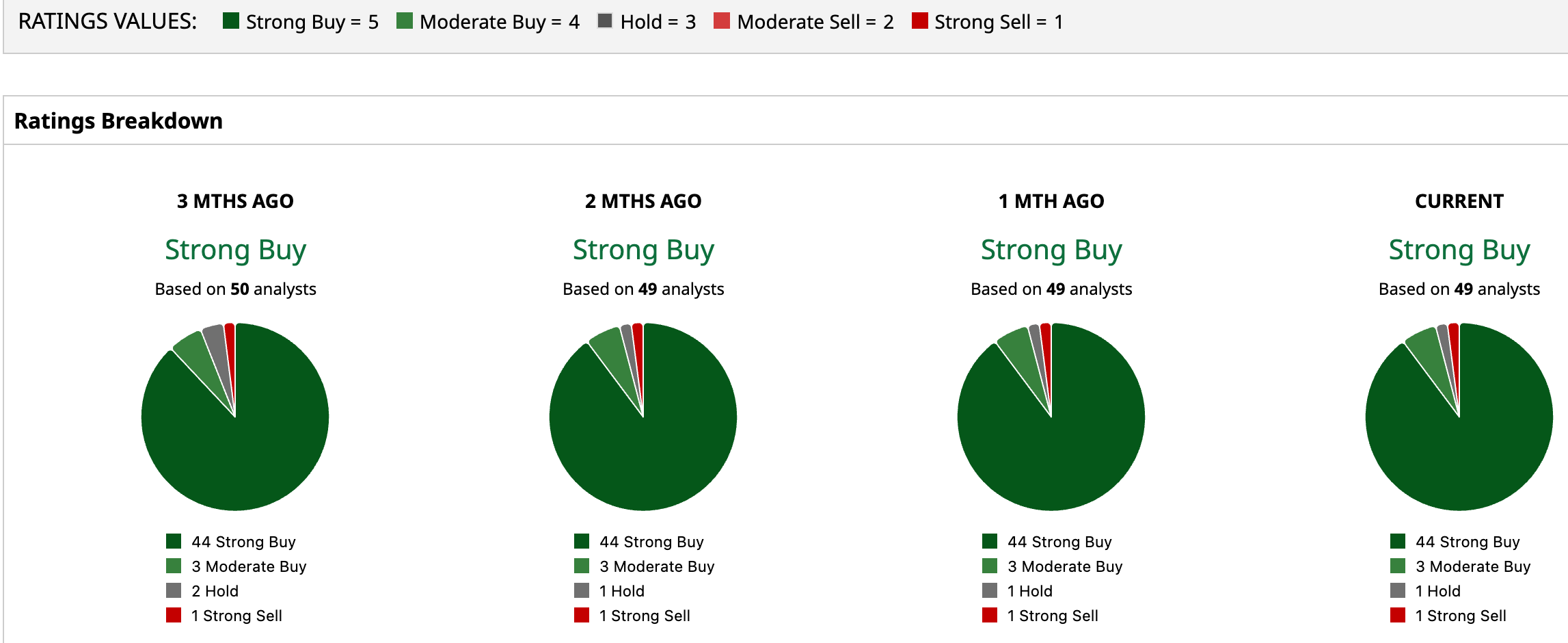

Nvidia has been in the spotlight on Wall Street for some time now, with analysts awarding it a consensus “Strong Buy” rating overall. Of the 49 analysts rating the stock, 44 rate it a “Strong Buy,” three rate it a “Moderate Buy,” one analyst plays it safe with a “Hold,” and only one analyst gives it a “Strong Sell” rating. The consensus price target of $268.80 represents 21.75% upside from current levels. Moreover, the Street-high price target of $380 indicates a 72.12% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)