/Cisco%20Systems%2C%20Inc_%20HQ-by%20Sundry%20Photography%20via%20iStock.jpg)

Artificial intelligence (AI) infrastructure giant Cisco Systems (CSCO) is in focus ahead of its fiscal Q3 earnings set to be released on May 13, after market close.

Consensus is for the company to earn $0.86 a share on at least $15.4 billion in revenue. This would represent a roughly 10% year-over-year increase on both the top- and bottom-line.

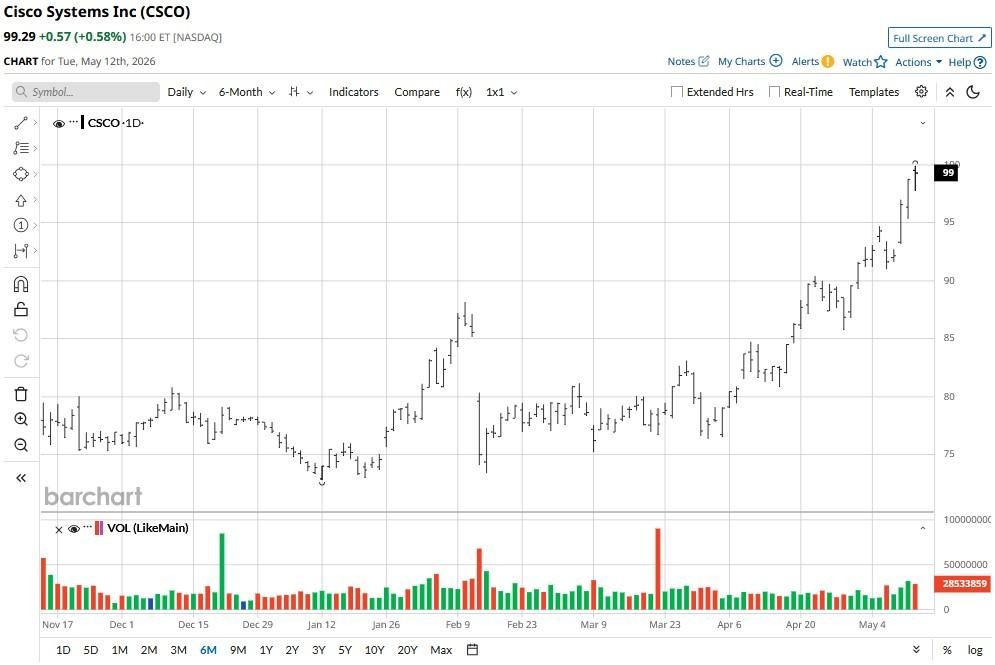

Heading into the quarterly print, Cisco stock is up about 30% versus the start of this year.

Where Options Data Suggests Cisco Stock Is Headed

Despite their year-to-date outperformance, the derivatives market remains convinced that CSCO stock isn’t out of juice just yet.

According to Barchart, options pricing remains skewed to the upside, with the put-to-call ratio on contracts expiring May 15 set at 0.81x currently.

Meanwhile, the upper price on those contracts sits at about $105, indicating Cisco could be trading nearly 7% above present levels by the end of this week.

Investors should also note that the AI infrastructure firm has ripped through its key moving averages (MAs) in recent sessions, indicating bulls are now firmly in control across multiple timeframes.

Strategist Sees Significant Further Upside in CSCO Shares

Freedom Capital’s chief market strategist, Jay Woods, also believes Cisco shares will extend gains after Q3 earnings.

According to him, it’s realistic to expect this legacy tech behemoth to hit as much as $120 over the next quarter, which signals potential upside of more than 20% from here.

A healthy 1.7% dividend yield makes the AI stock even more attractive as a long-term holding in 2026, Woods added.

Based on 13 distinct short-, medium-, and long-term technical indicators, Barchart also currently has a “100% BUY” opinion on San Jose-headquartered Cisco Systems.

How Wall Street Recommends Playing Cisco Systems

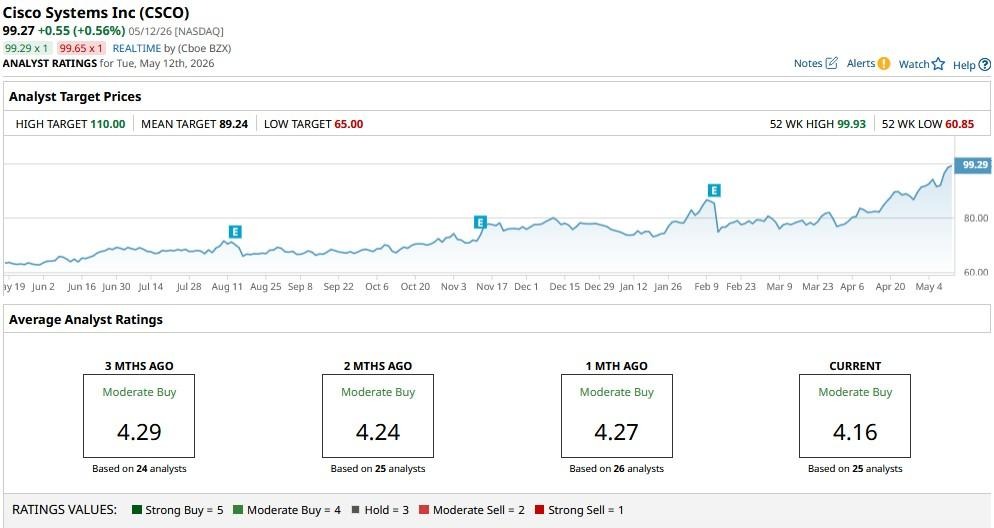

Investors could also take heart in the fact that Wall Street remains bullish on CSCO shares heading into the company’s Q3 earnings on May 13.

According to Barchart, the consensus rating on Cisco Systems sits at “Moderate Buy” currently, with price targets as high as $110, indicating potential upside of another 10% from here.

At the time of writing, Cisco is going for less than 7x sales, which makes it significantly cheaper to own than a bunch of its AI peers.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)