The hydrogen fuel cell company walked into its Q1 FY2026 earnings on Monday, May 11, handing skeptics a reality check they weren't quite ready for. Plug Power (PLUG) beat analyst expectations and put a dramatic improvement in gross margins front and center, signaling that years of uphill climbing might finally be paying off.

GAAP gross margin improved to -13% from -55% in the prior year’s period, reflecting a 71% overall margin improvement and a 42-percentage point year-over-year (YOY) expansion in margin rate.

Management pointed to three engines which drove the lift. First, sales growth spread operating leverage across the platform. Secondly, the service business tightened up with quarterly per unit costs falling 30% YOY, thanks to improved stack reliability and continued pricing actions. And third, fuel margin rate improved by approximately 54 percentage points.

The shareholder base, which weathered years of mounting losses and repeated cash burn warnings, quickly caught the optimism bug. The stock surged 12.8% on the day of announcement in direct response to the results.

The company has not crossed the profitability finish line yet, but the margin expansion makes a compelling case that cost reduction initiatives and manufacturing efficiencies are finding their footing at last.

In fact, CEO Andy Marsh stands behind the company's path, pointing to reduced liquefied hydrogen purchase costs and improved electrolyzer pricing as the primary levers toward a sustained positive gross margin.

About Plug Power Stock

The Slingerlands, New York-based Plug Power builds and operates hydrogen fuel cell systems, electrolyzers, and cryogenic infrastructure that powers forklifts, automated vehicles, fleet operations, and backup energy networks. The company holds a market cap of $4.9 billion and carries the distinction of creating the first commercially viable market for hydrogen fuel cell technology.

Plug Power has deployed more than 74,000 fuel cell systems and over 280 fueling stations, putting it ahead of every competitor in the world, while also holding the title of the largest buyer of liquid hydrogen on the planet.

The stock has rewarded believers handsomely on every timeframe worth measuring. Plug Power’s shares have gained 293.98% over the last 52 weeks and sits 80.7% higher year-to-date (YTD). Moreover, the stock has skyrocketed 29.93% in just the last one month, tacking on another 7.23% over the last five trading sessions alone.

On the valuation front, PLUG stock is currently trading at 6.13 times forward sales. The figure sits at a premium compared to the industry average but looks like a bargain when stacked against its own five-year historical multiple.

Plug Power Surpasses Q1 Earnings

Plug Power put its Q1 FY2026 numbers on the table on May 11. During the quarter, net revenue grew 22.3% YOY to $163.5 million, topping Street forecasts of $142.5 million. Non-GAAP loss per share narrowed 52.9% YOY to $0.08, beating Wall Street expectations of a loss per share of $0.09.

The hydrogen segment proved it could carry weight on its own terms. Fuel sales rose 22% YOY, driven by customer growth, increasing prices, and reduced customer warrant charges. The electrolyzer platform took things a step further, posting a 343% revenue increase YOY to $9.2 million.

The broader loss picture followed suit across every line, with gross loss narrowing 70.7% from the year ago figure to $21.6 million, operating loss pulling back 38.6% to $109.5 million, and non-GAAP net loss attributable to Plug Power tightening 35.4% YOY to $105.5 million.

On the liquidity front, Plug Power closed the quarter with $223 million in unrestricted cash and $579 million in restricted cash, stacking up to a total of $802 million.

With the numbers doing the talking, Plug Power ditched the vague "eventually profitable" language and replaced it with something the market could actually hold management to. The company targets positive EBITDA by Q4 2026, a specific near-term milestone with real teeth.

On the other hand, analysts see the trajectory continuing, projecting FY2026 loss per share to narrow 51.6% YOY to $0.30, and for fiscal year 2027, estimates point to loss per share tightening another 40% YOY to $0.18.

What Do Analysts Expect for Plug Power Stock?

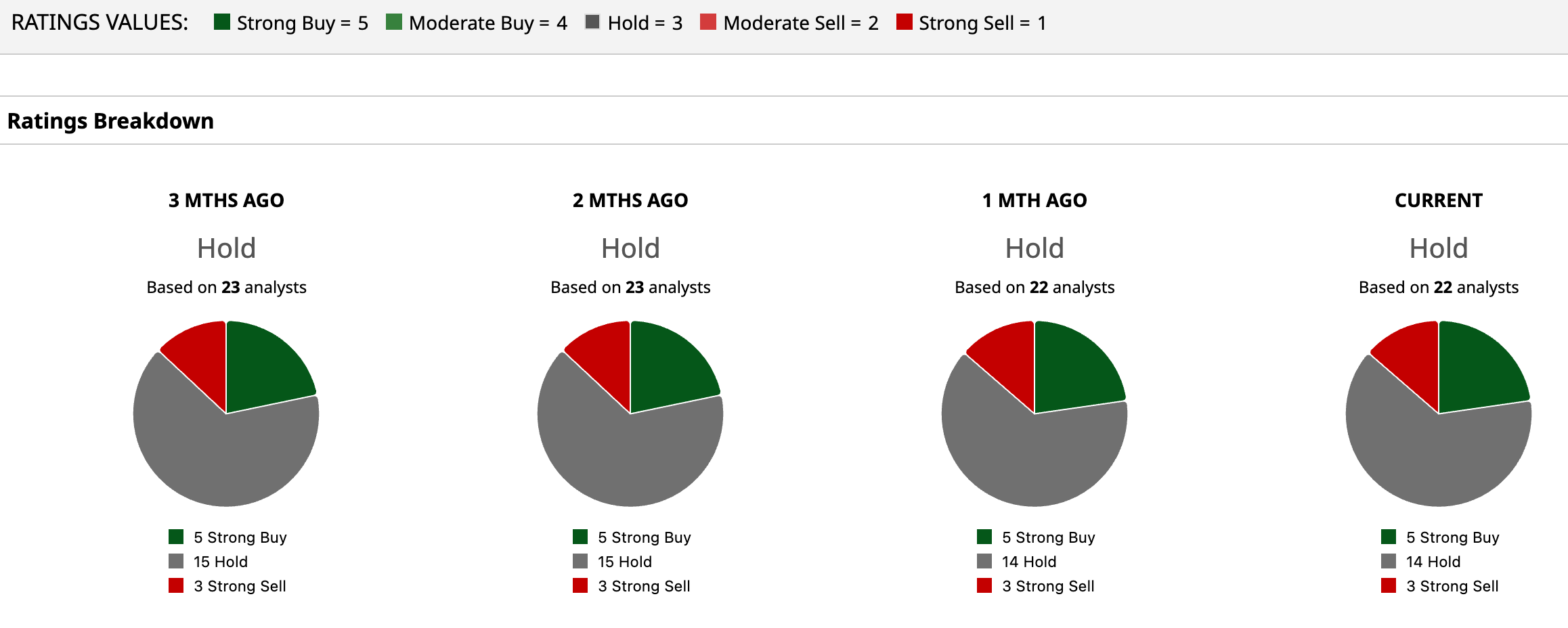

The financial improvement story carries genuine weight, but the current loss backdrop keeps the broader analyst community anchored at an overall "Hold" rating on the stock. Among 22 analysts covering the stock, five issue a "Strong Buy" rating, 14 have settled into a "Moderate Buy" stance, while three analysts hold their ground with a "Strong Sell."

The stock already trades above its average price target of $2.82. Meanwhile, the Street-High target of $7 keeps a compelling upside case of 95% on the table for investors willing to play on the turnaround running its full course.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)