Digital freelance hiring marketplace, Upwork (UPWK), just handed pink slips to roughly 24% of its total workforce, with affected employees set to receive notifications as early as this week. The announcement marks one of the more dramatic restructurings the gig economy space has ever witnessed, but one specific line buried inside the CEO's letter caught the tech world's attention.

CEO Hayden Brown declared publicly that "two pizza teams" are dead. Jeff Bezos originally coined the phrase at Amazon.com (AMZN) to describe a team small enough to share two pizzas, typically six to ten people, and for decades, the idea served as the golden rule of lean, agile organizations everywhere.

Upwork's CEO has now nailed the coffin shut on it, arguing that artificial intelligence (AI) has fundamentally collapsed the need for small, coordinated teams altogether. One person armed with the right AI tools can now carry the workload that once kept several people productively occupied.

The restructuring, announced on Thursday, May 7, is specifically designed to build a leaner operating model. Upwork expects the plan to wrap up substantially by the Q4 FY2026, with pre-tax restructuring charges landing somewhere between $16 million and $23 million on its GAAP financials.

The bulk of these costs, primarily severance and one-time termination payouts, will hit in Q2 FY2026, with the remainder spreading across the following two to three quarters.

The deeper irony practically writes itself on the wall, because Upwork, a platform that built its entire identity on the promise of human freelance talent, is now restructuring away from that very human labor in direct response to AI. With this backdrop in place, let us take a hard look at the possible future destiny of this stock.

About Upwork Stock

Based in Palo Alto, California, Upwork runs a digital hiring marketplace where enterprises and startups source freelance developers, designers, marketers, customer support specialists, and AI experts.

The roughly $1.1 billion market cap company goes well beyond simple matchmaking and handles onboarding, compliance, payroll, invoicing, contract management, escrow protection, and collaboration workflows, while its enterprise and managed services division takes the wheel on outsourced projects and contingent workforce operations.

However, UPWK stock has had a brutal ride through the market lately. Over the last 52 weeks, it plunged 52.16%, and year-to-date (YTD), the bleeding cuts even deeper at 58%. The past five trading sessions alone carved out a 19.25% decline on the heels of the restructuring announcement and a mixed earnings report.

On the valuation front, UPWK stock currently trades at 5.73 times forward adjusted earnings and 1.38 times sales. Both numbers look like a bargain when stacked against the industry averages and the stock's own five-year historical multiples.

A Closer Look at Upwork’s Q1 Earnings

Upwork dropped its Q1 FY2026 financial results on May 7, and the very next day, May 8, the stock plunged 16.9% as the market digested a mixed earnings report, weak forward guidance, and restructuring news.

Revenue grew 1.4% year-over-year (YOY) to $195.5 million, landing in line with analyst estimates of $195.9 million. Non-GAAP EPS climbed 2.9% YOY to $0.35, comfortably beating analyst estimates of $0.27 in the process.

With restructuring in the room, it would be remiss to not to talk about AI's fingerprints on the business. The company felt AI's impact from two very distinct angles during the quarter. On the low end, simple tasks are getting swallowed up by AI tools and quietly disappearing from the platform.

On the flip side, gross services value (GSV) from AI-related work surpassed $300 million on an annualized basis and grew more than 40% YOY during the quarter, which shows that the AI wave is lifting some boats even while sinking others.

Traction with small and medium-sized businesses (SMBs) and enterprises told a strong story as well. The Business Plus plan emerged as the fastest-growing product in the company's entire history, posting 34% quarter-over-quarter growth as Upwork pushes deeper into the $530 billion SMB market.

Over at the Lifted subsidiary, the enterprise pipeline grew 3x for new clients and 9x for existing clients during the quarter. Upwork also kept pouring investment into Uma, its AI work agent, to keep expanding the SMB AI value proposition.

For Q2 FY2026, Upwork’s management expects revenue to come in between $187 million and $193 million, with adjusted EBITDA sitting between $56 million and $59 million, which translates to an adjusted EBITDA margin of 30% to 31%. The company also expects Q2 non-GAAP diluted EPS to land between $0.35 and $0.37.

With geopolitical uncertainty still swirling and persistent softness among the lowest value contracts making things uncomfortable, Upwork has trimmed its full-year FY2026 revenue guidance to reflect those ongoing trends.

For the full year FY2026, the company projects revenue between $760 million and $790 million, adjusted EBITDA of $250 million to $260 million, representing a 33% adjusted EBITDA margin, and non-GAAP diluted EPS between $1.50 and $1.55.

Looking ahead, analysts peg Q2 FY2026 EPS growth at 33.3% YOY, arriving at $0.32. For the full year FY2026, EPS carries an estimated 66.7% growth from the prior year to reach $1.40, and in the following fiscal year, the bottom line could climb as much as 17.9% YOY to hit $1.65.

What Do Analysts Expect for Upwork Stock?

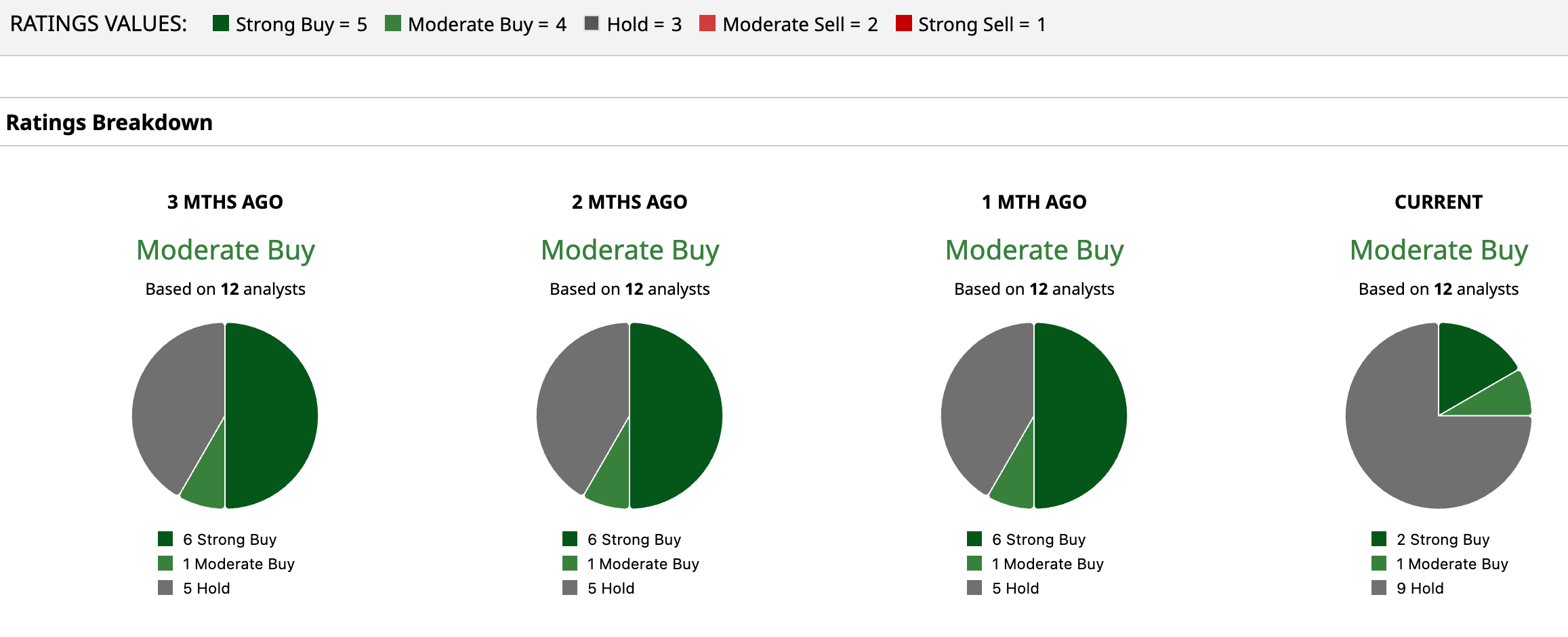

The broader analyst community has kept its head above the noise and assigned UPWK stock an overall rating of "Moderate Buy" despite the volatile fundamental backdrop. Among 12 analysts covering the stock, two analysts have issued a "Strong Buy" rating, one hands it a "Moderate Buy," and nine park themselves on the fence with a "Hold."

The average price target of $15.90 already bakes in potential upside of 90.4%. Meanwhile, the Street-High target of $27 sweetens the pot even further as it suggests a gain of 223.4% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)