/AI%20(artificial%20intelligence)/Artificial%20Intelligence%20technology%20concept%20by%20NicoEINino%20via%20Shutterstock.jpg)

AI‑infrastructure stocks have been the market’s adrenaline shot for more than a year now. Yet the ground is shifting. Investors have rotated from “buy the narrative” to “show me the cash flow.” Pure‑play AI cloud builders, companies that don’t just rent GPUs but own the concrete, steel, and fiber, are suddenly the act that everyone wants to see.

Into this glare steps Nebius Group (NBIS), the Amsterdam‑based full‑stack AI cloud operator, which has rapidly rebuilt itself after sanctions-related disruption and grown into a $45 billion AI infrastructure player that few investors expected.

So now, on Wednesday, May 13, before the opening bell, it reports first‑quarter 2026 numbers. For anyone holding shares or just watching the AI trade, that date is now circled in red.

How Did Nebius Stock Perform?

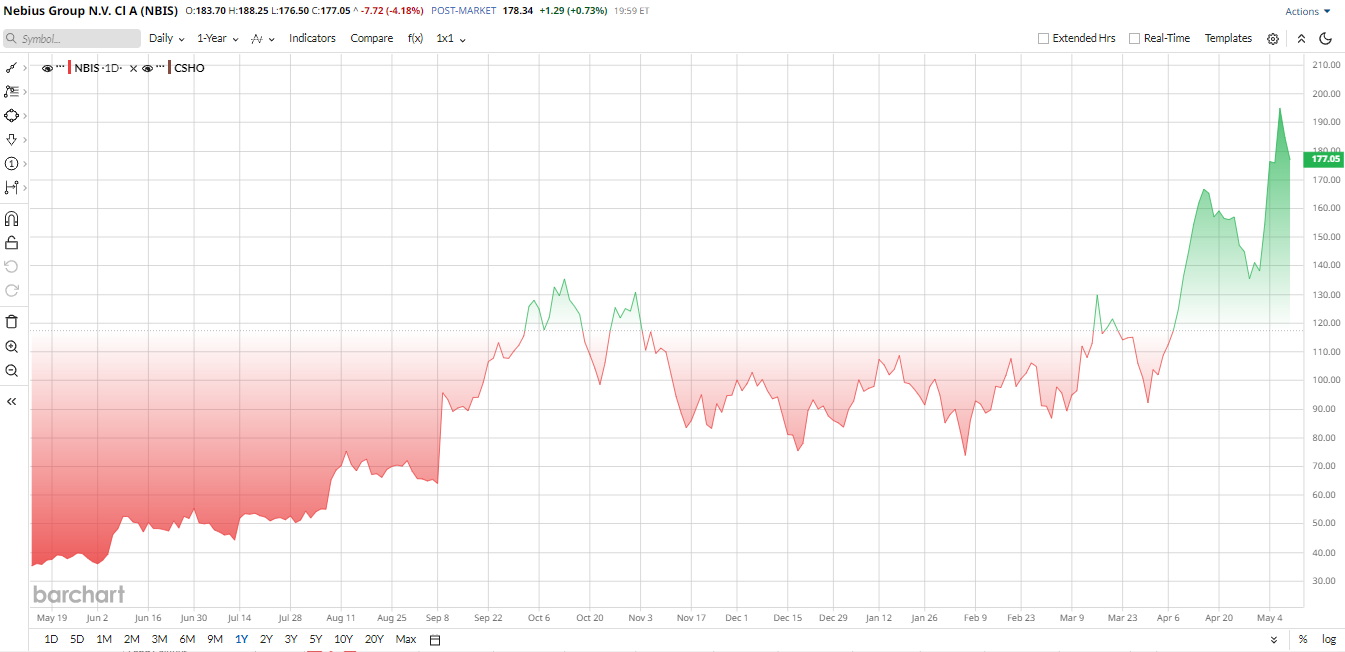

Nebius shares have been on the tear. It surged by about 111% year-to-date and more than 527% over the past 12 months, making it one of the biggest winners in the AI infrastructure trade. The rally has been driven by major contract wins, expanding demand for AI cloud capacity, and growing investor confidence that Nebius is becoming a serious long-term player in the space.

Among the biggest catalysts was Nebius’ landmark contract with Meta (META), which helped cement the company’s place among the more serious players in AI cloud infrastructure. The company also gained attention after announcing a strategic tie-up with Nvidia (NVDA), a move that many investors viewed as a strong validation of Nebius’ position in the market.

More recently, Nebius said it would acquire Eigen AI, a small but specialized inference-optimization company, for about $643 million. That deal matters because it fits neatly into Nebius’ higher-margin Token Factory platform, which is designed to serve production workloads rather than simply offer raw compute.

What to Expect From the Upcoming Report

All of that now leads to May 13, when Nebius is scheduled to report first-quarter 2026 results before the opening bell. This is the first major earnings test since the market began pricing the company more like a scaled AI infrastructure winner than a speculative growth story.

Wall Street is expecting revenue in the high $300 million range for the quarter, with losses ($0.81) still likely as the company continues to spend heavily on expansion. That is not unusual for a business at this stage, but it does mean the bar is high. A strong print could reinforce the idea that Nebius is becoming an execution story.

A miss, or any sign that capacity constraints are slowing growth, could quickly cool the enthusiasm.

The company’s fourth-quarter 2025 report reminded investors that this name can move sharply in either direction. Nebius missed both earnings and revenue expectations in that report, which triggered a selloff. That is why this next update matters so much: Investors are no longer willing to buy the story alone.

Valuation Still Looks Stretched

Even after all the progress, Nebius is not a cheap stock. On traditional measures, the valuation remains demanding. The EV/sales stands at 88, significantly higher than the sector median of 4, indicating a very expensive stock. Similarly, the price-to-book ratio is 9x compared to the sector's 4x, suggesting overvaluation.

That does not automatically make the stock unattractive. Bulls argue that old-school valuation metrics do not tell the full story when revenue is compounding rapidly, and capacity remains constrained across the AI ecosystem. If Nebius continues to scale and keeps locking in long-duration contracts, the current valuation could look less extreme in hindsight.

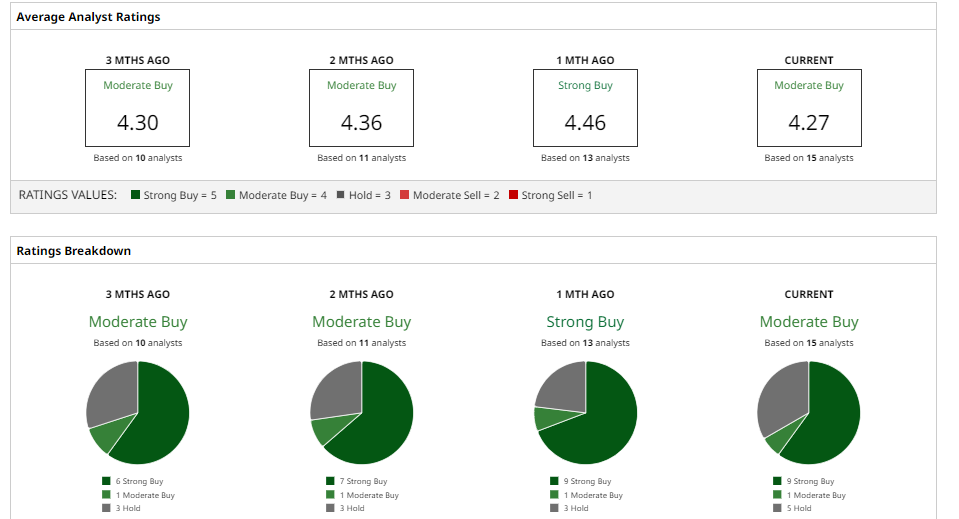

Analyst Opinions on NBIS Stock

Wall Street remains constructive overall, but not unanimously so. Goldman Sachs wasted no time after the Meta deal. It hiked its NBIS price target to $205, raised 2027‑2030 revenue estimates by 30‑54%, and kept its “Buy” rating, declaring the stock “a structural winner.”

Morgan Stanley’s Josh Baer is more guarded; he initiated on Jan 15 with an “Equal‑Weight” and a $126 target, emphasizing that “long‑term metrics, not near‑term earnings, should drive valuation.”

Wolfe Research split the difference with a “Neutral” and a fair‑value range of $80 to $170, calling the demand story compelling but warning that “execution and financing risk remain material.”

The consensus on Wall Street is “Moderate Buy.” The average 12‑month price target sits at $172.5, which the current stock price already surpassed; however, its street high is $291, which is floating around. $215 implies at least 21% upside potential.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)