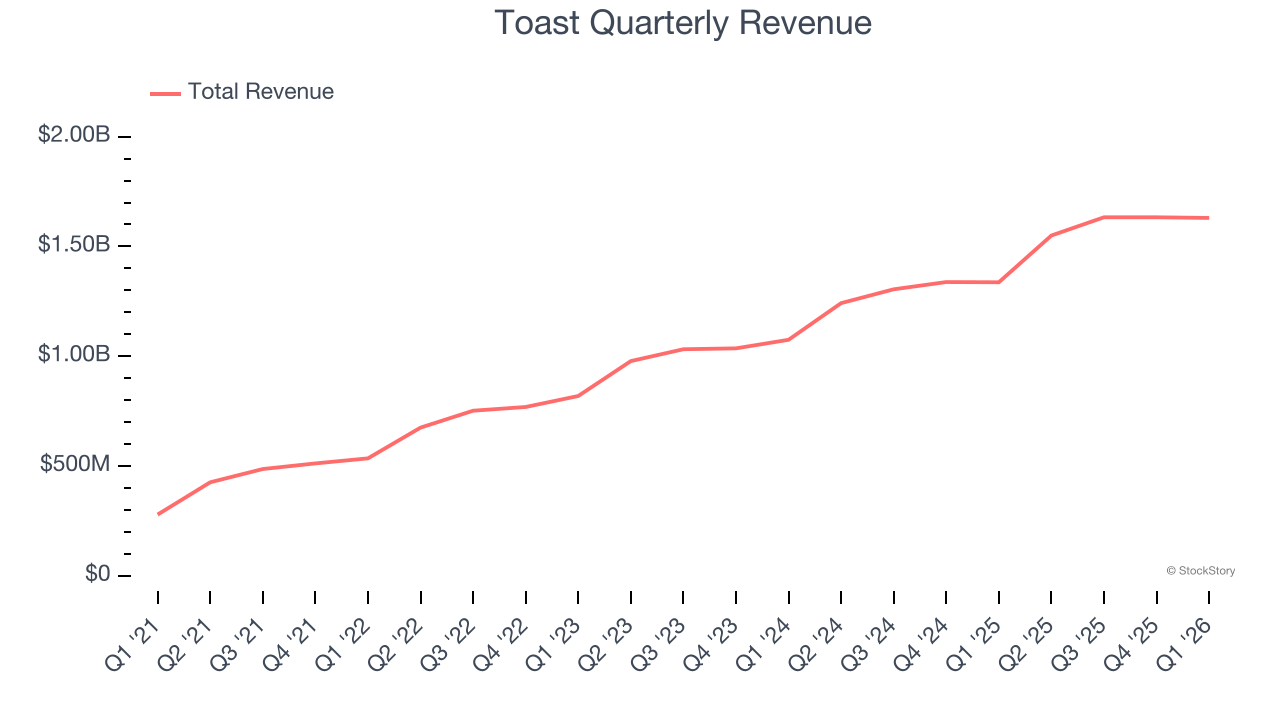

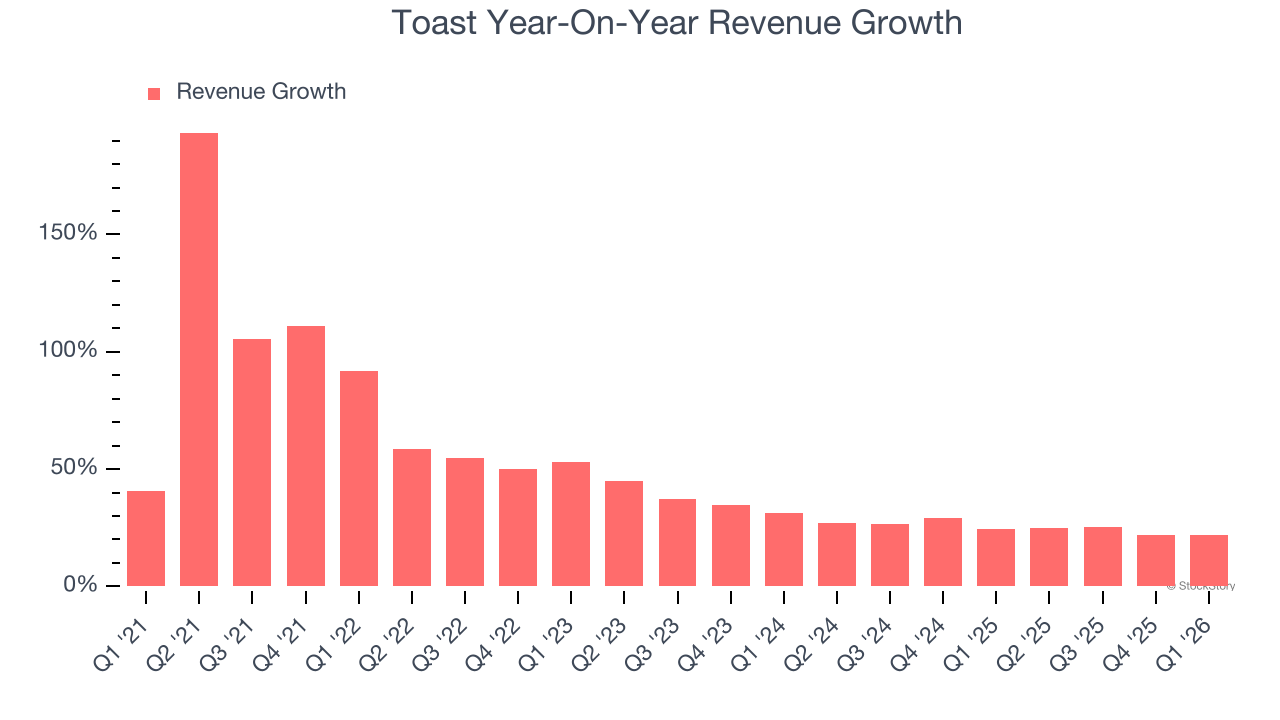

Restaurant technology platform Toast (NYSE:TOST) met Wall Street’s revenue expectations in Q1 CY2026, with sales up 21.9% year on year to $1.63 billion. Its GAAP profit of $0.20 per share was 28.6% above analysts’ consensus estimates.

Is now the time to buy Toast? Find out by accessing our full research report, it’s free.

Toast (TOST) Q1 CY2026 Highlights:

- Revenue: $1.63 billion vs analyst estimates of $1.63 billion (21.9% year-on-year growth, in line)

- EPS (GAAP): $0.20 vs analyst estimates of $0.16 (28.6% beat)

- Adjusted Operating Income: $164 million vs analyst estimates of $158.5 million (10.1% margin, 3.5% beat)

- EBITDA guidance for the full year is $800 million at the midpoint, above analyst estimates of $793.6 million

- Operating Margin: 6.7%, up from 3.2% in the same quarter last year

- Free Cash Flow Margin: 7.1%, down from 10.9% in the previous quarter

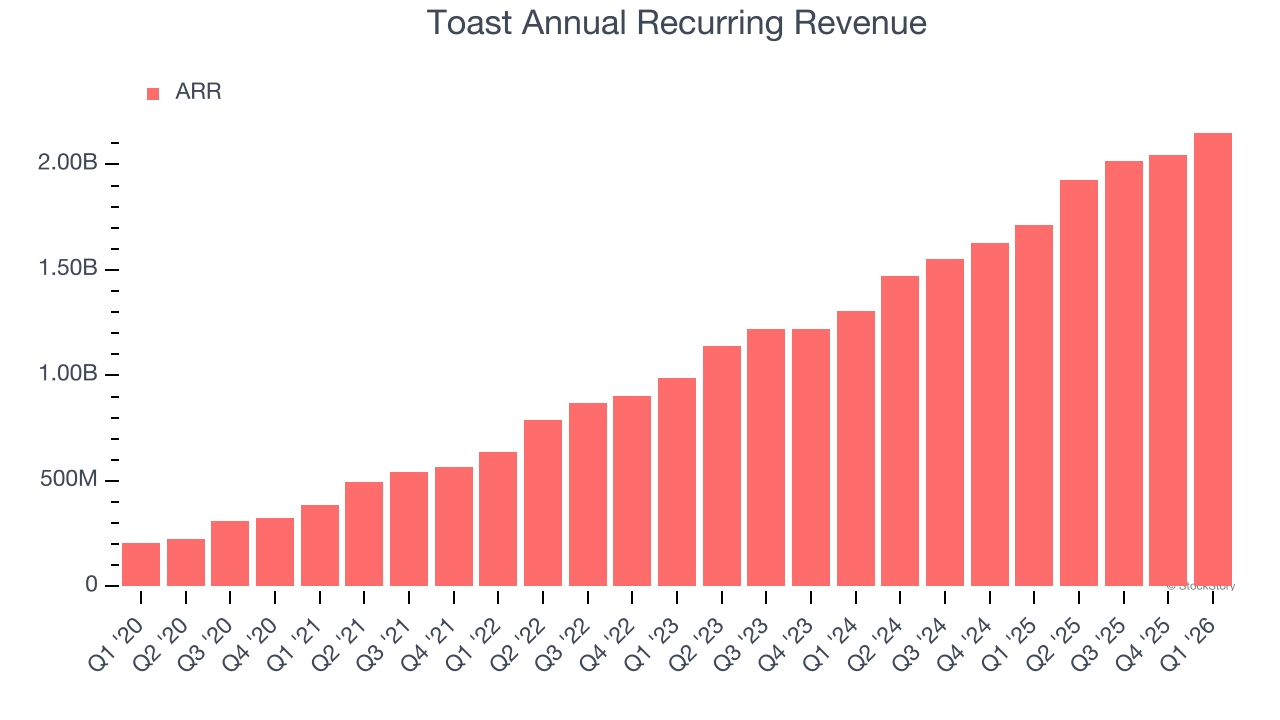

- Annual Recurring Revenue: $2.15 billion vs analyst estimates of $2.15 billion (25.6% year-on-year growth, in line)

- Billings: $1.63 billion at quarter end, up 22.3% year on year

- Market Capitalization: $16.41 billion

Company Overview

Born from the frustrations of three friends waiting too long for their restaurant bill, Toast (NYSE:TOST) provides a cloud-based digital technology platform with software, payment processing, and hardware solutions built specifically for restaurants.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Toast’s 48.1% annualized revenue growth over the last five years was incredible. Its growth beat the average software company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Toast’s annualized revenue growth of 25.1% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Toast’s year-on-year revenue growth of 21.9% was excellent, and its $1.63 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 20.1% over the next 12 months, a deceleration versus the last two years. Still, this projection is commendable and indicates the market sees success for its products and services.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Toast’s ARR punched in at $2.15 billion in Q1, and over the last four quarters, its growth was fantastic as it averaged 28% year-on-year increases. This alternate topline metric grew faster than total sales, which likely means that the recurring portions of the business are growing faster than less predictable, choppier ones such as implementation fees. That could be a good sign for future revenue growth.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Toast’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a competitive market and must continue investing to grow.

Key Takeaways from Toast’s Q1 Results

We enjoyed seeing Toast beat analysts’ EBITDA expectations this quarter. We were also glad its full-year EBITDA guidance slightly exceeded Wall Street’s estimates. On the other hand, its EBITDA guidance for next quarter missed. Zooming out, we think this was a mixed quarter. The market seemed to be hoping for more, and the stock traded down 10.5% to $26.35 immediately following the results.

So should you invest in Toast right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

/Intel%20Corp_%20badge%20holder-by%20hasrul_rais%20via%20Shutterstock.jpg)

/Advanced%20Micro%20Devices%20Inc_%20logo%20on%20phone%20and%20website-by%20T_Schneider%20via%20Shutterstock.jpg)

/The%20Shopify%20logo%20on%20a%20smartphone%20screen%20by%20IB%20Photography%20%20via%20Shutterstock.jpg)

/Robinhood%20app%20on%20phone%20by%20Andrew%20Neel%20via%20Unsplash.jpg)