/AI%20(artificial%20intelligence)/Image%20of%20server%20racks%20in%20modern%20server%20room%20data%20center%20by%20Sashkin%20via%20Shutterstock.jpg)

For months, investors have worried that AI could eat into enterprise software names, especially the ones tied to developer workflows and collaboration tools. That fear helped punish a lot of software stocks.

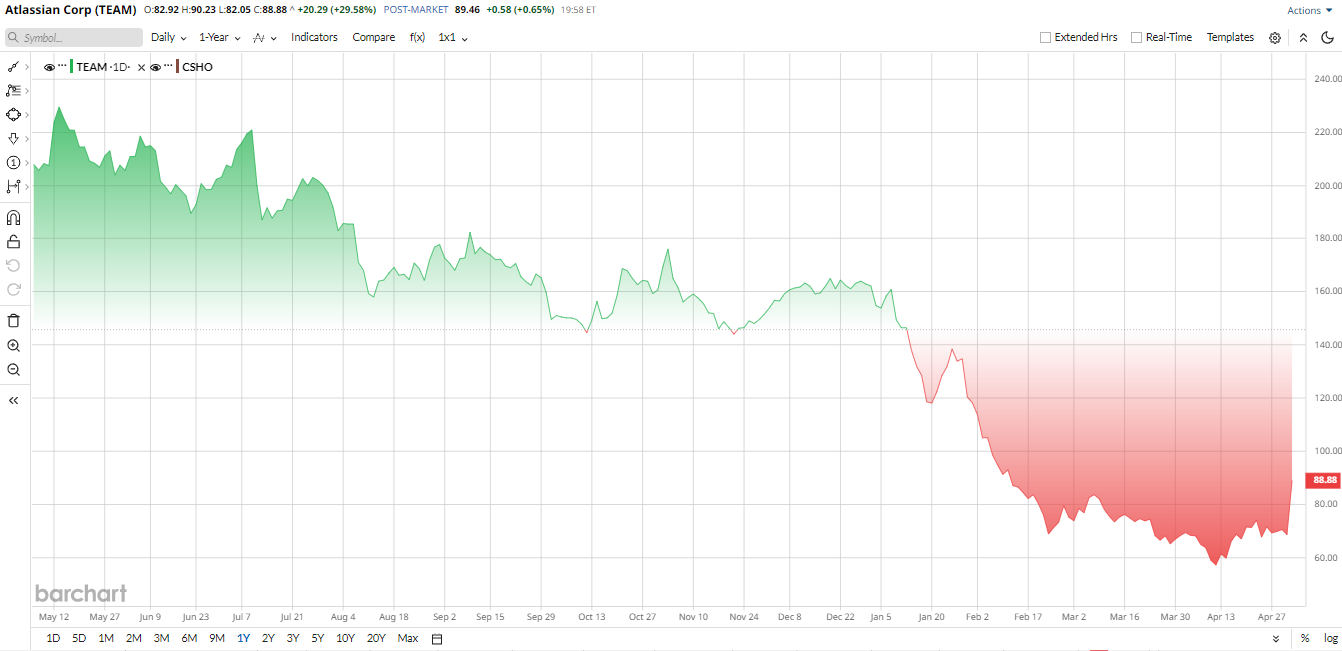

Atlassian (TEAM) was no exception. But the company just posted a quarter that made the doomsday trade look a lot less convincing. Shares jumped nearly 30% after the report as investors focused on stronger-than-expected demand, a big cloud beat, and data-center revenue that surged 44% year-over-year (YOY).

The story is simple. Atlassian still faces pressure from rising spending and a noisy debate about how fast it can turn AI into real growth. But the latest quarter shows a business that is still growing fast and still has plenty of customers willing to pay.

About Atlassian Stock

Atlassian builds software that helps teams plan work, track projects, and ship products. Jira and Confluence are its best-known tools. The company is not flashy, but it is deeply embedded into how many businesses run.

Over the past year, TEAM stock has been wild. Shares were previously down more than 60% when investors worried AI would weaken software demand, and when capex and investment plans looked heavy. That slump pushed the stock well below its highs. But in mid-2026, TEAM stock began fighting back and has climbed 35% over the past month. The rebound has been driven by better execution, stronger cloud growth, and proof that the company still has pricing power.

That earlier dip in shares made sense. Investors like growth, but they do not love big spending when the payoff is uncertain. Atlassian has been investing in AI, product expansion, and cloud infrastructure. That can weigh on sentiment even when the business itself is still healthy.

On valuation, Atlassian does not look cheap, but it also doesn't look absurdly expensive for a software name with this kind of growth. The stock trades at about 16.7 times forward earnings and 4.4 times sales. That is around the middle of the software pack — not a bargain basement number, but not bubble territory, either.

Atlassian Reports Earnings

The latest quarter changed the tone. Investors had been bracing for another disappointing software print, but Atlassian delivered a double-beat performance.

Total revenue in the March quarter rose 32% YOY to $1.79 billion. Data-center revenue was the standout, jumping 44% as customers kept spending even on older deployment models. That mattered because data center had been one of the biggest question marks around TEAM stock. Instead of fading quickly, it turned into proof that customers are still locked into the platform and willing to pay.

Atlassian also delivered solid profitability. Net income came in at $456.5 million, up from $261.5 million a year earlier.

Free cash flow came to $561.3 million. Atlassian ended the quarter with roughly $1.1 billion in cash and cash equivalents. Those are strong numbers for a company that is still investing aggressively in AI and enterprise growth.

CEO Mike Cannon-Brookes said the quarter showed the power of the company’s strategy, pointing to bigger customer commitments and stronger traction in Service Collection. That is exactly what investors wanted to hear, suggesting that the growth is not just a one-quarter spike but driven by larger deals and deeper product adoption.

Guidance helped, too. Atlassian raised its full-year revenue growth outlook to about 24%. Analysts are looking for roughly $6.47 billion in full-year revenue and adjusted earnings of about $5.50 per share, so the company looks well-positioned against Street expectations.

Atlassian Doubles Down on AI Growth

Atlassian is now starting to show that AI may be a growth engine, not a threat. The company has been building AI tools like Rovo, its workplace assistant, while adding AI features across Jira and Confluence. Atlassian’s cloud and data-center growth also suggests that AI is helping customers work faster, automate tasks, and keep spending inside its software ecosystem.

The company is remaining active on the product front in 2026. Atlassian recently expanded its partnership with Alphabet's (GOOGL) Google Cloud to push deeper into agentic AI, including support for Gemini 3 Flash in Rovo. It is also building out enterprise tools and AI features.

In September 2025, Atlassian agreed to buy DX for about $1 billion to improve how customers measure AI investment and developer productivity. That is a smart move that will give the firm more data and more insight — and give customers more reasons to stay inside its ecosystem.

What Do Analysts Think of TEAM Stock?

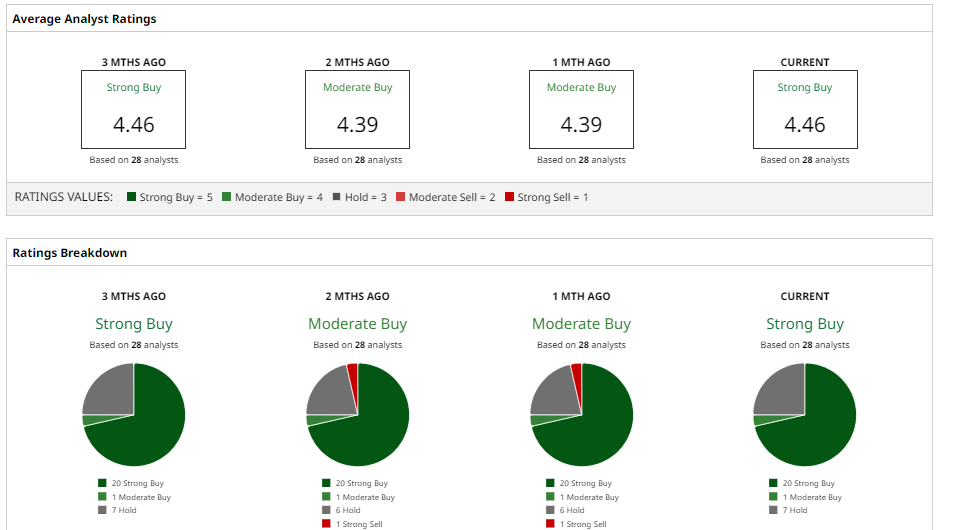

Wall Street analysts are highly optimistic about the TEAM stock rebound story. Morgan Stanley recently kept its “Overweight” rating and $120 price target on shares. Piper Sandler trimmed its target to $175 from $200 but still sees meaningful upside.

However, Goldman Sachs remains more cautious, keeping a neutral view as it watches spending and margin pressure. Barclays has also taken a more measured stance, even as the stock has recovered, offering an “Overweight” rating alongside a $106 price target.

Overall, analysts have a consensus “Strong Buy” rating on TEAM stock with an average price target of $126.04. That suggests potential upside of 36% from current levels.

For investors, the takeaway is simple. The software apocalypse story looks overdone, at least for now. Atlassian is still growing, winning enterprise customers, and proving that AI may help software companies sell more, not less.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)