/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

Alphabet (GOOG) (GOOGL) delivered a robust first-quarter performance led by solid AI-driven momentum across its core businesses, including Search, YouTube, and Cloud. Market reaction was positive, with shares rising in pre-market trading following the earnings release. This response reflects growing investor confidence that Alphabet’s AI investments are translating into measurable financial outcomes. In particular, improvements in ad targeting efficiency, user engagement, and enterprise cloud adoption indicate that AI integration is enhancing both monetization and competitive positioning.

Looking ahead, Alphabet appears well-positioned to sustain its solid growth trajectory. Google’s growing AI capabilities are leading to record revenue and backlog growth in Google Cloud. This indicates that Alphabet stock could hit new highs in the future.

AI Powering Alphabet’s Strong Growth

Alphabet’s aggressive push into AI is translating into solid financial performance. The tech giant’s first-quarter performance reflects that the integration of AI across its ecosystem is powering growth in its core businesses while opening new revenue streams.

In the first quarter, Alphabet extended its streak to 11 consecutive quarters of double-digit revenue growth, with total revenue climbing 22% year-over-year (YoY) to $109.9 billion. A bulk of this revenue is from the Google Services division, which generated $90 billion during the quarter, up 16% YoY.

Within Google Services, Search continues to deliver steady growth, contributing $60 billion in revenue. AI is enhancing user engagement and improving monetization efficiency. Google’s ongoing investment in AI-powered search features, such as AI-generated overviews, suggests the momentum will likely continue.

The company’s advertising business is also benefiting from AI advancements. YouTube saw ad revenue rise 11%. Notably, Alphabet is embedding its Gemini models into its advertising infrastructure to optimize targeting, creative delivery, and campaign performance. This integration is improving returns for advertisers while strengthening Alphabet’s pricing power.

Google Cloud delivered exceptional performance, marked by an acceleration in top-line growth. The segment delivered $20 billion in revenue, marking a 63% YoY increase. Growth was broad-based but particularly strong in Google Cloud Platform (GCP), which continues to outpace the overall cloud segment. AI workloads are emerging as the primary growth catalyst, with demand concentrated around advanced models such as Gemini and associated enterprise solutions.

Infrastructure expansion also played a key role. Increased deployment of TPUs and GPUs is supporting both internal AI development and external customer demand. Meanwhile, core GCP services, including cybersecurity and data analytics, remain key contributors, reflecting enterprise customers’ broader digital transformation efforts. Workspace continued its steady growth trajectory, benefiting from both seat expansion and higher average revenue per user.

Profitability within the cloud segment improved significantly, signaling operating leverage at scale. Operating income reached $6.6 billion, tripling YoY, while margins expanded from 17.8% to 32.9%. This margin profile indicates that prior heavy investments in infrastructure and AI capabilities are beginning to yield returns.

Looking ahead, the company’s cloud backlog nearly doubled to $462 billion, offering strong visibility into future growth. Management expects more than half of this to convert into revenue over the next two years.

Overall, Alphabet is evolving beyond its reliance on advertising into a more diversified, AI-driven business, with cloud and AI services emerging as key pillars of its future growth.

Alphabet’s Rising Capital Expenditure Signals Confidence, Not Concern

Alphabet has raised its 2026 capital expenditure guidance, now projecting total spending of $180 billion to $190 billion, up from its prior estimate of $175 billion to $185 billion. The upward revision is attributable to incremental investment requirements linked to its acquisition of Intersect.

Notably, elevated capital expenditures across the technology sector have drawn increased scrutiny from investors. However, Alphabet’s AI investments are already translating into tangible results, including strong revenue across its core services and a growing backlog in its Google Cloud division. These outcomes help explain and support the company’s decision to increase its capital expenditure.

Why GOOGL Stock Could Reach New Highs

Alphabet’s transformation into an AI-first company is driving strong growth across its business segments. Strong advertising performance, hypergrowth in cloud driven by AI workloads, solid demand for its custom TPUs, expanding margins, and a record backlog indicate that Alphabet stock could hit new highs.

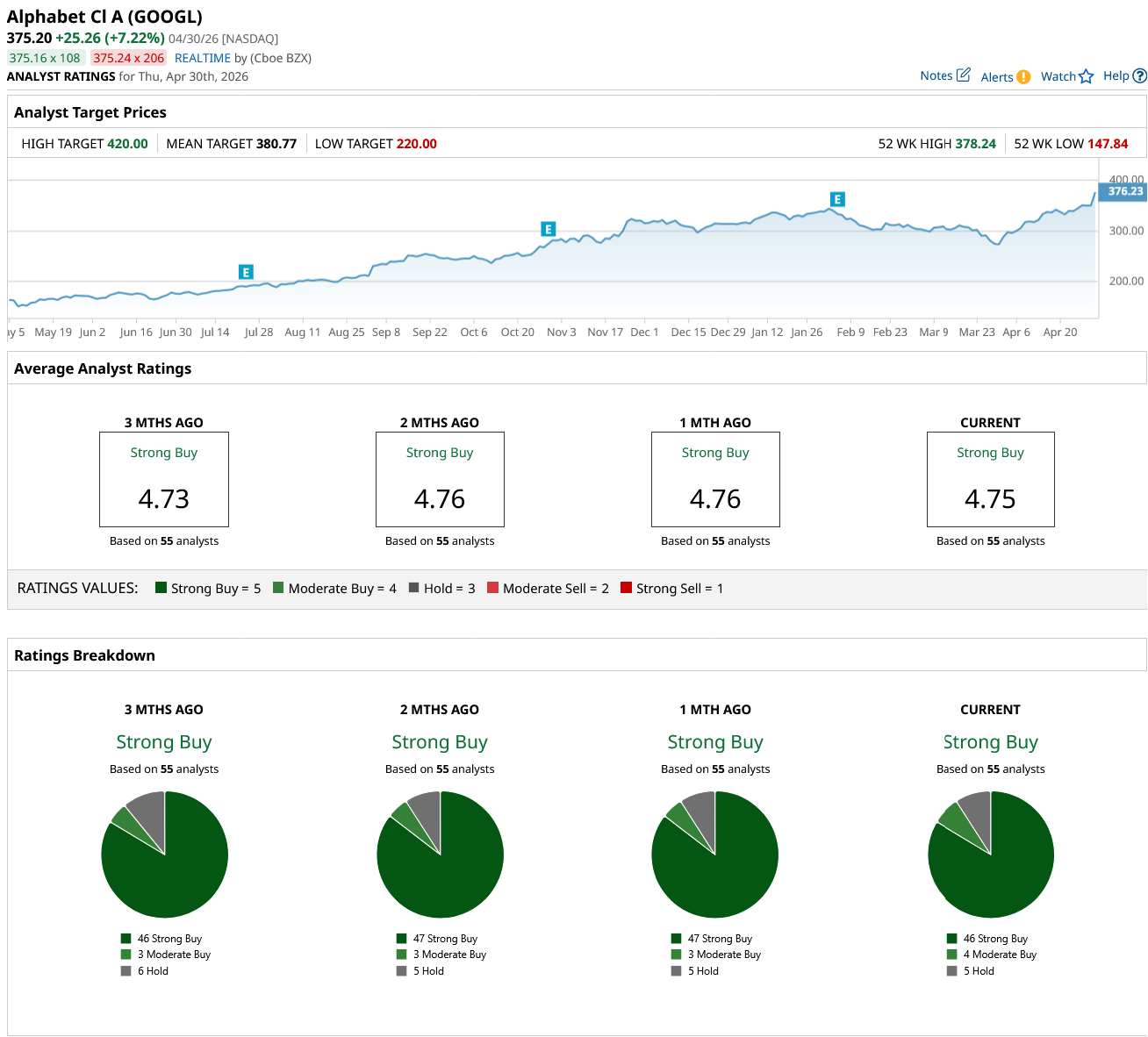

Analysts are upbeat and likely to raise their earnings forecast and price target following Q1 earnings. At the same time, GOOGL stock has a consensus “Strong Buy” rating.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)