With roots dating back to 1866, Nestlé (NSRGY) is one of the largest food and beverage companies globally. Last week, the company released its three-month sales report and, although sales declined, the market still reacted positively. NSRGY stock jumped almost 5% after the report — and closed the next day with another 2% gain.

What was the hidden factor that made Nestlé stock surge despite weak sales? Let's take a closer look.

Currency Headwinds Masked the Real Performance

For the first quarter of 2026, Nestlé reported CHF 21.3 billion in sales, down 5.7% year-over-year (YOY). At first glance, the numbers appear discouraging. However, currency headwinds played a major role, with foreign exchange alone dragging reported sales down by 9.3%. Ignoring the impact of the currency headwinds, organic growth climbed 3.5%, driven by 1.2% real internal growth (RIG) and 2.3% pricing.

Nestlé’s portfolio spans everyday consumer staples such as coffee, bottled water, dairy products, baby food, pet food, chocolates, and ready-to-eat meals, all of which remain in high demand regardless of economic conditions. So, although reported sales reflect macro pressures like currency fluctuations, organic growth highlights the company’s actual operating momentum. This shows that Nestlé is still expanding.

One of the key reasons the company's sales keeps increasing is its ability to raise prices without significantly damaging demand. This gives the company pricing power as customers are absorbing price increases, even in a more cautious global environment. Coffee, in particular, generated 9.3% organic growth, with strong momentum across brands, particularly Nescafé. Overall, the company’s performance improved in emerging markets with 4.6% organic growth, compared to 2.8% organic growth in developed markets. This implies that Nestlé’s long-term growth story remains intact, driven by rising consumption in developing economies. These emerging markets are not only growing faster but also contributing meaningfully to volume expansion rather than just pricing.

The Only Temporary Setback in Q1

The only drag this quarter was the infant formula recall, which had a minor impact on organic growth. The infant formula recall in early 2026 was triggered by the detection of cereulide, a toxin linked to a contaminated third-party ingredient (ARA oil), making it an industry-wide problem rather than a Nestlé-specific failure. Regulators tightened testing standards and the recall expanded across multiple countries and batches.

Nestlé pulled its affected products, switched suppliers, and strengthened safety protocols to restore supply and consumer trust. Management expects a full recovery by the end of the year. Nutrition segment growth declined 3.9%, largely due to this issue rather than any underlying demand issue. In other segments, Food & Snacks saw 4.2% organic growth — supported by improving confectionery demand — while Petcare remained resilient, growing 2.7% YOY.

Nestlé is actively reshaping its portfolio, including exploring partnerships for its Waters business and agreeing to sell Blue Bottle Coffee. It is also investing heavily in brand building and marketing. The company expects organic growth between 3% and 4% and improved margins in 2026. Management also reaffirmed expectations to generate free cash flow above CHF 9 billion. This upbeat outlook is probably why NSRGY stock surged.

The Bottom Line on Nestlé Stock

For investors looking for aggressive growth, Nestle is not the stock for you. As a consumer company, it generates reliable cash flow, maintains dividends, and operates in essential categories like food, coffee, and pet care — markets that tend to remain stable even during economic slowdowns. For investors looking for portfolio stability, consistent returns, and downside protection, Nestlé fits well as a defensive holding in a diversified portfolio.

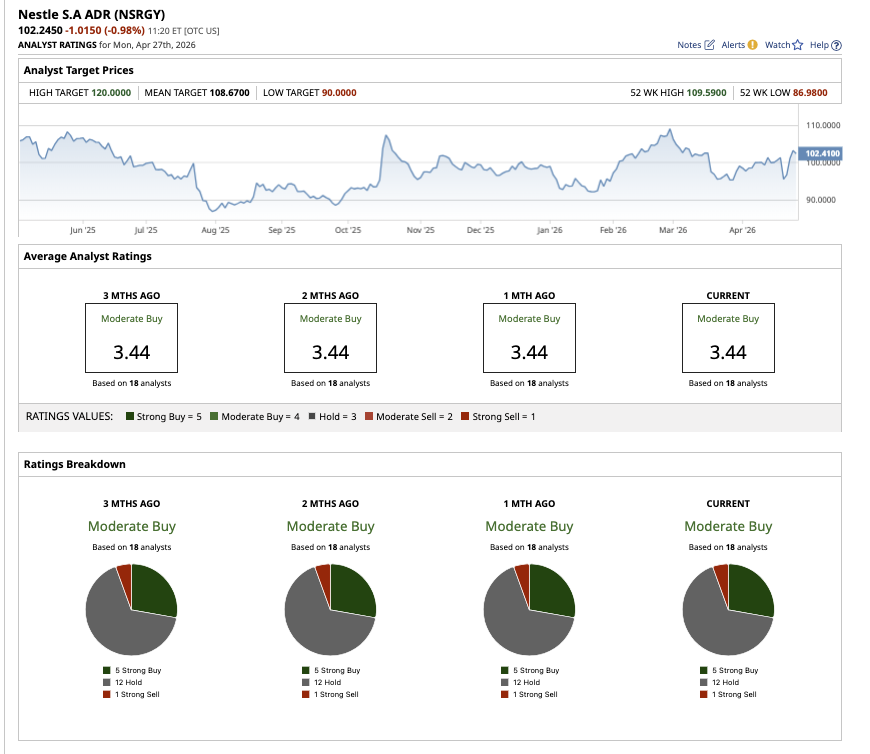

On Wall Street, NSRGY stock holds an overall “Moderate Buy” rating. Of the 18 analysts with coverage, five have a “Strong Buy,” 12 have a “Hold" rating, and one analyst has a “Strong Sell.” The average target price is $103, which implies just over 1% potential upside from current levels. The Street-high estimate of $116 suggests the stock could climb by 14% over the next year.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Unitedhealth%20Group%20Inc%20HQ%20photo-by%20jetcityimage%20via%20iStock.jpg)