/Oracle%20Corp_%20logo%20on%20phone-by%20WonderPix%20via%20Shutterstock.jpg)

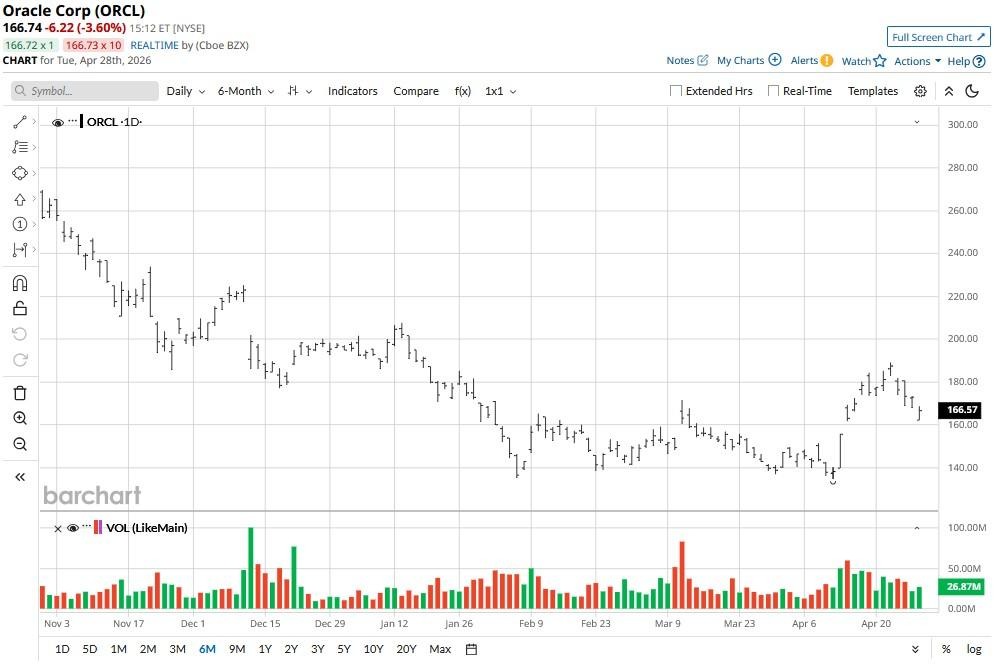

Oracle (ORCL) shares are under immense pressure on April 28 following a Wall Street Journal report that OpenAI, the company behind ChatGPT, is seeing a slowdown in revenue and user growth.

The selloff pushed ORCL below its 100-day moving average (MA), a technical setup that is often interpreted as shifting momentum in favor of the bears.

Including today’s decline, Oracle stock is down about 19% versus its year-to-date high.

What the OpenAI News Really Means for Oracle Stock

Investors are bailing on ORCL stock primarily because the company serves as a key infrastructure supplier to OpenAI’s training ambitions.

If the AI research lab is seeing both revenue and user growth stall, it’s reasonable to assume that a pullback in mode-trailing, intensity, GPU demand, and data-center buildouts will follow.

And that would hurt Oracle, given it’s heavily levered to all of those through its multi-year cloud and compute commitments.

A weaker OpenAI trajectory signals softer utilization of Oracle’s artificial intelligence (AI) clusters, lower long-term cloud revenue, and potentially unnecessary debt-funded capacity expansion.

Is It Worth Investing in ORCL Shares Today?

Long-term investors should still consider loading up on Oracle shares today, given the NYSE-listed firm has signed massive supercluster deals with other enterprise giants as well, including Meta Platforms (META).

In fact, the company ended its third quarter with $553 billion worth of remaining performance obligations (RPOs), up a remarkable 325% on a year-over-year basis.

Still, ORCL is trading at a forward price-to-earnings (P/E) ratio of about 28x currently, which does not look particularly stretched given it’s an AI beneficiary.

A history of closing the next three months (May, June, July) in the green makes Oracle exciting in the near term, while a healthy 1.2% dividend yield is why it’s attractive for long-term, income-focused investors as well.

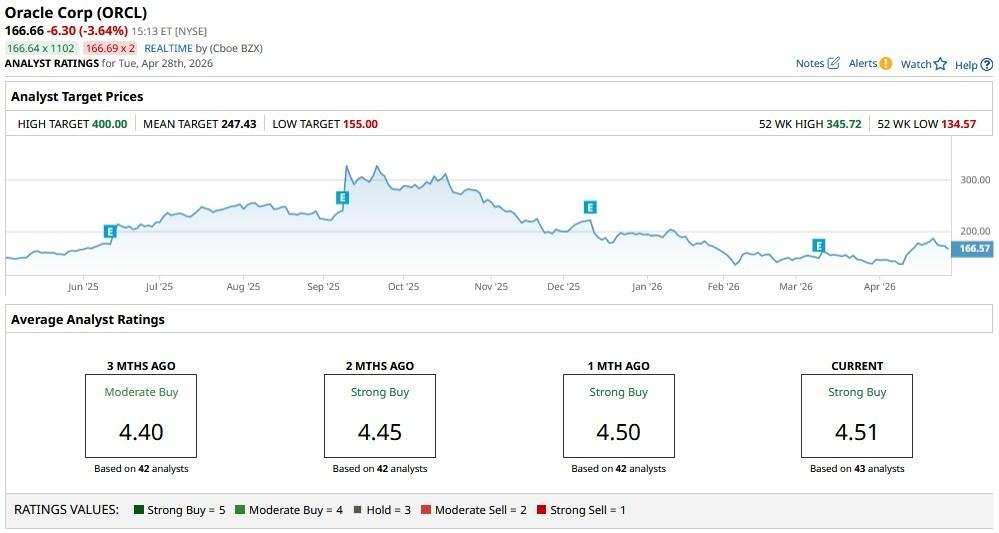

What’s the Consensus Rating on Oracle?

It's also worth mentioning that Wall Street expects Oracle to rip much higher from here over the next 12 months.

According to Barchart, the consensus rating on ORCL shares remains at “Strong Buy,” with the mean price target of about $247 indicating potential upside of a whopping 50% from current levels.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)