/A%20Lucid%20Motors%20vehicle%20parked%20in%20front%20of%20a%20showroom_%20Image%20by%20Michael%20Berlfein%20via%20Shutterstock_.jpg)

Lucid Group (LCID) shares tanked this week after the electric vehicle (EV) maker named Silvio Napoli its new permanent chief executive (CEO).

Napoli, who most recently served in a similar capacity at Schindler Group, brings decades of experience in managing global operations and scaling complex manufacturing organizations.

While he’s an auto-industry outsider, the board cited his track record of manufacturing excellence and building tech-enabled, service-oriented businesses as qualities needed for the company’s next phase.

Lucid stock is now down about 30% in the past month.

Should You Invest in Lucid Stock Today?

In a post-appointment statement, Napoli said his priorities at Lucid Group will center on consistent execution, financial discipline, and translating tech innovations into long-term value.

This emphasis on operational rigor rather than engineering vision represents a meaningful strategic shift for a company that has historically been defined by its tech-first identity under Rawlinson.

Still, the market’s reaction was decidedly negative, especially since Lucid’s fundamental picture remains deeply troubling, with a negative $3.8 billion free cash flow, reinforcing that profitability remains distant.

Even from a technical perspective, LCID shares currently sit decisively below their major moving averages (MAs), indicating a strong downtrend.

Why LCID Shares Are Still Unattractive

Alongside naming its next permanent CEO, Lucid pre-announced its Q1 revenue that missed Street estimates by an alarming 35%, making the EV stock even less attractive to buy on the dip.

In Q1, the firm delivered 3,093 vehicles against expectations of 5,237, largely due to a 29-day supplier disruption involving second-row seats.

Meanwhile, operating loss approached $1 billion, continuing a pattern where the company spends roughly twice as much to build each car as it collects in revenue.

Overall, hiring Napoli as CEO is rational for LCID, given that its primary challenge has shifted from tech development to operational scaling and cost management.

However, that doesn’t automatically resolve the fundamental issues of massive cash burn, chronic production shortfalls, dilute capital raises, and a competitive EV landscape that continue to haunt Lucid shares.

Wall Street Hasn’t Thrown in the Towel on Lucid

Despite the aforementioned risks, Wall Street seems to believe the year-to-date crash in LCID stock is rather overdone.

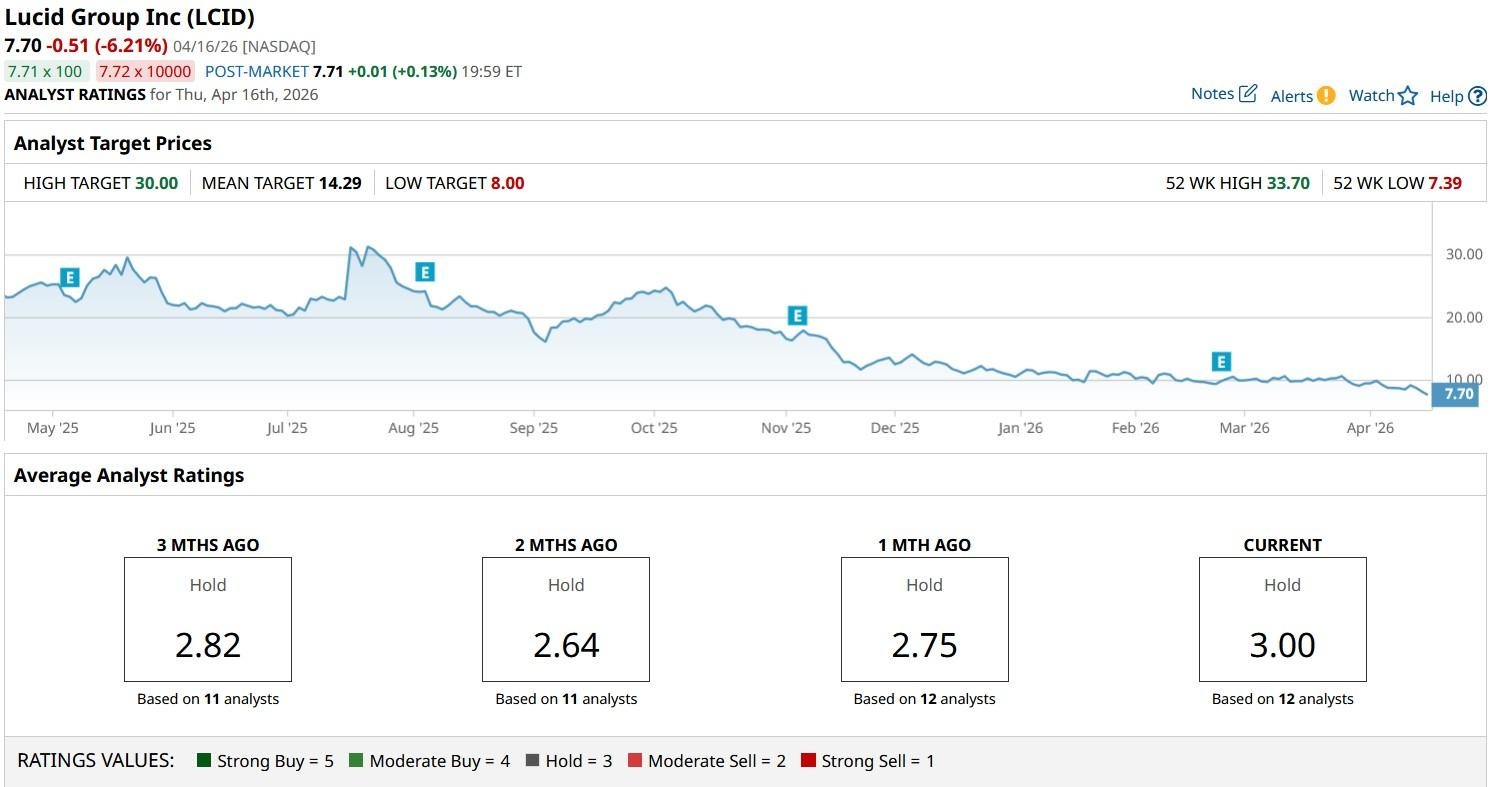

While the consensus rating on Lucid Group sits at a “Hold," the mean price target of about $14 indicates potential upside of a whopping 80% from here.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)

/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)