/Ulta%20Beauty%20Inc%20sign%20by-%20damann%20via%20Shutterstock.jpg)

As tensions flare around the Strait of Hormuz, oil prices refuse to sit still, and U.S. gas prices climb in lockstep, hitting consumers right where it hurts. Analysts across the consumer sector are keeping their ear to the ground, watching the ripple effect squeeze spending, especially among lower-income households already walking a tightrope.

John San Marco of Neuberger Berman, an investment management firm, has run the math and called it as he sees it. The surge in gas prices has wiped out the tax benefit for roughly two-thirds of consumers. However, higher income groups still land on their feet, enjoying the refund tailwind as tax law changes are tilting the scales in their favor and keeping them relatively insulated from rising fuel costs.

This is where Ulta Beauty (ULTA) is stealing the spotlight. San Marco points to the lipstick effect, a classic case of consumers tightening the belt on big-ticket items but still finding room for small indulgences to keep spirits up. When push comes to shove, people may skip the splurge but still grab a feel-good purchase, and Ulta sits right in that sweet spot.

The proof is in the pudding. The beauty products retailer’s fourth quarter fiscal 2025 update shows demand holding firm, even as shoppers think twice before opening their wallets. Meanwhile, CEO Kecia Steelman has kept the wheels turning with a strategy reset and leadership buildout under the Ulta Beauty Unleashed plan.

The company rolled out 100 new brands in 2025 and stayed culturally plugged in through events like the Cowboy Carter Tour, Lollapalooza, and Coachella, while also sharpening its e-commerce game. As volatility calls the shots, Ulta may look like an unlikely safe harbor, yet it just might help investors keep their footing when the ground starts to shift.

About Ulta Beauty Stock

Headquartered in Bolingbrook, Illinois, Ulta Beauty stands tall as the largest specialty beauty retailer in the U.S., serving as a one-stop shop for cosmetics, fragrance, skin care, hair care, wellness, and salon services. Since opening its first store in 1990, the company has grown like wildfire to 1,505 locations across the country.

With a market cap of $23.3 billion, Ulta sells through brick and mortar stores, e-commerce platforms, and mobile apps, blending branded and private label products with salon tools and services.

Over the past 52 weeks, the stock has climbed 49.65%, though it has hit a rough patch lately. It is down 11.42% year-to-date (YTD), and has gained only marginally over the last month, proving that even strong runners sometimes lose their footing.

When it comes to valuation, Ulta Beauty is not exactly scraping the bottom of the barrel. The stock is currently trading at 18.50 times forward adjusted earnings and 1.76 times sales, comfortably sitting above industry norms. Even so, when you stack those numbers against their own five-year track record, they start to look like a bargain hiding in plain sight.

A Closer Look at Ulta Beauty’s Q4 Earnings

On March 12, Ulta Beauty reported its fourth quarter fiscal 2025 results, posting revenue of $3.9 billion and beating Street expectations of $3.83 billion, thanks to higher comparable sales, the acquisition of Space NK, and contributions from new stores.

Even so, the market did not roll out the red carpet. The stock dropped 4.3% on the announcement day and then took another hit of 14.2% in the following session, as investors focused on the cracks beneath the surface.

Comparable sales rose 5.8%, driven by a 4.2% jump in average ticket and a 1.6% increase in transactions. Operating income fell 7.6% from the prior year’s period to $476.9 million, while net income plunged 9.3% to $356.7 million. EPS landed at $8.01, down 5.3% year-over-year (YOY) and just a hair below the $8.03 analysts expected.

The pressure came largely from a 23.4% surge in SG&A expenses, as Ulta poured money into modernizing its supply chain. The company has been front-loading investments into automated distribution to trim labor costs down the line.

At the same time, management has been going all in on virtual try-on technology and TikTok shop integrations as part of the broader Ulta Beauty Unleashed push. Over time, these moves would boost efficiency and expand margins, which makes the post-earnings dip look like an opportunity knocking for patient investors.

Ulta’s management expects fiscal year 2026 net sales to grow between 6% and 7%, with diluted EPS landing between $28.05 and $28.55.

Analysts are not blinking either. They expect first-quarter fiscal 2026 EPS to rise 3.9% YOY to $6.96. For the full year, they see earnings climbing 11% to $28.47 and then pushing another 11% higher to $31.59 in fiscal year 2027.

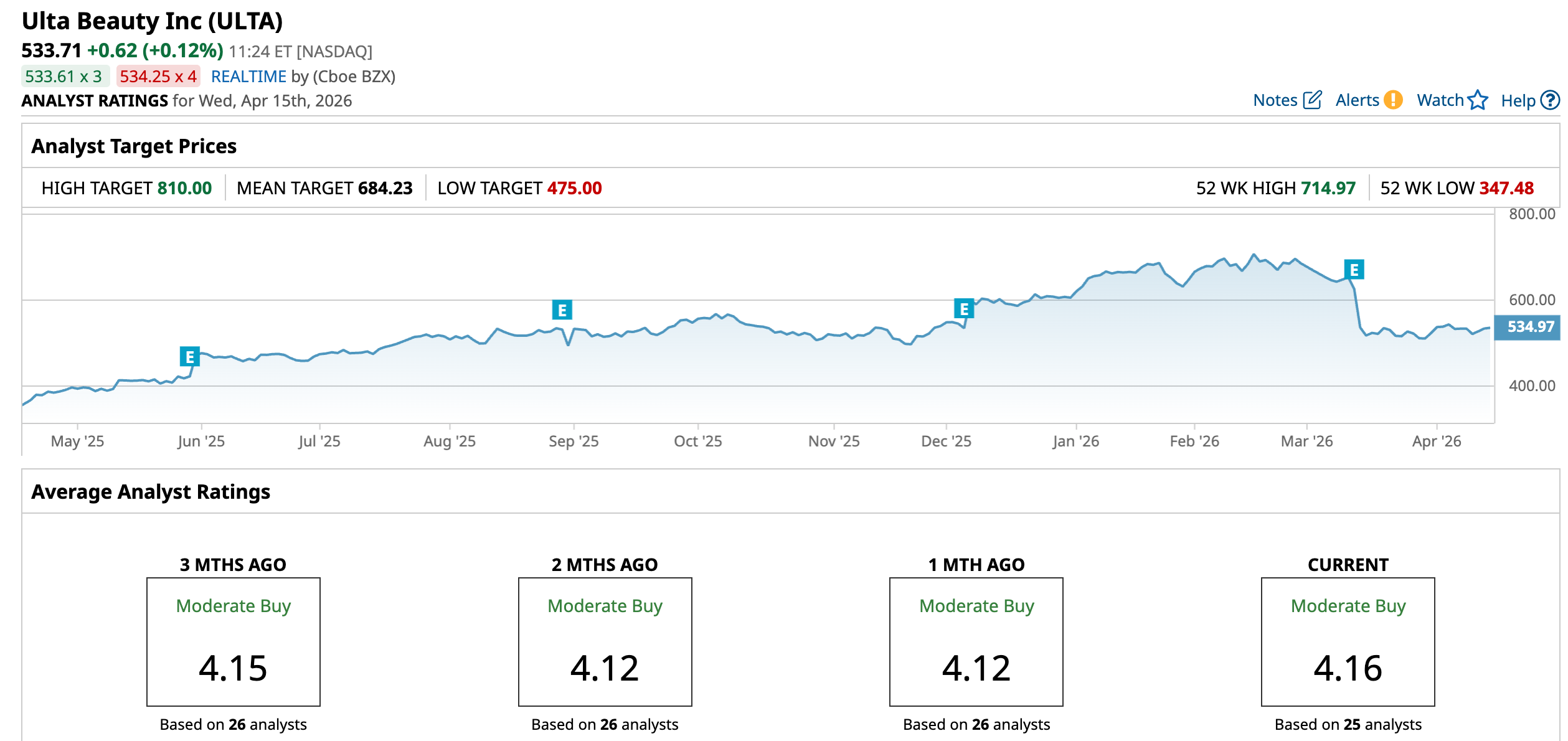

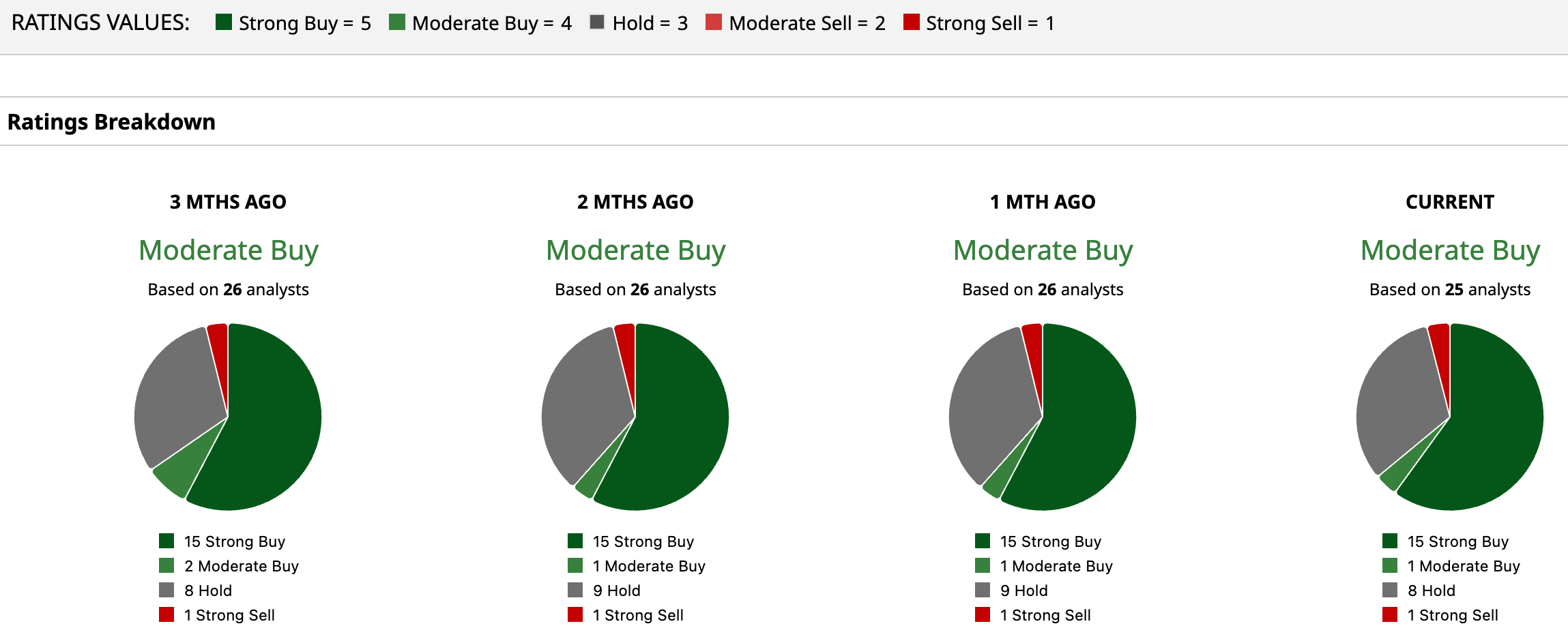

What Do Analysts Expect for Ulta Beauty Stock?

Wall Street has placed ULTA stock firmly in “Moderate Buy” territory. Out of 25 analysts covering the stock, 15 have issued “Strong Buy” ratings, one has gone with “Moderate Buy,” eight have stayed on “Hold,” and one has waved a “Strong Sell” flag.

To that end, the stock’s average price target of $684.23 suggests potential upside of 28.2%. Meanwhile, the Street's high target of $810 suggests a gain of 51.8% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

/Johnson%20%26%20Johnson%20location%20sign-by%20JHVEPhoto%20via%20iStock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)