Disney (DIS) shares are in focus on Friday morning following reports that the entertainment giant plans on cutting roughly 1,000 jobs, primarily within its newly consolidated marketing division.

This restructuring, led by the company’s new chief executive, Josh D’Amaro, aims to centralize operations and reduce duplication across its streaming and film segments, the reports added.

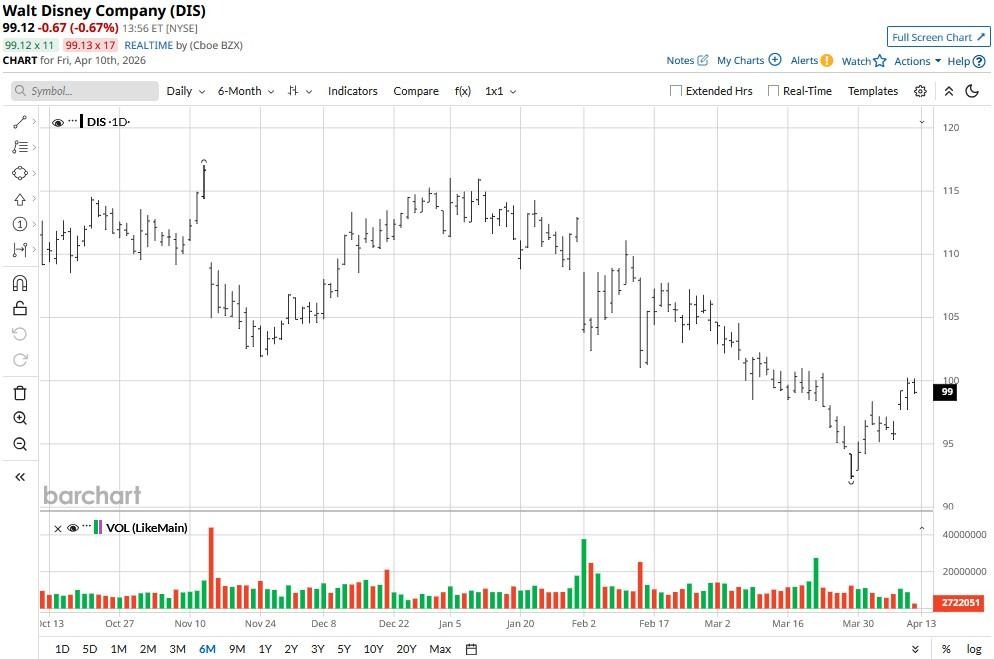

Disney stock has been in a downtrend since the start of 2026, currently trading at about a 15% discount to its year-to-date high.

What These Layoffs Really Mean for Disney Stock

The potential impact of these layoffs is a double-edged sword for investors. From a bullish perspective, these cuts signal a disciplined shift toward leaner operations and improved margins.

By centralizing marketing under its “One Disney” strategy, the company can eliminate redundant roles and pivot resources toward high-growth areas like theme park expansions.

Conversely, the move can be viewed as bearish for DIS shares, suggesting that organic growth in the streaming and linear TV segments has now plateaued.

Critics argue that repeated workforce reductions may damage creative morale and indicate that cost-cutting is the only remaining lever for Disney to sustain profitability in a volatile media landscape.

What Makes DIS Shares Worth Owning in 2026

Beyond headline noise, Disney shares remain compelling for long-term investors given they’re trading at about 15x forward earnings — well below their historical valuation multiple.

The stock looks strongly positioned for a meaningful recovery as management continues to scale Disney+ toward consistent profitability in 2026.

Meanwhile, the giant’s experiences segment, which recently posted record operating income of $3.31 billion, adds to enthusiasm, reinforcing the strength of its high-margin, demand-resilient businesses.

A healthy dividend yield of 1.51% makes DIS even more attractive as a long-term holding, at least for income-focused investors.

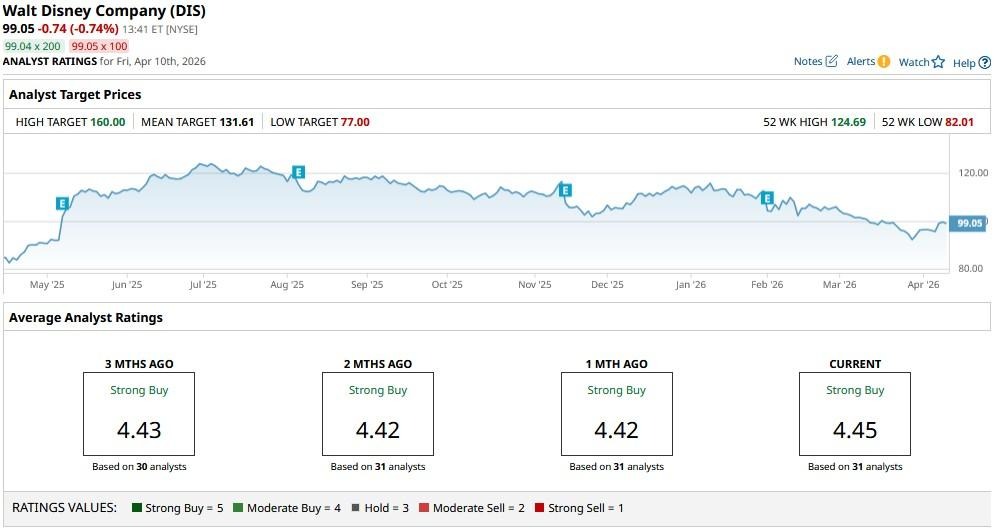

Wall Street Remains Bullish on Disney

Investors could also take heart in the fact that Wall Street remains bullish on Disney, citing its massive $60 billion investment planned for parks and cruises as a powerful tailwind for long-term recovery.

The consensus rating on DIS stock sits at a “Strong Buy” currently, with the mean price objective of about $131 indicating potential upside of more than 30% from here.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/Friends%20choosing%20a%20movie%20on%20a%20streaming%20service%20by%20Stock-Asso%20via%20Shutterstock.jpg)