/Bank%20Of%20New%20York%20Mellon%20Corp%20location%20sign-by%20JHVEPhoto%20via%20Shutterstock.jpg)

Legacy financial institution Bank of New York Mellon (BK) secured a crucial win from the U.S. government when it was picked as the designated financial agent for the “Trump Accounts” program. A tax-advantaged account to instill the habit of savings and investment from a child's younger years; under the program, the government will provide a one-time $1,000 contribution for U.S. citizen children born between Jan. 1, 2025, and Dec. 31, 2028. Part of the One Big Beautiful Bill Act (OBBBA) of 2025, the scheme's investment avenues are restricted to low-cost and relatively safer instruments such as ETFs or low-cost index funds.

BNY will, along with Robinhood (HOOD), develop the app and handle the initial accounts. Notably, the Wall Street major is a lead developer of the underlying infrastructure of the app, along with having the responsibility for the actual custody of the funds and securities within the accounts.

About Bank of New York Mellon

Founded way back in 1784 as the Bank of New York and known in its current avatar since 2007 after its merger with Mellon Financial, BNY engages in several financial activities. Its core businesses include asset management, asset servicing, securities services, and treasury and payments.

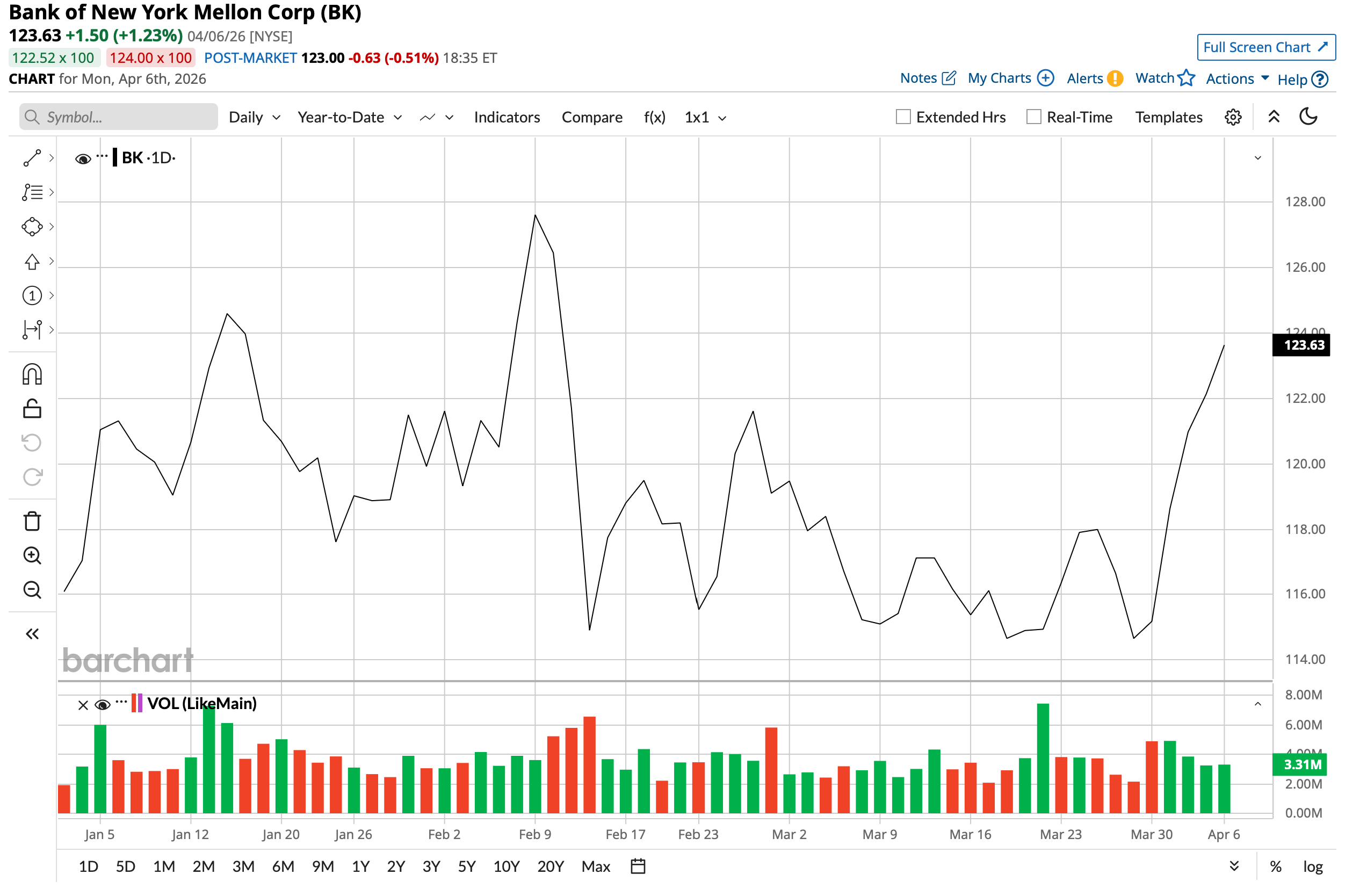

Valued at a market cap of $84.1 billion, BK stock is up 6% on a year-to-date (YTD) basis. Further, the stock offers a dividend yield of 1.75%.

So, how much of a shot in the arm can this government win be for BK stock? Are there other reasons to own this one, or is it an avoid? Let's find out.

Upbeat Q4

BNY's results for the most recent quarter were impressive, as both revenue and earnings surpassed Street estimates. While total revenues increased by 7% from the previous year to $5.2 billion, earnings soared at an even higher rate of 31% in the same period to $2.02 per share. Not only was this higher than the consensus estimate of $1.91 per share, but it was also the fourth consecutive quarter of earnings beat from the company.

Overall, BNY has clocked revenue and earnings CAGRs of 5.27% and 9.02%, respectively, over the past five years; that's particularly excellent when one considers the scale of its operations.

Furthermore, BNY's assets under custody increased to a whopping $59.3 trillion from $52.1 trillion in the year-ago period. Average deposits and loans also witnessed yearly rises of 8% and 11% to $310.5 billion and $76.7 billion, respectively. The gap is normal for a financial institution like BNY, as its primary line of business is asset servicing and not giving out loans.

Some key operating and solvency metrics also improved, as Return on Tangible Capital Employed improved to 26.6% from 23.3% in Q4 2024, along with pre-tax operating margin at 36% compared to 30% in the prior year. The Common Equity Tier 1 ratio rose to 11.9% from 11.2%, much higher than the required 8.5% for a company like BNY.

Finally, the quarter also saw BNY returning about $5 billion to shareholders in the form of share repurchases ($3.5 billion) and dividends ($1.5 billion). And on a forward P/B basis, the stock is trading at 1.99, just above the sector median of 1.15. Overall, analysts are projecting BNY to have a forward EPS growth rate of 17.15%, higher than the sector median of 14.54%.

Strategic Drivers

BNY's structural strength was certainly a contributing factor to its becoming the partner of choice for the Trump Accounts program. The Treasury Department officially tapped the institution because it sits at the absolute center of American financial plumbing. With nearly $60 trillion in assets under custody, BNY possesses the unparalleled scale and regulatory framework necessary to securely manage millions of new government-funded starter portfolios.

Moreover, BNY dominates asset servicing simply because changing custody banks is a logistical nightmare for large institutions. This immense switching cost creates a deeply sticky client base that acts as a wide economic moat against competitors like State Street and Northern Trust. Their sheer size allows them to price their services aggressively while still turning a profit.

To grow this core segment, management is pivoting away from basic asset holding toward higher-margin data solutions. They are charging clients not just to store assets but to analyze and report on them. Additionally, BNY is aggressively expanding its servicing capabilities for exchange-traded funds and alternative private markets, capturing the ongoing shift away from traditional mutual funds.

Further, beyond basic custody, the institution is aggressively expanding its wealth management and treasury services divisions to diversify revenue. A major growth engine is their new wealth management platform called Wove, which gives independent financial advisors a unified digital workspace to manage client portfolios. Technology and AI are the absolute focal points of this expansion.

Notably, instead of just adding headcount, management is deploying AI to automate mundane back-office tasks like trade settlement reconciliation and data entry. This allows BNY to expand its profit margins through massive operational leverage. BNY is also using predictive analytics to offer real-time liquidity management tools, helping corporate clients optimize their cash flows much faster than legacy systems previously allowed.

However, the most immediate headwind plaguing the company is severe fee compression within its legacy asset servicing division. Institutional clients are constantly negotiating pricing downward, forcing the bank into a relentless race to cut costs just to maintain profitability. Additionally, their asset management arm is heavily exposed to the industry-wide bleeding of capital from active management into passive index funds, which inherently generate significantly lower fee revenue.

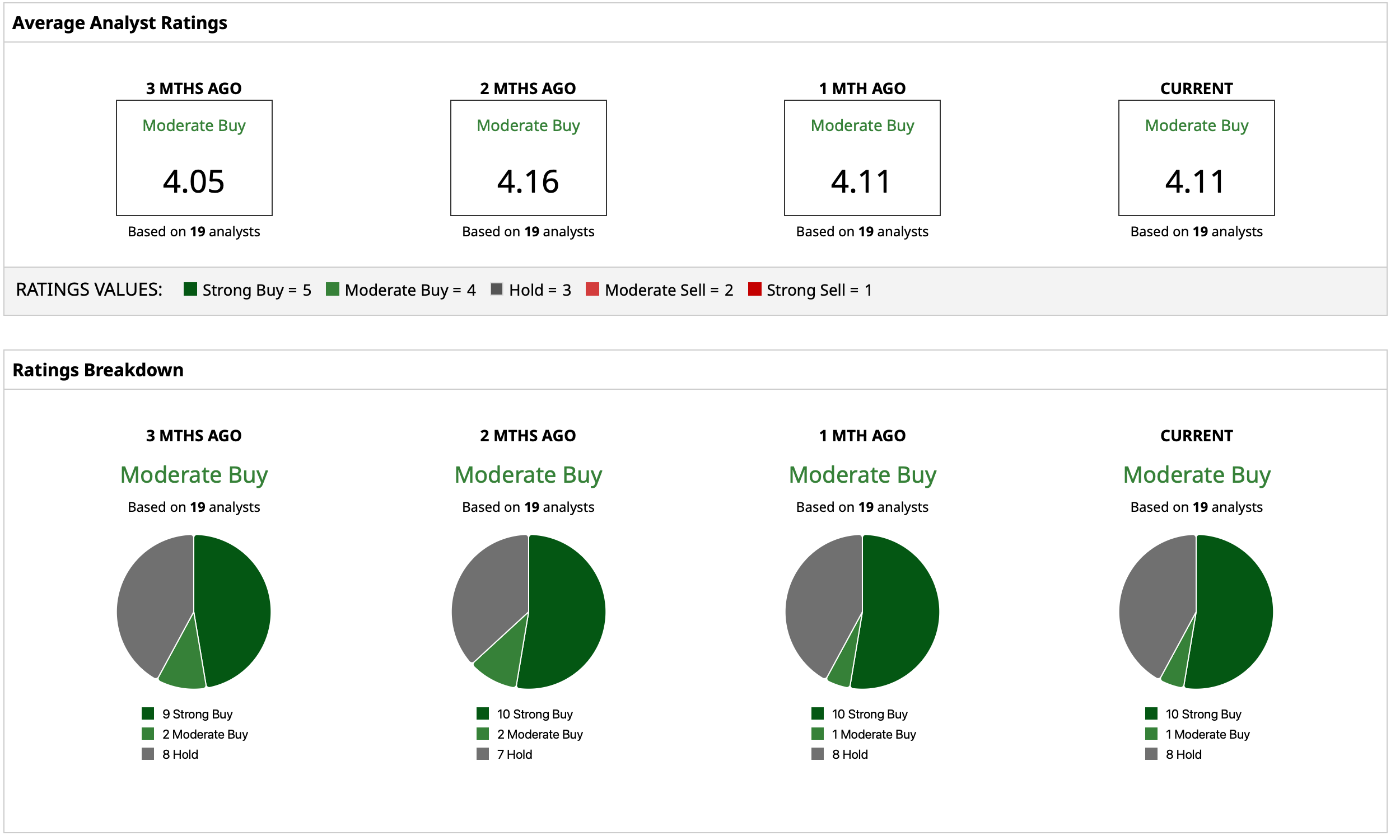

Analyst Opinion of BK Stock

Thus, analysts have deemed BK stock a consensus “Moderate Buy,” with a mean target price of $134.32, which indicates an upside potential of about 8.6% from current levels. Out of 19 analysts covering the stock, 10 have a “Strong Buy” rating, one has a “Moderate Buy” rating, and eight have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Doctor%20stacking%20healthcare%20medical%20insurance%20icons%20by%20Dilok%20via%20Adobe%20Stock.jpeg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)