Blue Owl (OWL) stock has faced intense pressure in recent sessions after the company announced an alarming $5.4 billion in redemption requests across its flagship credit and tech-focused funds.

The selloff crashed OWL’s relative strength index (14-day) back into the oversold territory (below 30), signaling the asset management firm may be due for a technical rebound.

Blue Owl shares have been a disappointment for investors this year, trading down more than 45% versus its year-to-date high at the time of writing.

Why Are Redemption Requests Bearish for Blue Owl Stock

The recently disclosed flood of redemption requests is a major headwind for OWL shares because it challenges the “permanent capital” narrative that once made them a market darling.

When investors request to pull over 20% of a flagship fund and 41% of a tech-focused vehicle in a single quarter, it signals a profound crisis of confidence.

To meet these demands, Blue Owl may be forced into defensive asset sales or gating funds, which would hamper its ability to earn performance fees and raise concerns about the underlying valuation of illiquid loans.

Moreover, the concentrated exposure to software companies — potentially vulnerable to AI-driven disruption — has investors fearing that these requests are just the tip of the iceberg for future credit losses.

Is It Worth Buying OWL Shares on the Pullback?

Despite the concerning headline, there’s reason to stick with Blue Owl stock, especially if you’re a long-term investor.

The New York-headquartered firm recently sold $1.4 billion in direct lending assets at 99.7% of par value, proving its credit book is high-quality and liquid enough to satisfy institutional buyers.

With a dividend yield not exceeding 10% and the technical RSI indicating a washout bottom, the current pullback offers a compelling entry point for those interested in betting on the resilience of the private credit asset class.

Note that OWL is now trading at a rather attractive 4.7x sales as well.

How Wall Street Recommends Playing Blue Owl Capital

Investors should also take heart that Wall Street firms remain bullish on Blue Owl Capital.

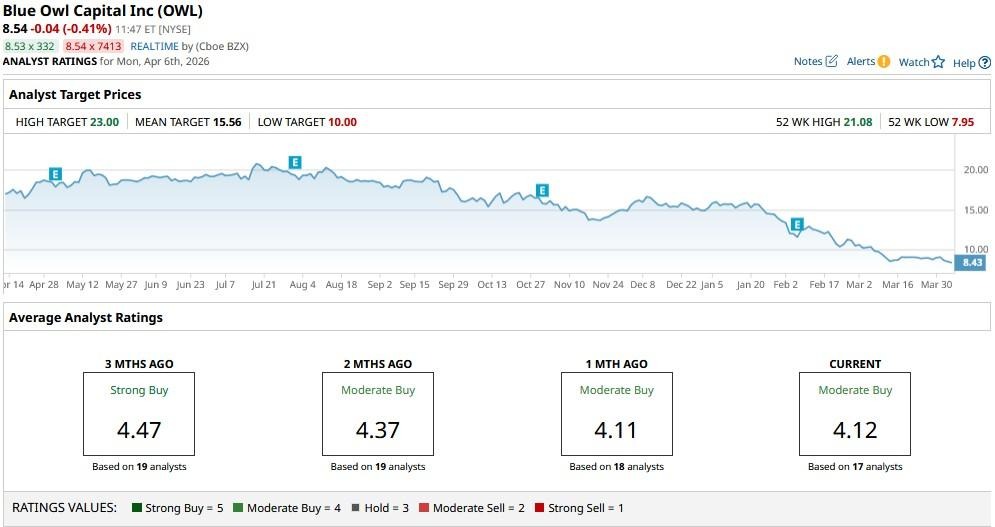

According to Barchart, the consensus rating on OWL stock is a “Moderate Buy,” with the mean price target of $15.56 indicating potential upside of nearly 85% from here.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)