Weather - delta-river-in-the-daytime-the-river-flows-into-the-sea

- Continued dry weather across the US Plains and Midwest is having an effect on all the major US grain markets.

- This has raised concern for both 2022 and 2023 production, all while South America and Ukraine remain question marks.

- As I've mentioned a number of times, until weather patterns change interest rate hikes won't be enough to completely corral global inflation.

There are three big stories in the grain and oilseed sector, with all three again highlighting my idea agriculture production markets are, at their core, weather derivatives.

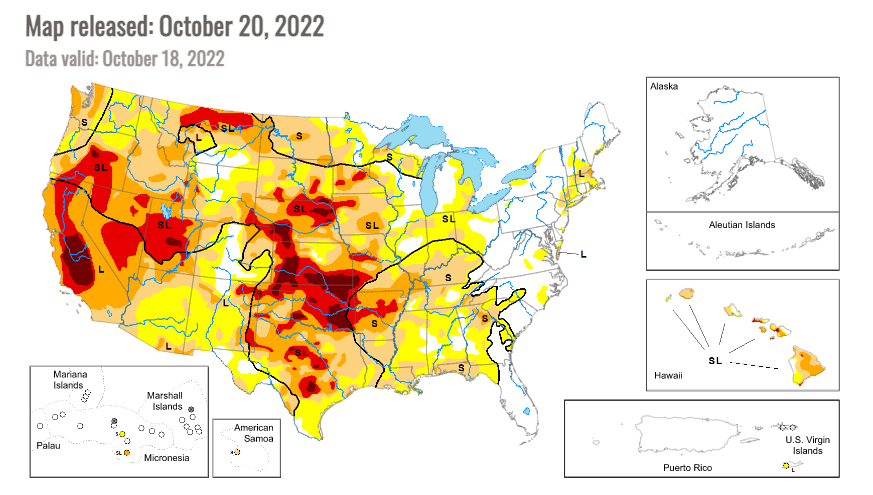

- The US Southern Plains HRW wheat (KEN23) growing area remains in an extreme drought situation, according to the latest US Drought Monitor map (for the week ending Tuesday, October 18). The reality is much of the 2023 crop has been planted in the dust, not an optimal situation and certainly not since there are serious concerns about how much wheat will be planted in Ukraine for next year.

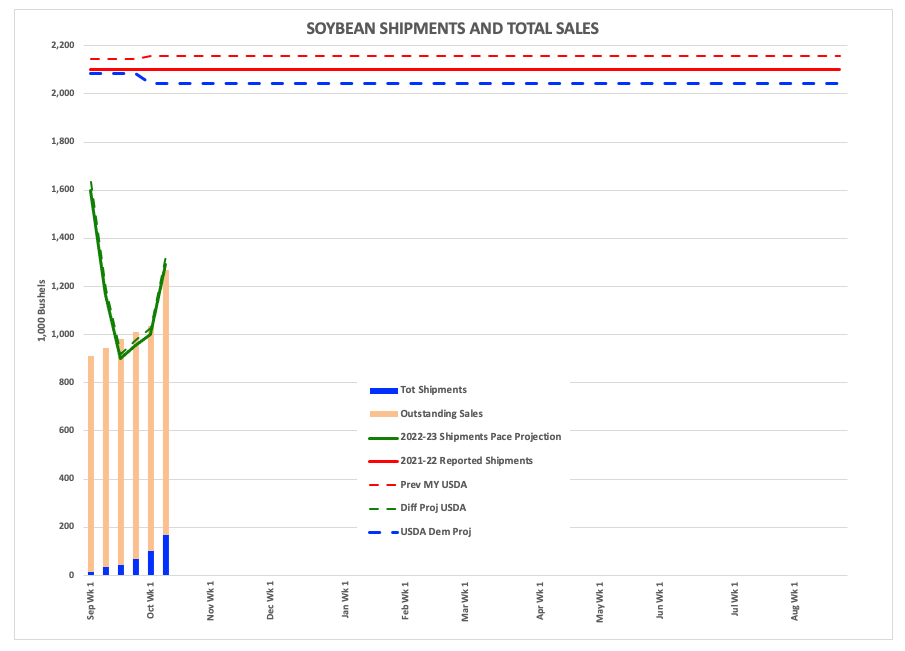

- The Mississippi River is not so mighty these days, but instead acting more like Old Man River as its flow has slowed to a trickle. There have been some incredible videos on social media showing people walking in its riverbed, the river itself barely visible in the distance. This has a number of economic impacts on the US, with one of the key points being barges can’t get grain to export facilities at and around New Orleans. The ripple effects, or lack thereof, are being felt in the US soybean (ZSPAUS.CM) market as most of its shipments occur the first half of the marketing year. Historically, the US has exported 35% of what turns out to be its marketing year total by the end of November (Q1) and 70% by the end of February (Q2). The most recent weekly update showed US shipments, for the week ending Thursday, October 20, at only 168 mb, a pace that projects total shipments of only 1.3 bb.

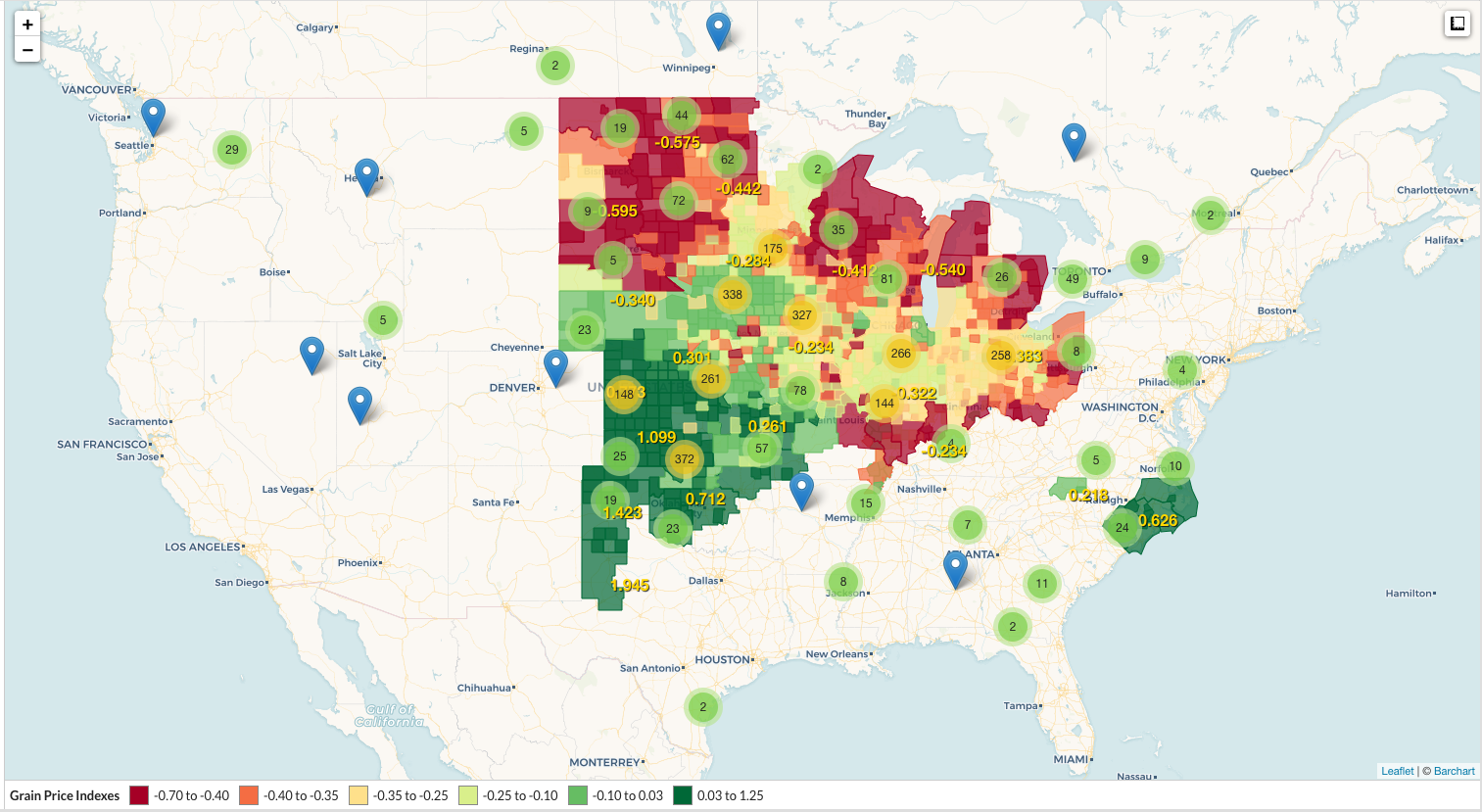

- Whenever Dad’s side of the family got together for holidays, celebrations, whatever the day always ended with the entire clan playing the card game Pitch. The big table held most of us, with the game being 10-point Call Your Partner. My Grandad ran it with an iron fist. If you won there, you moved to the small 4-person table where Dad and my uncle held court playing 5-point Cutthroat. I was reminded of this again as I heard stories of what feed yard and ethanol plant merchandisers are doing to find corn (ZCPAUS.CM) supplies this fall. The bottom line is the basis market is skyrocketing, a hot topic for both my appearances on RFD-TV this week as we discussed the Barchart Ag Corn Basis Map. What has happened to the corn basis market? We knew going in US available stocks-to-use were tighter than what official numbers were telling us, and the same drought across the US Plains and Midwest that has drained the Mississippi River dropped corn production in those areas as well. What has been harvested is being locked up tight in on-farm storage, possibly until January or maybe not until next spring or summer.

All this fits with my ongoing belief that interest rate hikes alone aren’t going to be enough to solve inflation if Mother Nature is going to continue to play hardball when it comes to US and global grain and oilseed production. And as I was nearing the end of this piece, the story came across on CNBC that another rail union had rejected the latest contract proposal. This puts the spotlight on the next possible strike date of November 19.

More Grain News from Barchart

- Wheat Bounced on Thursday

- Double Digit Gains in Bean Market

- Corn Closes Higher on Thursday

- Coffee Prices Remain Weak on the Outlook for Improved Brazil Coffee Production

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)