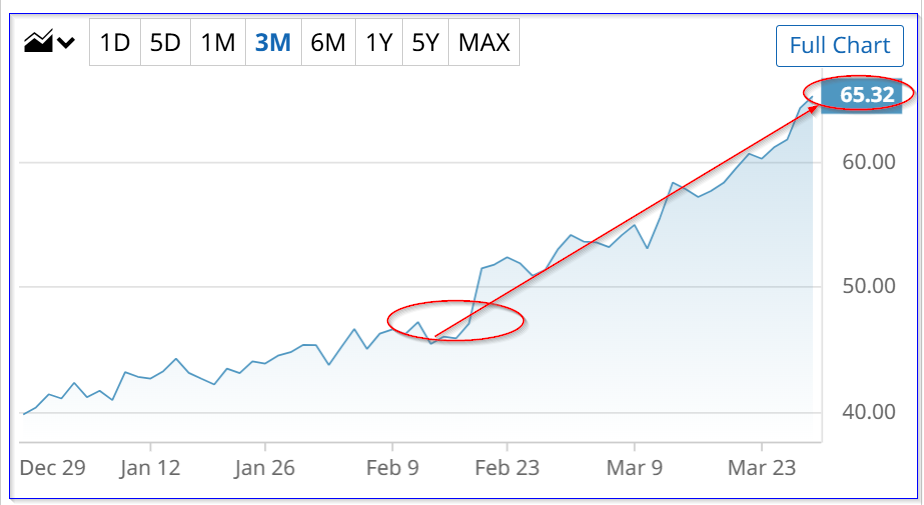

Occidental Petroleum (OXY) stock closed up 1.49% on Friday and has risen 23% since the end of February. Even if it's not a peak, it might make sense to sell OXY covered calls, given the high out-of-the-money one-month expiry OXY call premiums.

OXY is at $65.32, up 23.1% from $23.08 at the end of February, right before the Iran war started. And it's up almost $20 or 43.6% since Feb 12 ($45.49). Has it reached a peak?

Analysts say OXY stock looks overvalued, based on their average price targets (PTs). For example, Barchart's mean survey price target is $59.11, and 26 analysts surveyed by Yahoo! Finance have an average PT of $60.28.

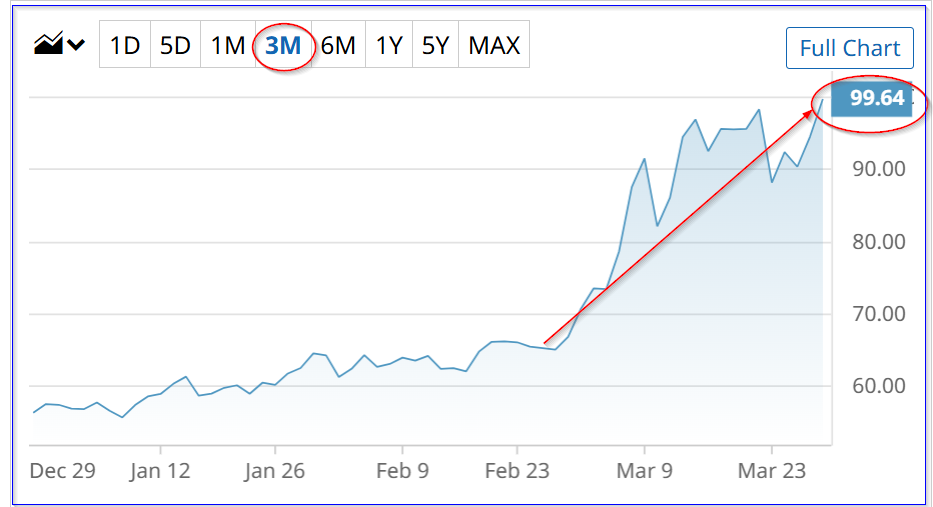

Obviously, if the price of oil keeps rising exponentially, it's possible that OXY may keep pushing higher. For example, look at the Barchart chart below for West Texas Intermediate oil:

It clearly shows a direct correlation between the price of OXY and the oil futures price. So, in a way, it doesn't really matter what analysts think, right?

However, don't forget that the market discounts the OXY price based on oil and gas price expectations. The price incorporates what income OXY will receive over the next 6 to 9 months. In a sense, OXY's price has already incorporated a forecast of higher oil prices.

So, that might make an investor consider selling their shares now, especially if OXY is deemed at a peak. However, a better way to do this, without making a sale and giving the investor more alternatives, is to sell out-of-the-money (OTM) covered calls.

After all, one-month expiry premiums seem to be very high now. This article will show why some investors might want to take advantage of these high premiums by shorting them.

Selling OXY Covered Calls

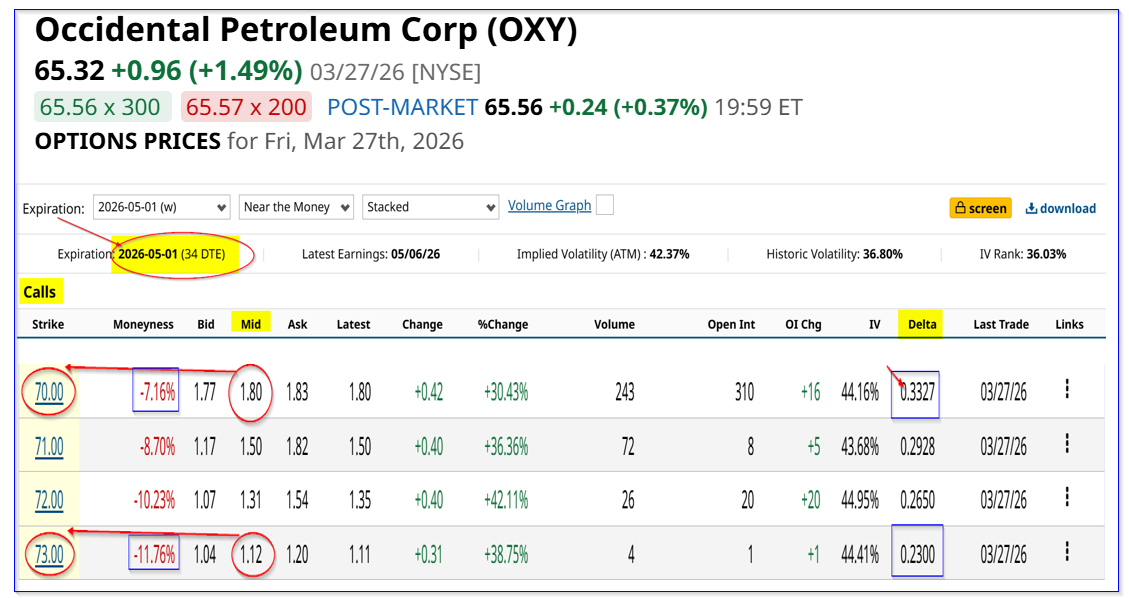

For example, look at the May 1, 2026, expiration option chain, just over one month from now. It shows that the $70.00 call option contract has a very attractive midpoint premium of $1.80

That means an investor who owns 100 shares of OXY, or buys them at $65.32 (Friday's close), can make an immediate 2.76% yield over the next month:

$180 received / $6,532 cost for 100 shares = 0.02755 = 2.755% yield

However, there is a fairly high risk that OXY could rise another $4.68 or +7.16% in the next 34 days. The delta ratio is 33%, implying a one-third chance this could occur.

That's why the premium is so high. Is that a bad thing? Not necessarily.

Even if OXY goes to $70.00, the investor keeps the $180 call premium already received. The investor's 100 shares are assigned for sale at $70,00, or $7,000. So, the total profit is:

$180 + ($7,000 - $6,532) = $180 + $468 = $648 total return

That's equal to an ROI of almost 10% (i.e., 648/$6,532 = 0.0992 = 9.92%.

Higher Strike Prices

More risk-averse investors might want a much lower chance of having to sell their shares, but still make a good income.

The $73.00 call option contract, which is almost 12% higher (+11.76%), has a midpoing premium of $1.12. That implies a 1.715% one-month yield:

$112 / $6,532 = 0.17146 = 1.75% one-month yield

However, there is only a 23% chance of OXY rising to $73 by May 1 (i.e., the delta ratio is just 0.23).

Moreover, even if it rises to $72.99, i.e., +11.74% from Friday, the investor keeps the unrealized capital gain and does not have to sell their shares.

In addition, the total potential one-month return is over 13.5% even if OXY reaches $73.00 on or before May 1 (i.e., 11.76% + 1.75% = 13.51%.

And don't forget, the investor can always roll the call option forward if it looks like their shares will be called. This could lower the total potential return over the next period.

The bottom line is that OXY may be at a peak, but even if it isn't, it might make sense to sell out-of-the-money covered calls.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)