Big tech stocks have been treading water after last year’s surge, especially as companies pour billions into AI and data centers. Meta Platforms (META), the Facebook parent, has felt the pressure. Ad revenue growth is cooling from its pandemic peak, and Meta is ramping up spending on AI “superintelligence.” In that context comes the latest jolt when Meta confirmed it will cut “several hundred” jobs across units like sales, recruiting, and its Reality Labs VR arm. The company is also under increasing legal pressure from regulators.

The question now for investors is whether, with AI (and legal) costs mounting and layoffs announced, META stock looks like a buy, sell, or hold? Let's try to find out.

Meta’s Core Business Still Dominates Revenue

Meta Platforms is one of the world’s largest social media and ad-tech companies. It has 3.6 billion daily users and generates almost all its revenue from the Family of Apps segment. Its Reality Labs unit, VR/AR headsets, etc., is tiny by revenue, about 1% of the total, but has accumulated massive losses. CEO Mark Zuckerberg is now shifting focus toward AI, even as he seeks efficiency in the core business.

Recently, Meta delayed the rollout of its next big AI model, “Avocado,” after internal tests lagged Google’s (GOOG) (GOOGL) top models. Meta reiterated it’s on a “rapid trajectory” for better models and said more will roll out steadily. The company also acquired an AI-wearable startup, Limitless, to advance its “personal superintelligence” vision.

For now, Meta is following new EU rules, letting users choose fewer personalized ads, and addressing AI chat concerns. It’s using AI internally while keeping public launches compliant.

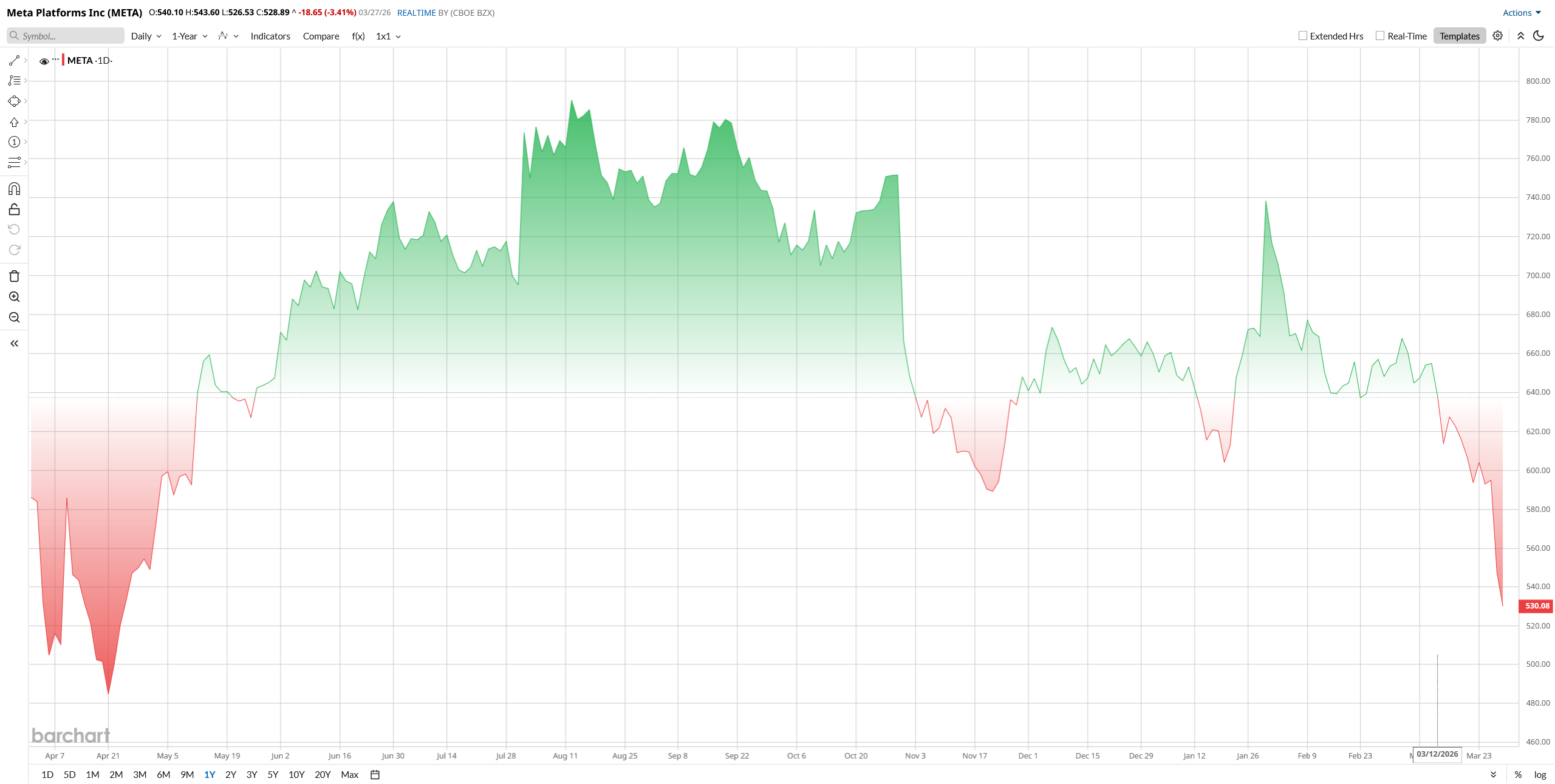

META’s stock rallied on a few past headlines, like AI progress and earnings beats in the past year, which were not enough to sustain these gains in 2026; now it is down roughly 20% year to date (YTD). The pullback signals investor concerns over slowing ad trends and heavy spending on AI and the metaverse.

From a valuation perspective, META remains richly priced, as its forward P/E is about 21×, well above typical tech/media peers 13×, and its EV/EBITDA is 15× versus an industry average around 11×. It means the stock trades at a premium on expectations of strong future growth and profits.

What Happened: Layoff News

On March 25, news broke that Meta was cutting “a few hundred” jobs. The layoffs spanned Reality Labs, sales, recruiting, and other teams. Meta framed this as routine restructuring; a company spokesperson said teams “regularly restructure” and that affected staff would be given “other opportunities” within the company. Indeed, with 79,000 total employees, the cuts are a tiny fraction of Meta’s workforce.

Going forward, analysts note the main impact is on expenses; trimming a few hundred jobs may save tens of millions, but Meta’s real story is the huge AI spend and ad growth. For now, the market seems focused on revenue trends and investment returns rather than this modest layoff.

Meta Q4 Shows Growth Yet Loss Cycle

Meta’s latest quarter showed accelerating growth but steep spending. Revenue jumped 24% year-over-year (YoY) to $59.89 billion, driven by more ads across Facebook and Instagram as daily active users rose about 7% YoY. Operating income rose only 6% to $24.75 billion because expenses swelled 40% to $35.15 billion on data center buildouts and research and development. Net income was $22.77 billion, up 9%, and diluted EPS was $8.88, 11% higher than a year ago, both beating Wall Street targets.

Meta also remains a cash cow. Free cash flow for the quarter was about $14.1 billion, and it ended 2025 with roughly $81.6 billion in cash and marketable securities. CFO Susan Li said this cash hoard allows Meta to fund its AI ambitions. Mark Zuckerberg summed it up by saying the company had strong business performance in 2025 and is now looking forward to advancing personal superintelligence in 2026.

In practice, nearly all of Meta’s revenue still comes from the Family of Apps. For instance, in fiscal 2025, that segment brought in about $198.8 billion, or 98.9% of total sales, up about 22% YoY, while Reality Labs revenue was about $2.2 billion. Reality Labs losses continued, and Meta said 2026 may be the peak year for those losses.

Management also provided upbeat guidance despite heavy spending. For the first quarter of 2026, Meta expects revenue between $53.5 billion and $56.5 billion, helped by about a 4% foreign exchange tailwind. For fiscal 2026, the company is budgeting $162 billion to $169 billion in total expenses, with sharply higher capital expenditures of up to $135 billion. Even with the spending surge, Meta expects operating income to exceed 2025 levels.

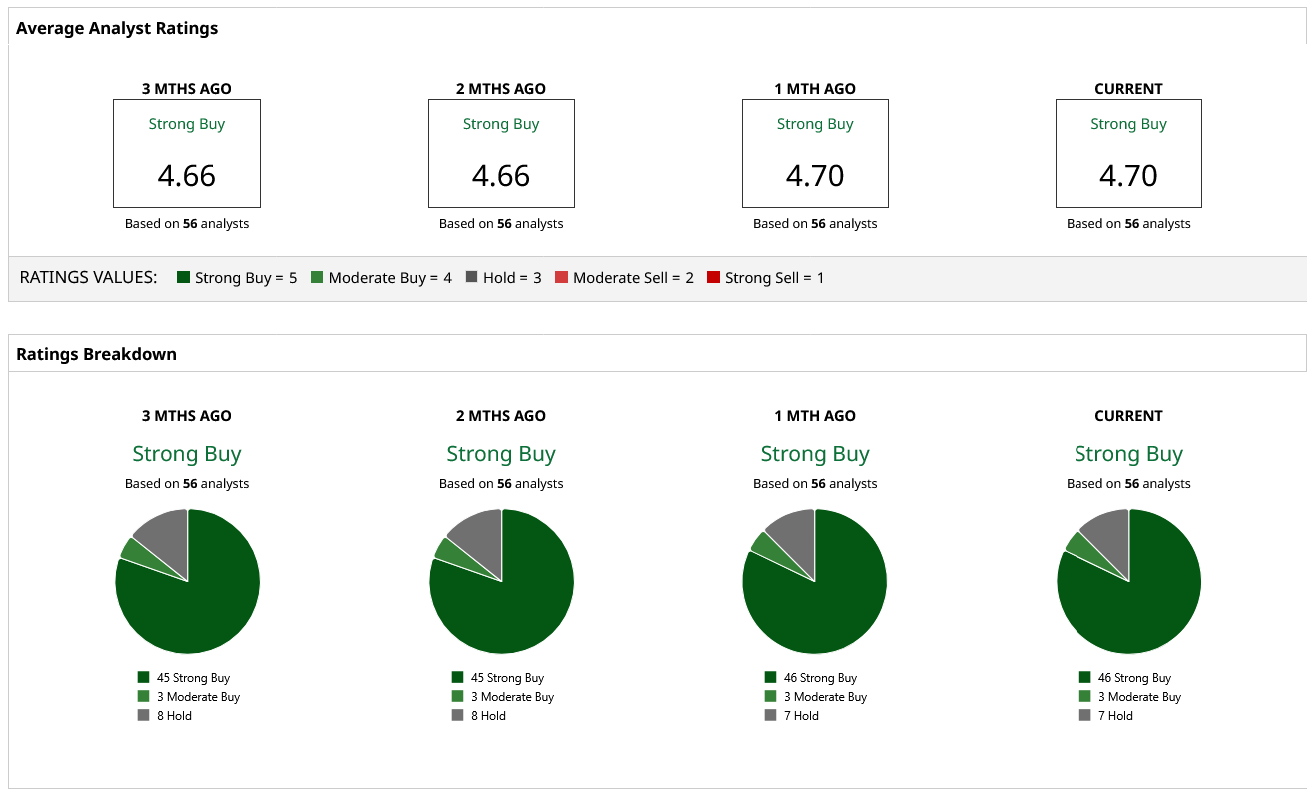

Analysts’ Take on META Stock

Analysts are generally optimistic about META stock, but with different price targets. Bank of America remains an outstanding bull, with a new target set at $885 from $810 and a “Buy” recommendation. According to BofA analyst Justin Post, Meta has a strong 21% revenue growth with 82% gross margins, and he writes that it is an infrastructure powerhouse that should be able to make free cash flows positive in 2026.

RBC Capital also maintained an “Outperform” on META at a target of $810. According to RBC, Meta beat Q4 and guided 10% higher than consensus, and Reality Labs' losses had reached their highest point.

Goldman Sachs was also encouraging: Goldman analyst Eric Sheridan kept a “Buy” rating but slightly raised his target to $835 with the support of growing ad momentum. On the cautious side, Morgan Stanley, which had reduced its target to $750 in December, admitted that Meta had good fundamentals. MS observed sentiment was apprehensive as higher spending P/E had stabilized to near-long-term levels, yet considers the data, distribution, and AI advantage of Meta as a strength.

Overall, Wall Street’s consensus target hovers around $864, which suggests nearly a 63% upside premium. According to Barchart, out of 56 analysts polled, most rate META as a “Strong Buy.”

On the one hand, the debate is obvious because bulls claim that the further earnings of ad and investing in AI by Meta are worth the premium, but Bears fear that the high valuation is due to the high expectations.

In the meantime, Meta provided a blueprint to increase record revenue and cash, but at a higher cost. I think the stock could rally if its AI investments translate into real productivity gains and returns without hurting overall profitability.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)