Unity Software (U) shares pushed higher on March 27 after the game software company reported its preliminary Q1 results that came in ahead of its prior guidance. Investors cheered the San Francisco-headquartered firm also on reports that U is considering selling its China business at a valuation of more than $1 billion.

Despite today’s surge, however, Unity stock remains down nearly 60% versus its year-to-date high.

Why China News Warrants Buying Unity Stock?

Unity now sees its revenue coming in at $505 million at least, handily beating its earlier outlook for $490 million tops. But the China exit news is a strong reason to buy U shares into strength today.

Why? Because it will remove a significant geopolitical risk that the firm’s own SEC filings flagged, while adding more than $1 billion to a balance sheet that already holds roughly $2 billion in cash.

CEO Matt Bromberg characterized the restructuring as “addition by subtraction.” And analysts agree that concentrating on the game engine and Vector AI platform positions Unity for faster growth and better profitability.

Note that U closed marginally above its 20-day moving average (MA) on Friday, indicating bullish momentum could accelerate in the coming week.

Where Options Data Suggests U Shares Are Headed

Unity shares remain attractive also because the company, under Matt Bromberg, has pivoted from “growth at any cost” to a sustainable increase in EBITDA. This may be part of the reason why options pricing signals a bullish skew at the time of writing.

According to Barchart, the put-to-call ratio on contracts expiring mid-June sits at 0.88x currently, with the upper price on those contracts at about $24, indicating potential upside of over 20% from here.

Finally, at roughly 4x sales, Unity Software is trading at a discount to its historical multiple in 2026.

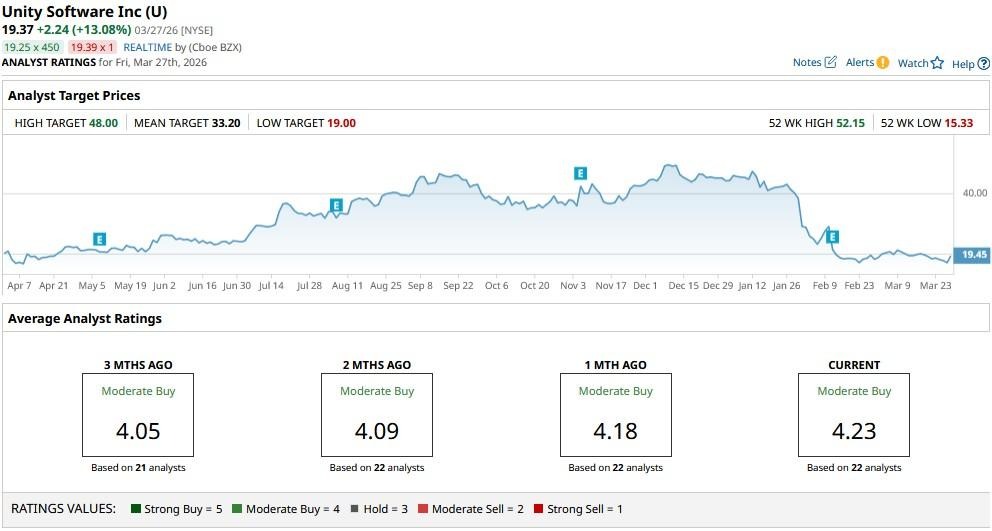

How Wall Street Recommends Playing Unity Software

Wall Street analysts seem to agree with options traders that U stock is undervalued at current levels.

The consensus rating on Unity Software remains at a “Moderate Buy,” with the mean price target of about $33 indicating potential upside of more than 65% from here.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

/Johnson%20%26%20Johnson%20location%20sign-by%20JHVEPhoto%20via%20iStock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)