/Textron%20Inc_%20magnified%20logo-by%20Pavel%20Kapysh%20via%20Shuuerstock.jpg)

Providence, Rhode Island-based Textron Inc. (TXT) is a global multi-industry company that manufactures aircraft, automotive engine components, and industrial tools. Valued at $15.5 billion by market cap, Textron operates through Textron Aviation, Bell, Textron Systems, Industrial, Textron Aviation, and Finance segments.

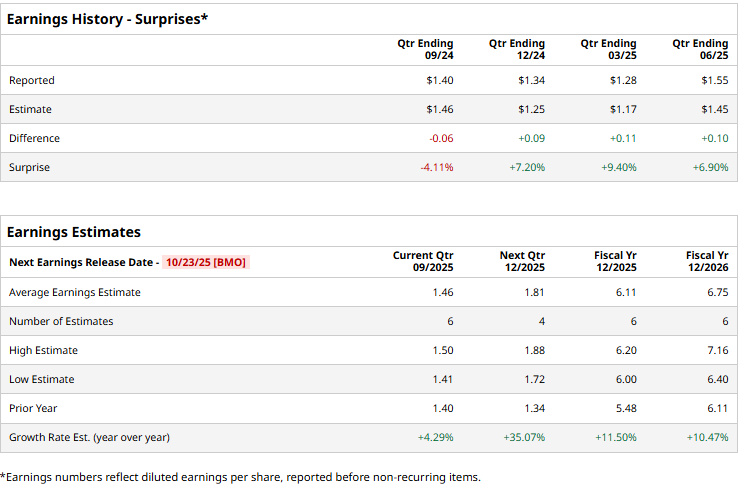

The industrial sector major is set to announce its third-quarter results before the market opens on Thursday, Oct. 23. Ahead of the event, analysts expect Textron to deliver an adjusted profit of $1.46 per share, up 4.3% from $1.40 per share reported in the year-ago quarter. The company has a mixed earnings surprise history. While it surpassed the Street’s bottom-line estimates thrice over the past four quarters, it missed projections on one other occasion.

For the full fiscal 2025, TXT is expected to deliver an adjusted EPS of $6.11, up 11.5% from $5.48 in 2024. In fiscal 2026, its earnings are expected to surge 10.5% year-over-year to $6.75 per share.

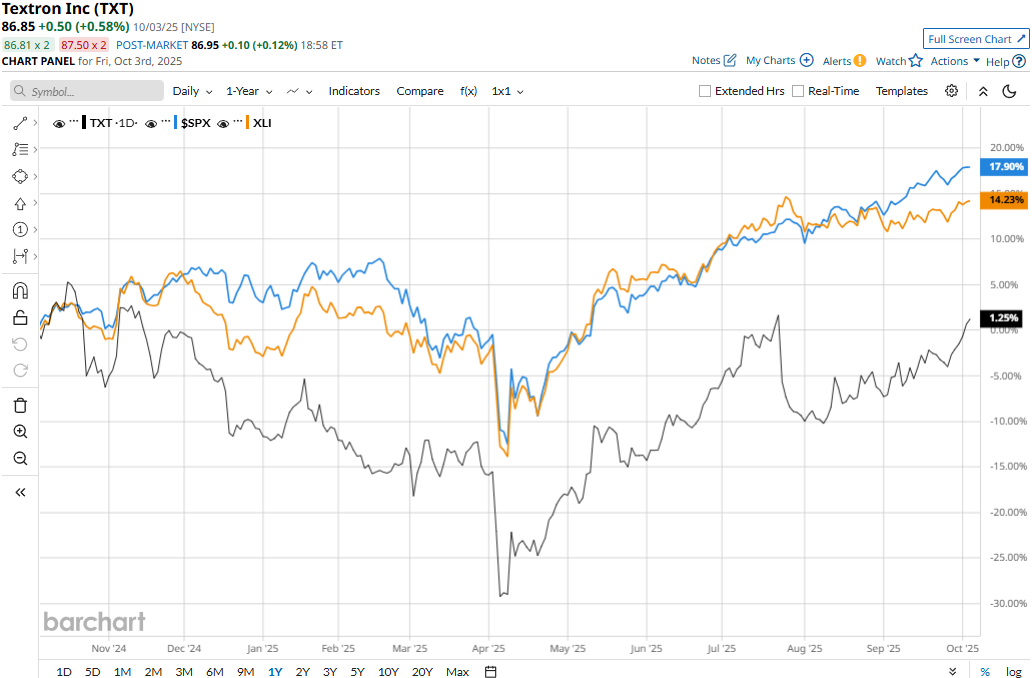

Textron’s stock prices have observed a marginal 86 bps uptick over the past 52 weeks, notably underperforming the S&P 500 Index’s ($SPX) 17.8% surge and the Industrial Select Sector SPDR Fund’s (XLI) 14.7% gains during the same time frame.

Despite reporting better-than-expected topline and earnings, Textron’s stock prices plunged 7.2% in the trading session following the release of its Q2 results on Jul. 24. Although the company’s industrial revenues observed a decline, driven by growth in commercial aircraft and helicopter businesses, the company’s overall revenues came in at $3.7 billion, up 5.4% year-over-year, 2.4% above the Street’s expectations. Meanwhile, TXT reported a modest 65 bps increase in adjusted EPS to $1.55, surpassing the consensus estimates by 6.9%.

However, the company reported notable quarter-on-quarter declines in Aviation, Bell, and Textron Systems’ backlogs, which unsettled investor confidence.

Nonetheless, analysts remain optimistic about the stock’s prospects. TXT maintains a consensus “Moderate Buy” rating overall. Of the 14 analysts covering the stock, opinions include five “Strong Buys” and nine “Holds.” Its mean price target of $92 suggests a 5.9% upside potential from current price levels.

On the date of publication, Aditya Sarawgi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20concept%20image%20of%20space_%20Image%20by%20Canities%20via%20Shutterstock_.jpg)

/A%20concept%20image%20of%20a%20flying%20car_%20Image%20by%20Phonlamai%20Photo%20via%20Shutterstock_.jpg)