Charter has gotten torched over the last six months - since November 2025, its stock price has dropped 25.4% to $148.50 per share. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Charter, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Charter Will Underperform?

Even though the stock has become cheaper, we're swiping left on Charter for now. Here are three reasons we avoid CHTR and a stock we'd rather own.

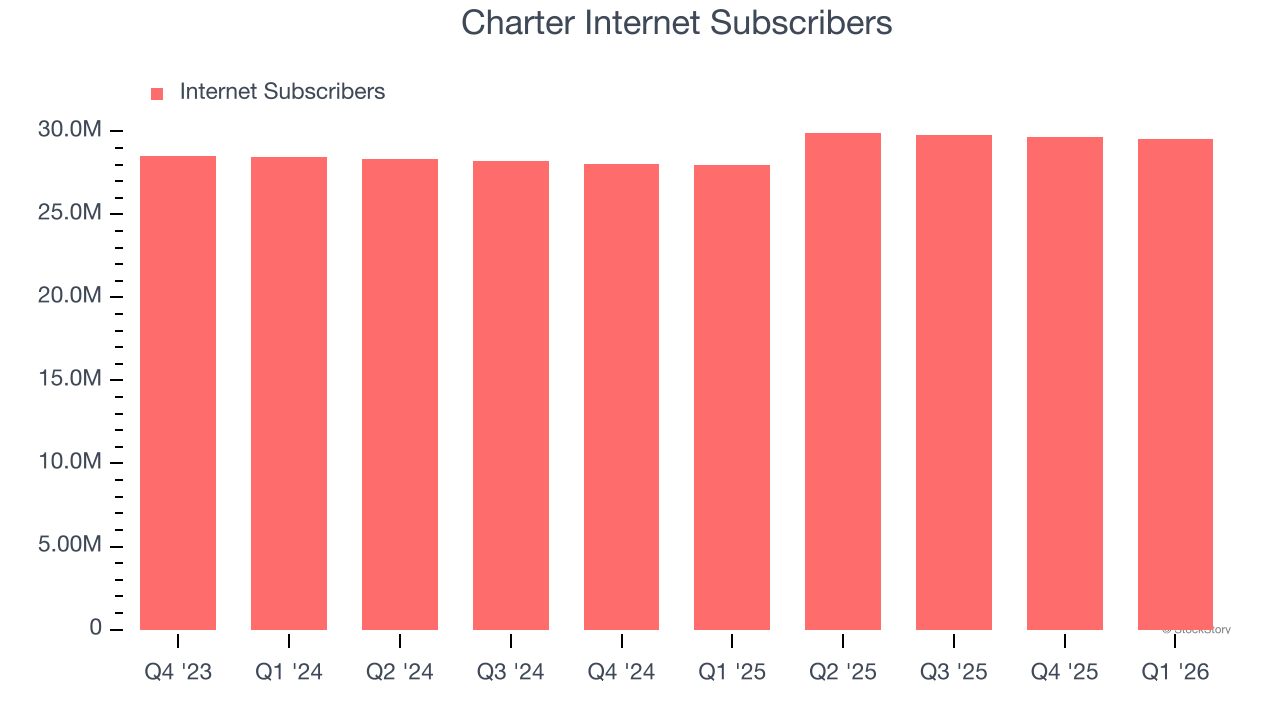

1. Weak Growth in Internet Subscribers Points to Soft Demand

Revenue growth can be broken down into changes in price and volume (for companies like Charter, our preferred volume metric is internet subscribers). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Charter’s internet subscribers came in at 29.56 million in the latest quarter, and over the last two years, averaged 3.2% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

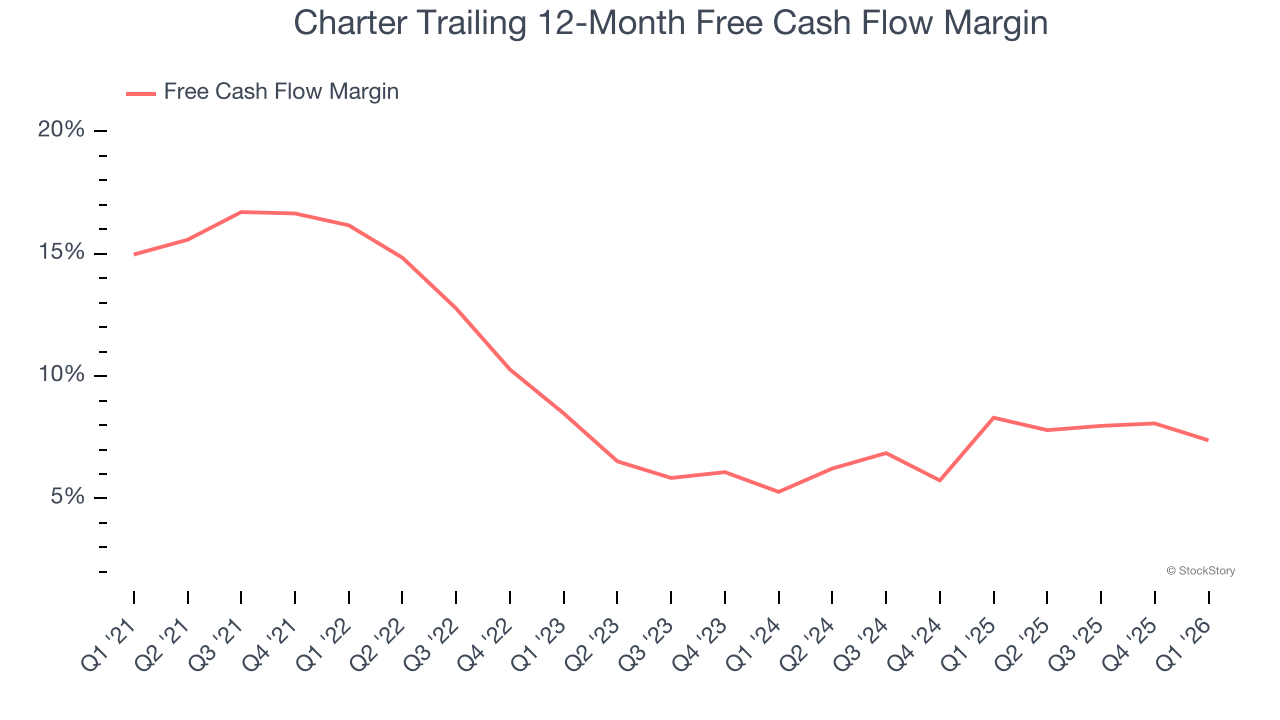

2. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Charter has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 7.8%, below what we’d expect for a consumer discretionary business.

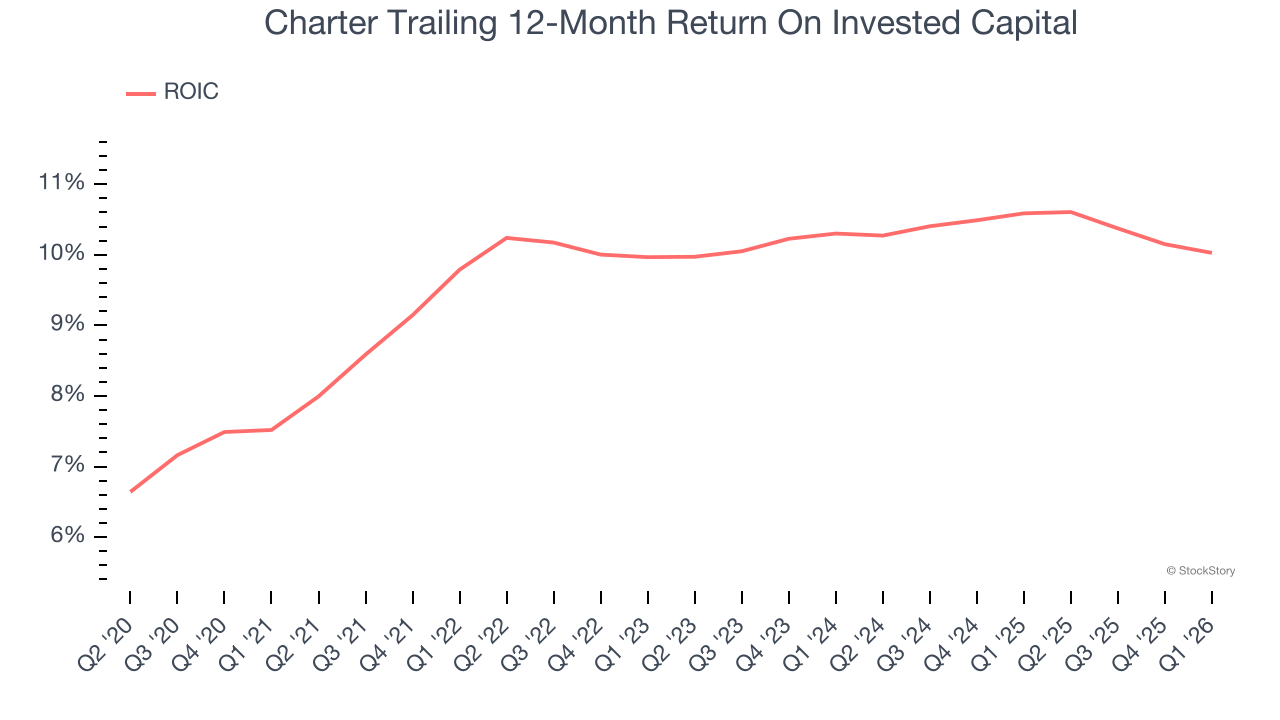

3. New Investments Aren’t Moving the Needle

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Charter’s ROIC has stayed the same over the last few years. If the company wants to become an investable business, it must improve its returns by generating more profitable growth.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of Charter, we’ll be cheering from the sidelines. Following the recent decline, the stock trades at $148.50 per share (or a forward price-to-sales ratio of 0.3×). The market typically values companies like Charter based on their anticipated profits for the next 12 months, but there aren’t enough published estimates to arrive at a reliable number. You should avoid this stock for now - better opportunities lie elsewhere. We’d recommend looking at one of our top digital advertising picks.

Stocks We Like More Than Charter

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month - FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

/Abbott%20Laboratories%20vials%20and%20Logo-by%20Melniov%20Dmitriy%20via%20Shutterstock.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Intuit%20Inc%20logo-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)